Although there are several currently active mines, demand is expected to outstrip supply. However, the industry is taking steps to expand its sourcing of raw materials; both the U.S. and Europe are increasing their lithium mining capacity, for example. Meanwhile, individual companies are working to produce alternative technologies such as solid-state batteries and hydrogen fuel cells.

The environmental impact of traditional mining. The processes required to mine the materials needed to make batteries, among them lithium ore, rely heavily on the use of natural resources and cause numerous adverse impacts to the environment. Sourcing is also costly and highly concentrated in particular regions of the world, such as Chile, Australia and China, while global geopolitical tensions pose a threat to the security of supply. With that in mind, manufacturers (e.g., Tesla, BMW) are building new lithium cell production facilities adjacent to their existing plants, and interest around opening more mines stateside is growing. Brine extraction methods are also being utilized to minimize environmental harm.

Considerations around ethical extraction in sourcing countries. The key raw materials used to make batteries — namely lithium, cobalt and nickel — are found in regions of the world where environmentally sensitive areas, operations exposure to protected territories and questionable extraction practices are likely to create legal implications. Chile, Australia, China and Argentina are responsible for some 95% of the world’s lithium mining, which results in pollution of and water shortages for surrounding communities. Cobalt is primarily mined in the Democratic Republic of the Congo, which has a history of conflict, corruption and child labor. The serious injuries to and deaths of children working in cobalt mines have already prompted accusations and even lawsuits against the likes of large manufacturers such as Apple, Google, Microsoft and Tesla. Indonesia and Australia are the largest suppliers of nickel, and those mines are often located on the lands of Indigenous people, forcing local populations to relocate.

Potentially higher cost of procurement due to underlying shortages. The growing demand for lithium, nickel and cobalt, itself the most expensive battery metal in the world, has driven soaring prices in recent years and is expected to continue to rise for the foreseeable future, increasing pressure on manufacturers’ procurement costs.

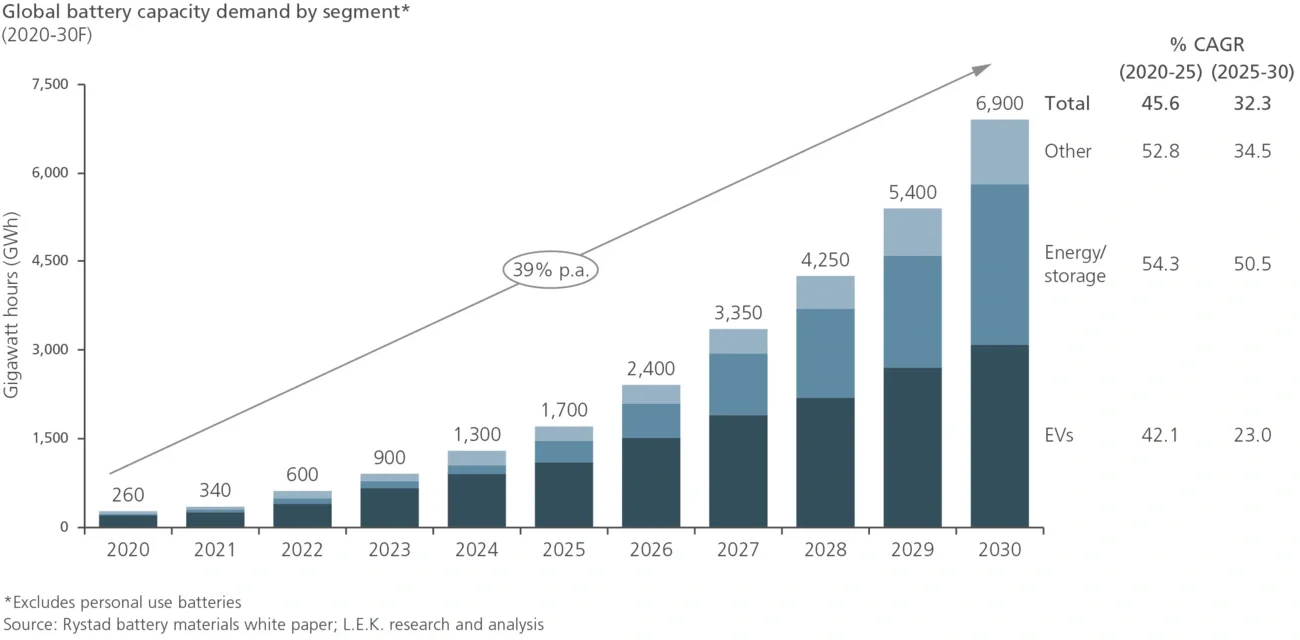

Probability that battery manufacturing will lag expected growth in demand. Fueled largely by the EV market, global demand for battery capacity is expected to continue growing at a rapid pace, reaching 6.8 terawatt hours (TWh) by 2030. But supply of critical materials (e.g., lithium, cobalt, nickel, graphite) may fail to keep pace with skyrocketing demand as slow financing and extraction act as barriers to bolstering new capacity.

A need for more cost-effective recycling of lithium. Recycling lithium batteries is a highly complex, capital-intensive process, one that requires sophisticated equipment in order to treat the resulting hazardous emissions. And different batteries contain different lithium-based materials, which in turn require different recycling processes. Plus, while recycling will recover the value of raw materials in the near term, the value of these raw materials fluctuates significantly from year to year and, with it, the overall profitability of recycling them. The good news is that the number of recyclers and second-life players, which take batteries that no longer meet automotive standards and utilize them for less-demanding energy storage applications, is expected to rise in coming years. Market consolidation is also expected to continue, and larger players will be able to repurpose batteries at costs that are significantly lower than the costs at which they repurpose today.