US Infrastructure Plan

A Window of Opportunity in the Building and Construction Industry?

A Window of Opportunity in the Building and Construction Industry?

The magnitude of the U.S. infrastructure plan, which was passed in November 2021 — $550 billion, front-loaded over 2022-25 — is without precedent in modern history. It comes at a time of very strong residential demand and recovering commercial construction. Combined, these factors amount to an extremely robust demand outlook in the building and construction industry.

Supply, on the other hand, is expected to be tight. Utilization rates for key construction inputs such as cement, concrete and asphalt are already high, while industrial metal prices have soared and labor shortages are back to their highest levels.

In the past, such as during the housing boom of the early 2000s, milder increases in demand combined with high utilization rates have led to substantial price increases, well above underlying inflation, and generated significant profit upside for industry participants.

Historically, market participants have tended to be reactive to situations of profit expansion, but they currently have a window of opportunity to invest tactically before production capacities are saturated and profits surge.

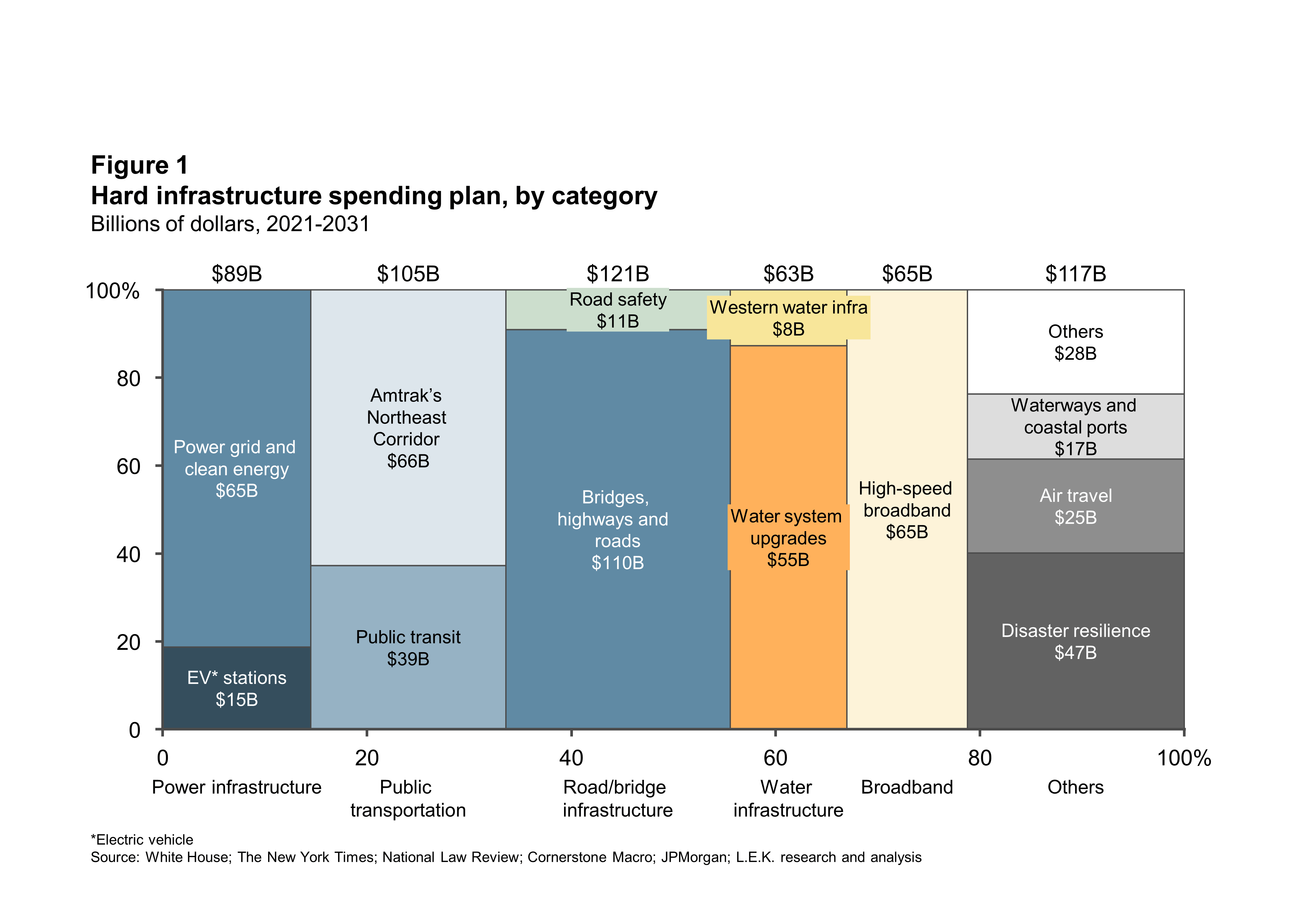

Two funding streams for infrastructure are currently in play. The Infrastructure Investment and Jobs Act (see Figure 1), which passed the Congress in November 2021, focuses on “hard infrastructure” (roads, bridges, tunnels, public transportation and the power grid) with an overall allocation of $550 billion. We regard it as our “base case.”

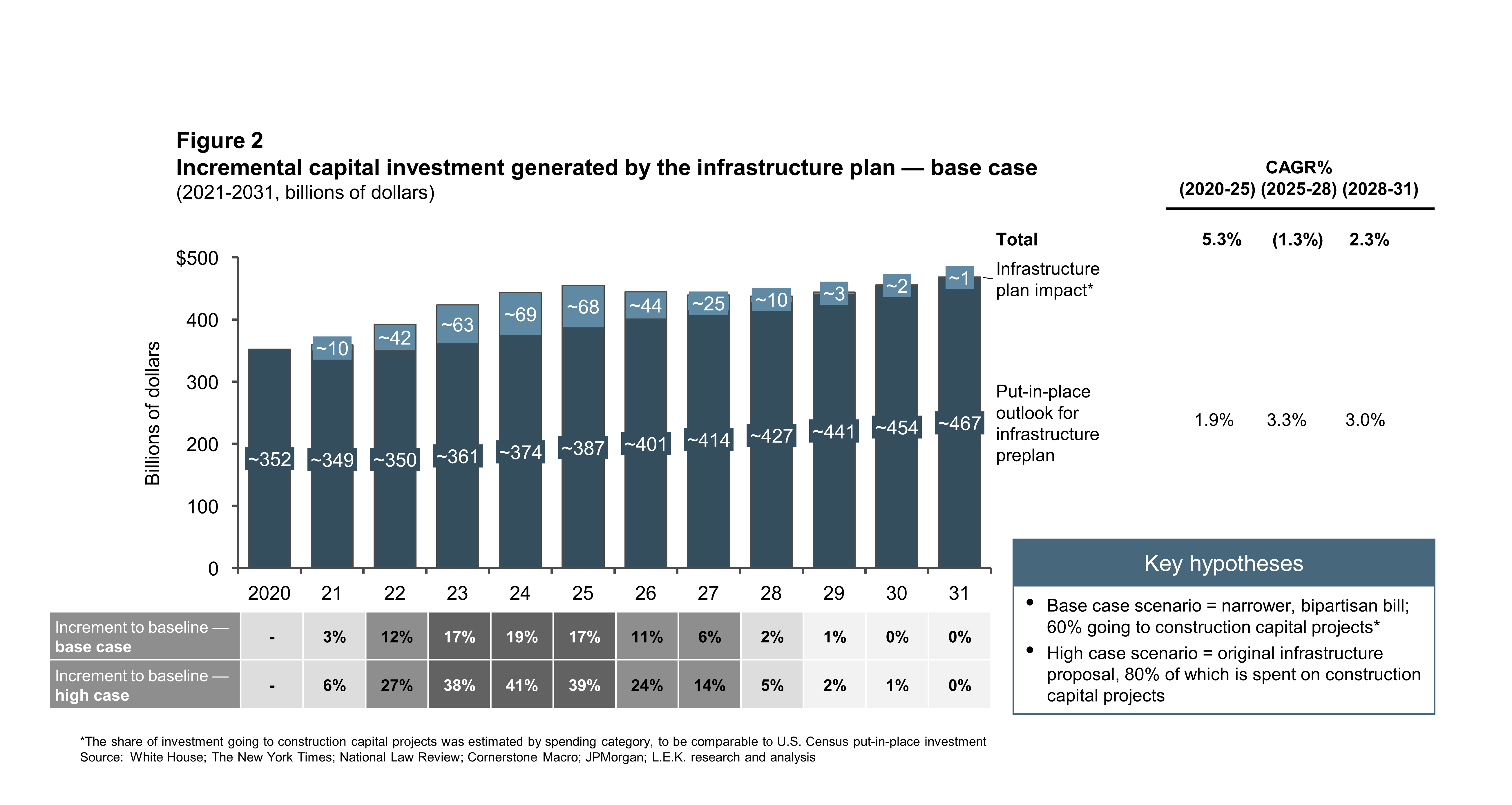

A separate reconciliation bill due for consideration in the House and then the Senate may restore some of the administration’s originally proposed funding levels that were reduced in or removed from the Bipartisan Infrastructure Framework. We regard this higher outlay — a total expenditure of $930 billion, 80% of which is allocated to construction capital projects — to be our “high case.”

Both infrastructure proposals are heavily front-loaded, with a sharp increase in overall infrastructure spending throughout, but especially at the start of the funding period, from 2022 through 2026 (see Figure 2).

The increase in infrastructure spending takes place in the context of a construction boom already in progress — the result of continued residential demand, a recovery in commercial construction, and strong fundamentals at the state and local level, thanks to an influx of federal pandemic stimulus funds.

Residential demand has seen recent high growth, especially in single-family starts, which increased by 11.5% from 2019 to 2020 and is forecast to continue to grow robustly. There have been limiting factors in the recovery in commercial construction, but improvement is projected over the next couple of years.

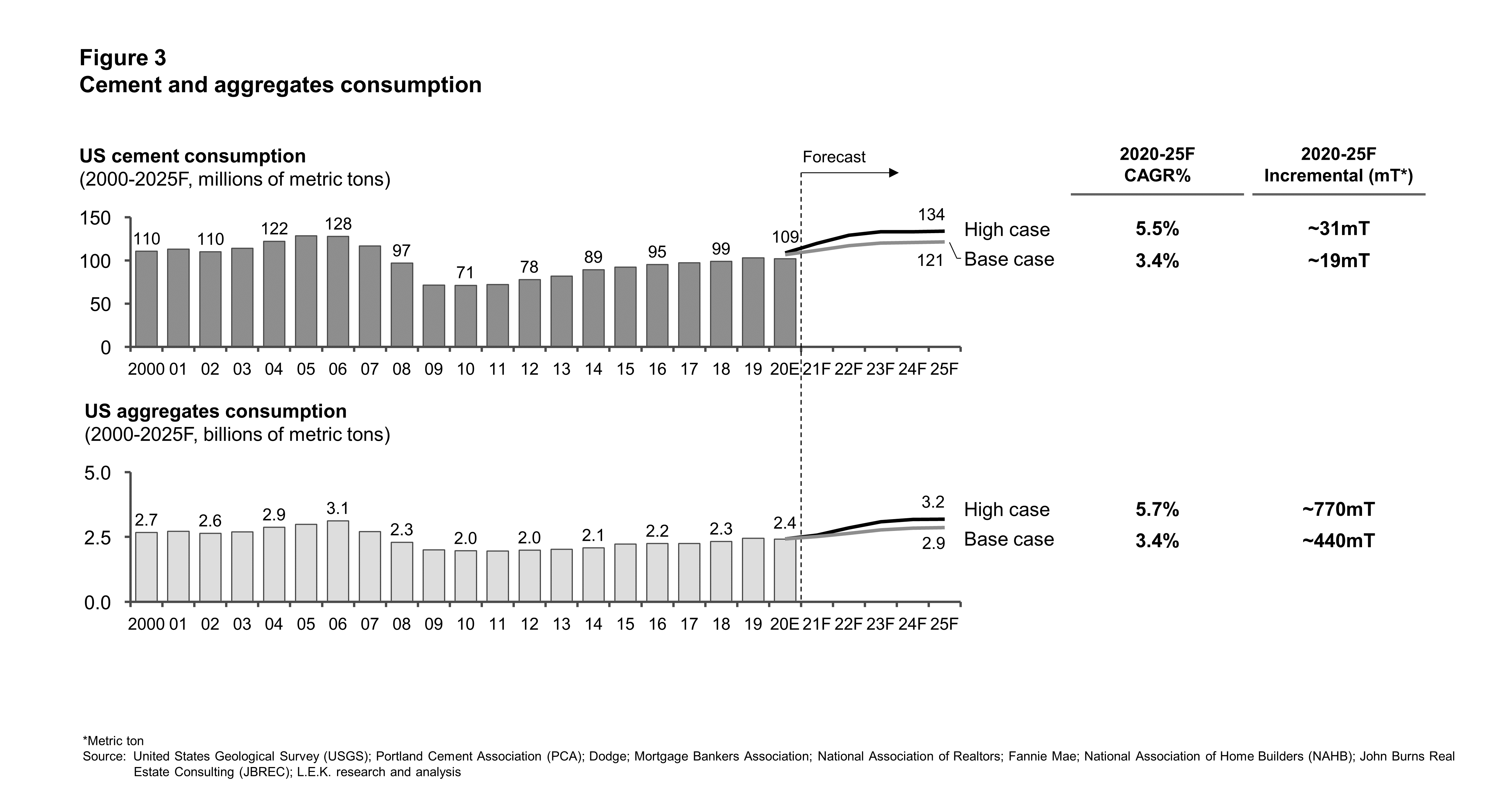

These dynamics — along with the sharp increase in federal infrastructure spending — are highly likely to lead to a demand surge for construction inputs (see Figure 3).

Demand for materials is not the only factor to consider. The strong demand comes at a time when the labor supply is already constrained (54% of respondents to the 2020 Associated General Contractors survey expected to have a hard time filling some or all positions in 2021), prices for construction-related commodities have surged to peak or near-peak levels, and utilization for a number of key materials is already high.

Construction-related commodity prices have also surged. Copper and aluminum prices peaked in the spring and steel prices peaked in late August, and all three are currently not far below those highs. Prices for cement and ready-mix concrete are increasing steadily.

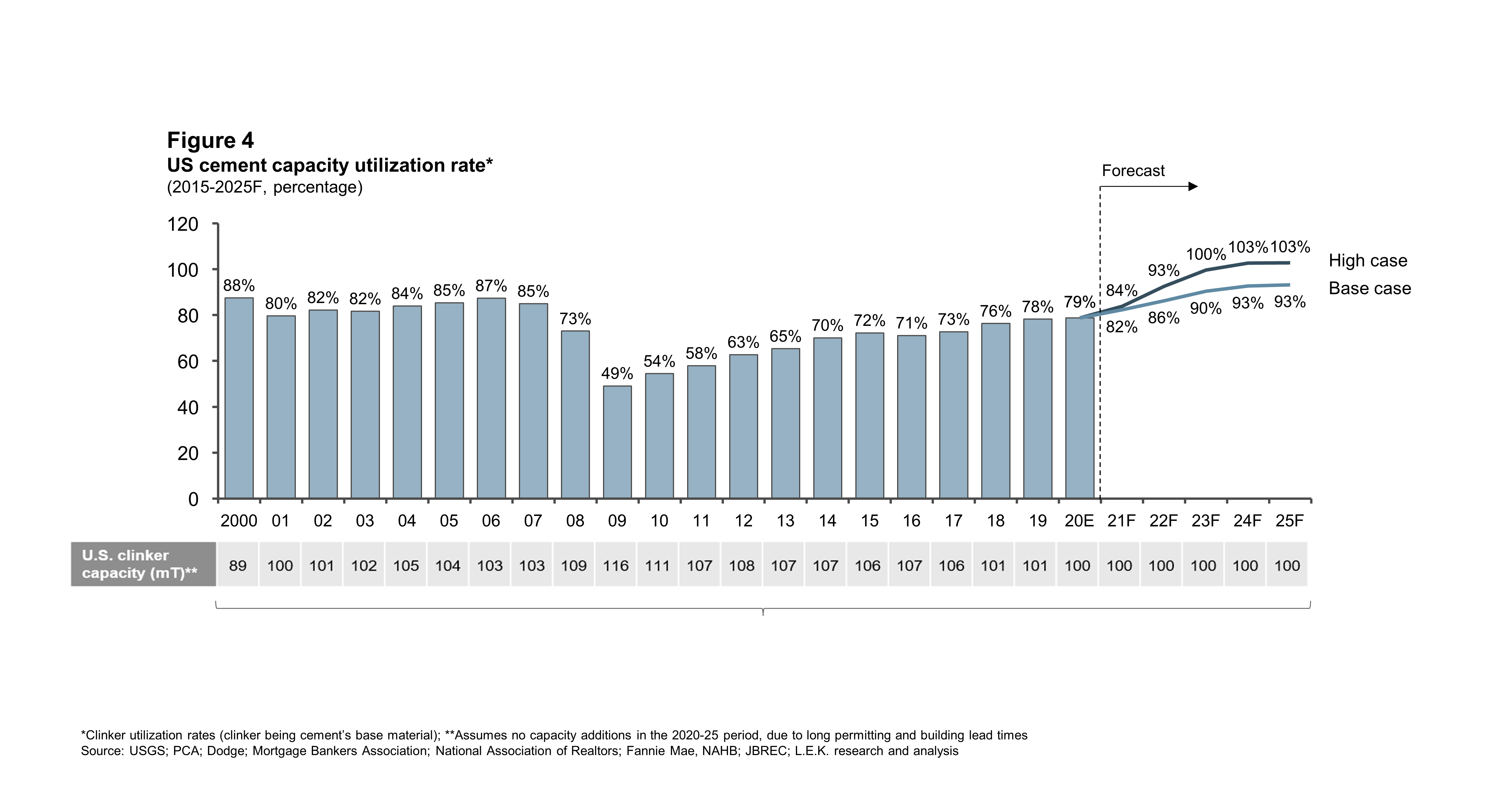

Finally, utilization rates for critical construction inputs are already high and expected to increase (see Figure 4).

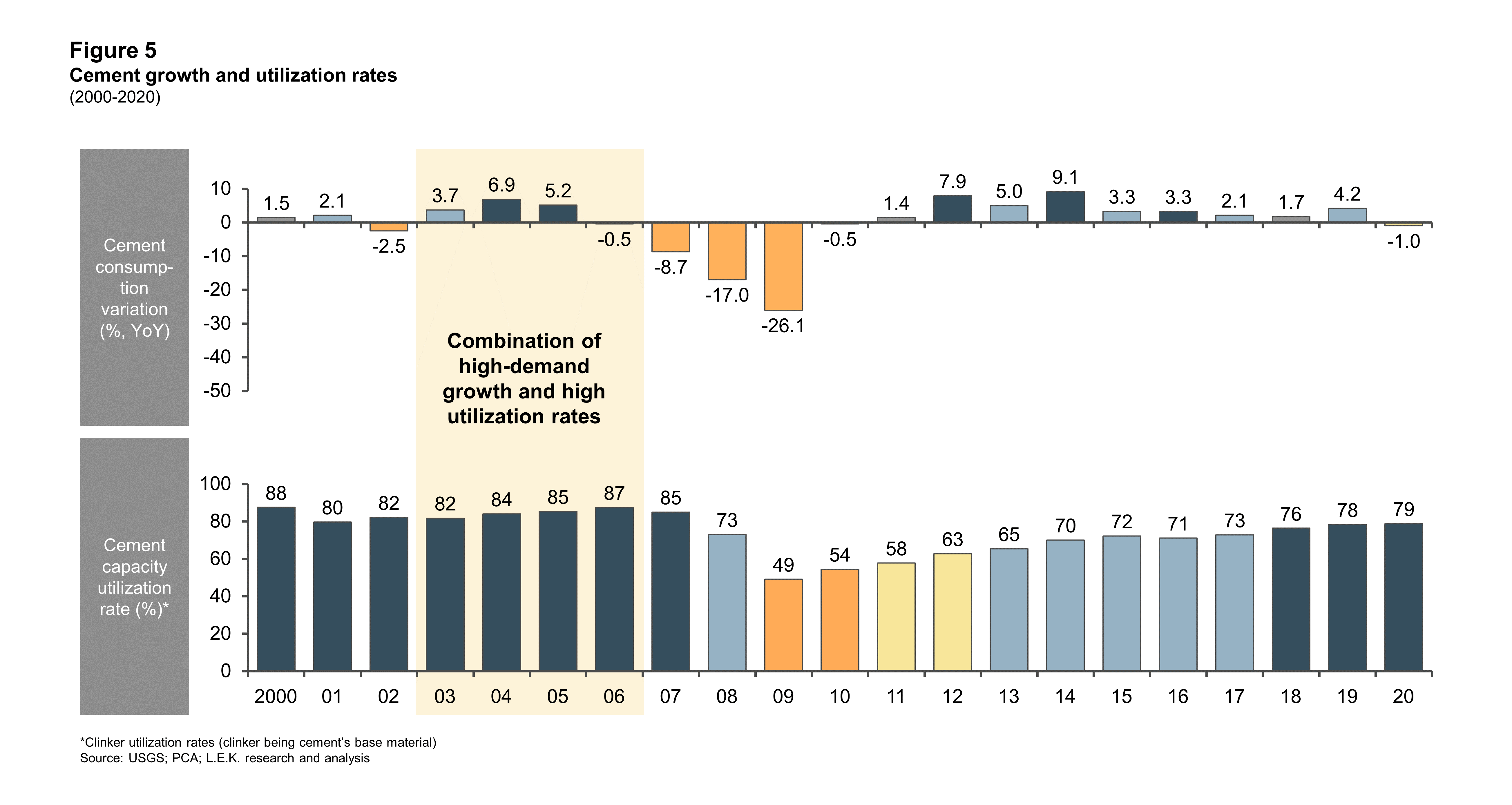

The current market dynamic — involving high demand and high utilization rates — suggests parallels to the 2003-06 construction boom (see Figure 5).

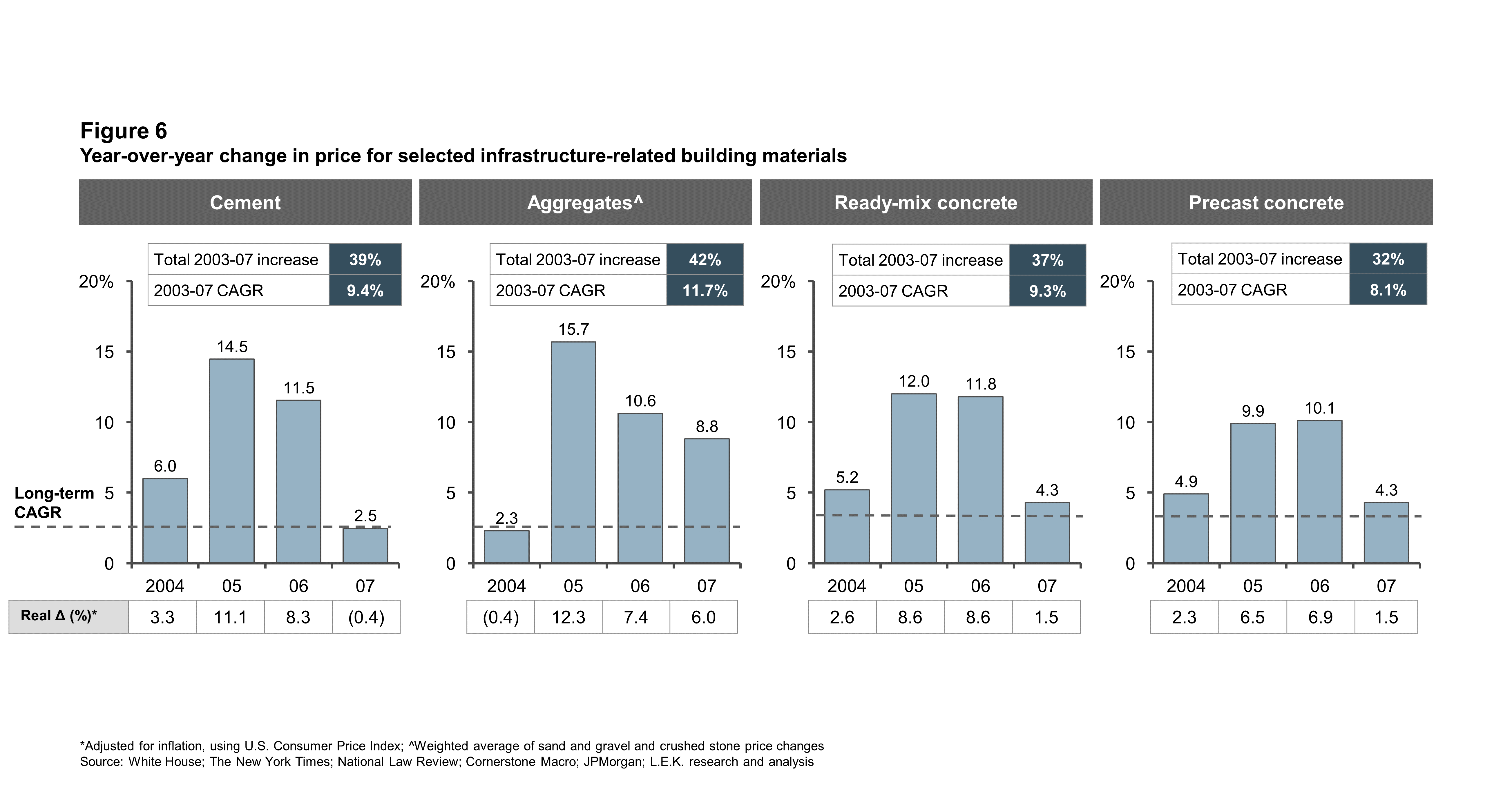

The result during that time period was not just an overall price surge, but also the timing of the surge itself, with a significant price/demand increase occurring late in the cycle (see Figure 6).

That was good news for materials producers. As prices rose significantly faster than production costs during that period, the combined profitability of publicly traded producers of heavy construction material more than doubled — margins increased by a factor of 2.2 (from 6.5% in 2002 to 14.1% in 2007) during the period of highest demand growth and highest utilization.

But other dynamics of that earlier boom are cause for concern. Most market participants were reactive to demand growth and to price increases. Peak investment coincided with a peak in demand, with the result that prices moved with demand, and investors lost the opportunity to fully capitalize on the demand surge.

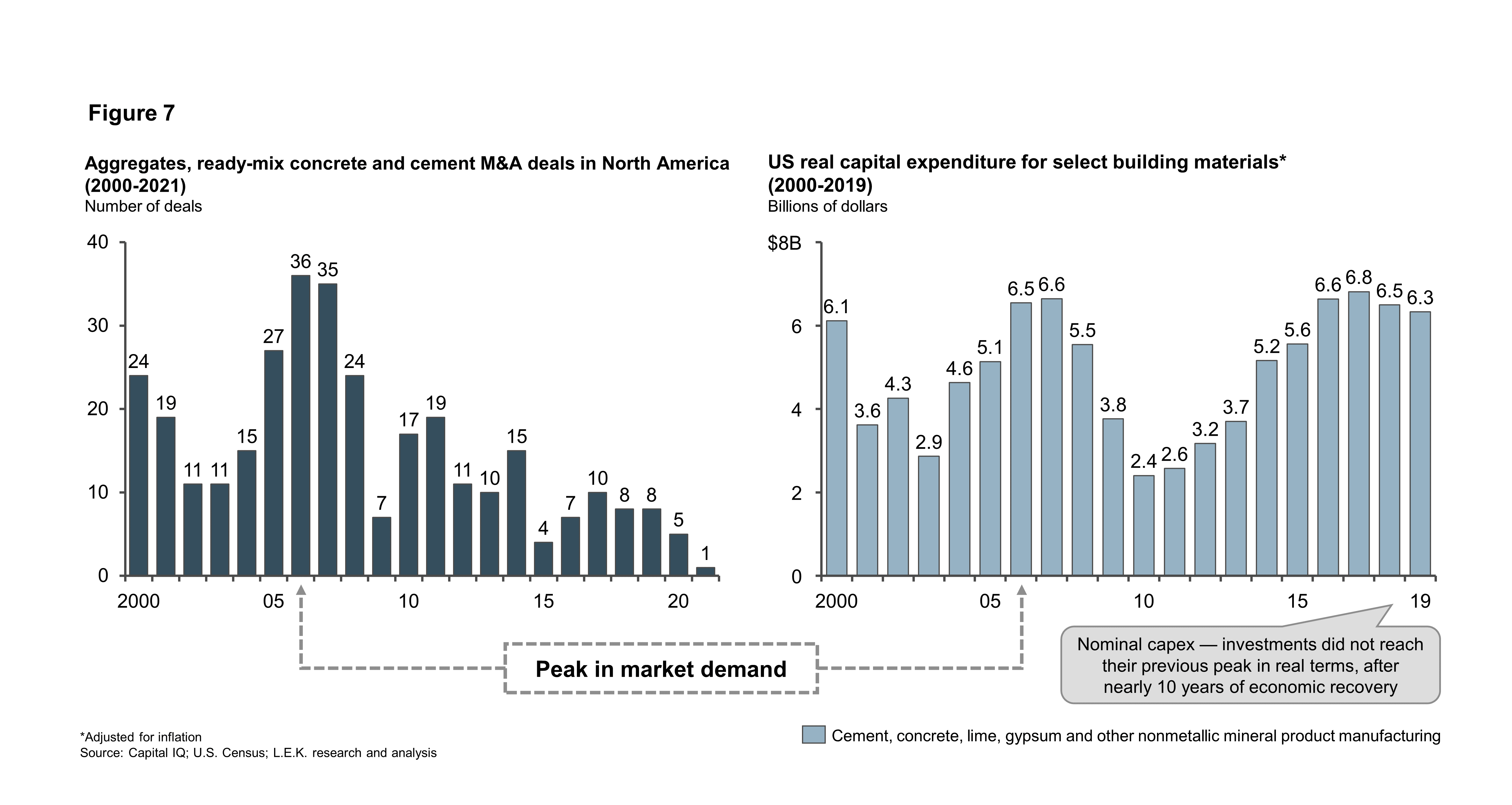

For a more detailed analysis, please see Figure 7 below.

Anticipating the significant uptick in activity and the coming increase in demand, it should be possible — unlike in the previous boom — to invest ahead of demand and to build a materials reserve that reduces costs during peak demand periods.

We recommend that market participants and investors:

While the coming surge of infrastructure investment is likely to produce price increases as well as shortages of existing materials, there is no need to repeat the experience of the last demand surge. By keeping close watch on infrastructure spending and planning carefully to take advantage of peak demand, market participants and investors can avoid the traps of reactive purchasing and investment, and instead seize the moment that this landmark infrastructure legislation affords.