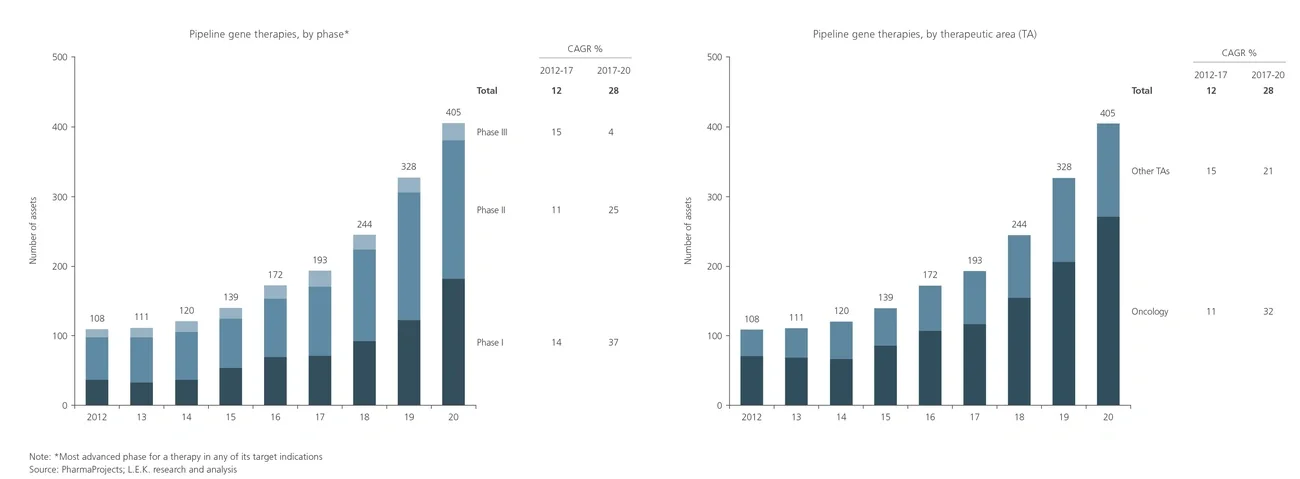

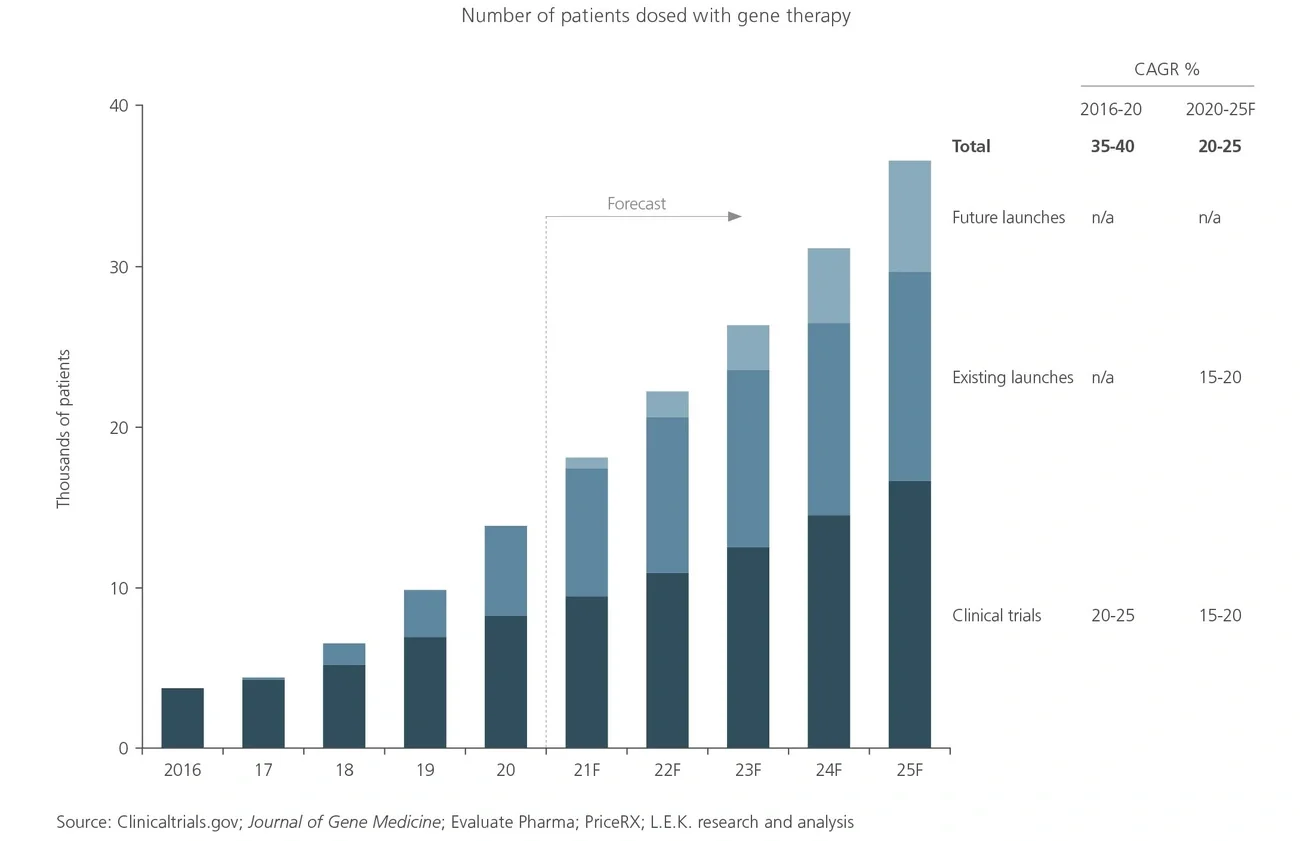

Substantial interest and investment in gene therapies has arisen from the promise of curative treatments for high-unmet-need diseases and the associated commercial opportunities. As a result, there is a rapidly growing clinical pipeline of gene therapies, with the first launches occurring in recent years. The market is currently experiencing a shortage of manufacturing capacity to serve these products, and L.E.K. Consulting’s analysis suggests that this bottleneck is likely to become more acute in the near to mid-term.

In this Executive Insights, we discuss the expected disparity between the demand for manufacturing capacity and current supply, and explain the strategic choices available to biopharma companies.