The global transition to a lower-carbon energy system is spurring the rapid development of renewable energy generation and electrification of the transport sector. In the U.S. this shift has already translated into progress on multiple fronts: an energy market that currently surpasses 100 gigawatts (GW) of installed solar capacity, a national goal supporting an offshore wind project pipeline expected to add approximately 30 GW of capacity by 2030, a more stable onshore wind installation landscape, and the commitment by leading U.S. auto manufacturers to a future of 100% electric vehicle fleets. While these developments are certainly supportive of long-term climate goals, they are also creating considerable challenges for utilities and transmission operators amid their efforts to maintain a reliable, flexible and resilient power grid.

While several approaches may bolster the power grid — expansion of transmission and distribution infrastructure, use of performance analysis software to optimize solar and wind generation, and a buildout of reserve capacity from conventional resources — energy storage has emerged as the solution that best addresses the combined needs of cost-effectiveness, capital efficiency, ease of deployment into operations, dispatchability and the ability to meet policy objectives.

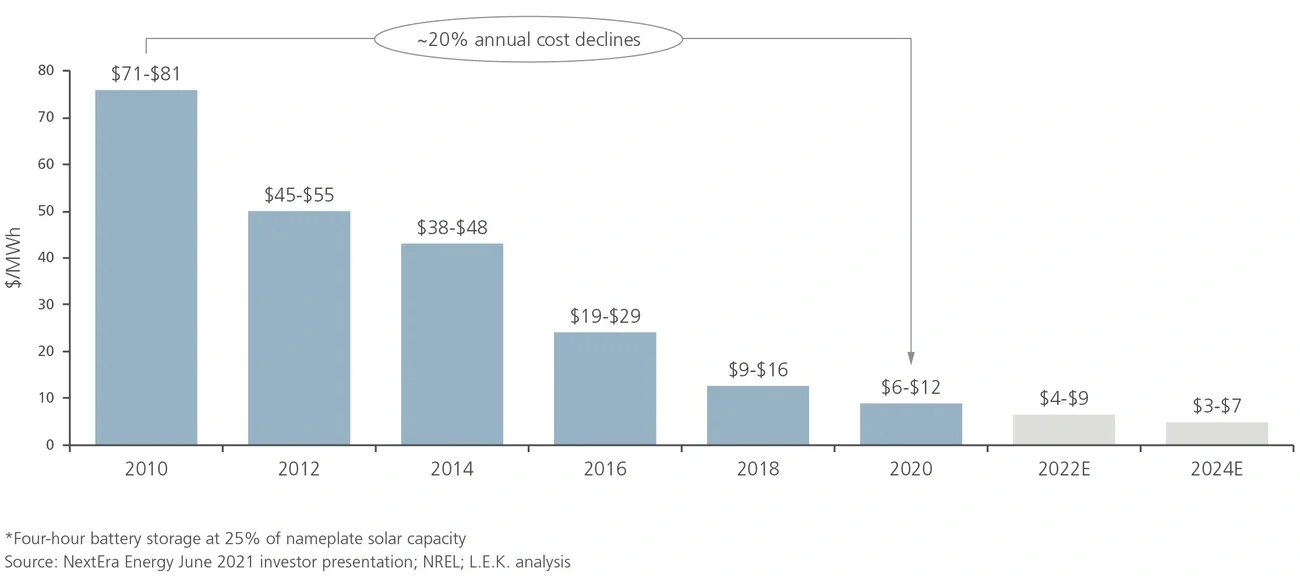

There are a number of energy storage technologies such as pumped hydro, thermal, compressed air and even hydrogen; however, battery-based energy storage — more specifically, variants of lithium-ion technology such as lithium iron phosphate (LFP) and lithium nickel manganese cobalt oxide (NMC) — is emerging as the front-runner and will account for 85% of new MWs added this year.1 Utility and developer comfort with the technology and the inherent flexibility in sizing to the required application are supporting the emerging incumbency status, but the key moat is the cost advantage. Battery energy storage also benefits from scale gained in the electric vehicle market, which has seen investment flow into battery cell, module and pack manufacture. In turn, costs of battery energy storage have fallen by more than 80% over the past decade, and they are projected to fall further.

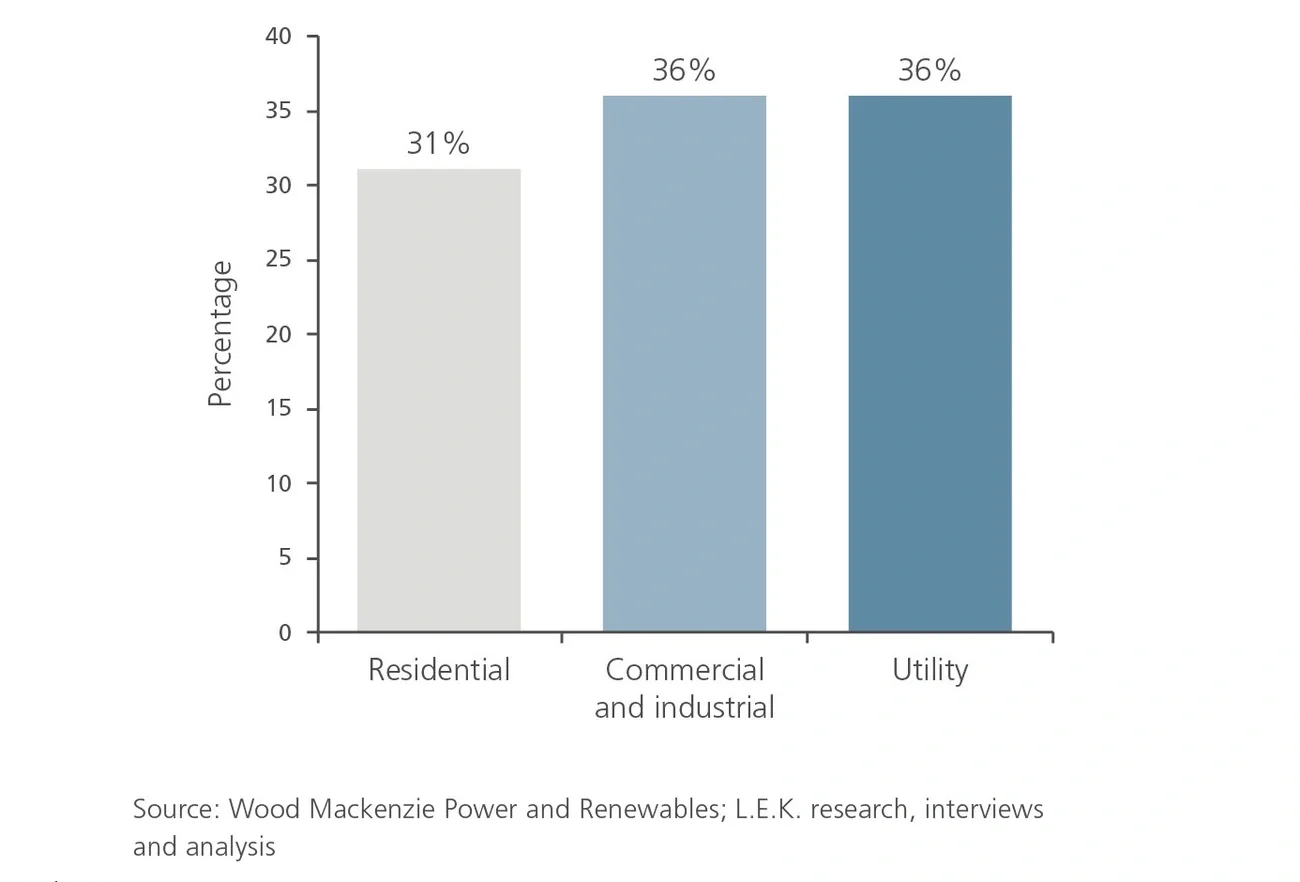

Beyond supporting grid resiliency, battery energy storage’s appeal is also in its extensive set of use cases that unlock value through cost avoidance, loss mitigation and new income streams. For utility-scale applications, battery storage reduces and delays capital-intensive investments in transmission infrastructure, offers a source of backup generation, and captures additional revenue in markets willing to pay for resource adequacy and ancillary grid services. In the residential market, battery energy storage enables homeowners to increase self-consumption of solar assets — and in some markets, sell more power to the utility during high-rate periods — by charging during the day and discharging at night, managing time-of-use around variable electricity rates, and providing backup power for shorter-duration needs. On the commercial and industrial side, value capture is similar to residential and also benefits from demands for cleaner crucial backup power when solar and storage are paired with conventional fuel generators to support hospitals, data centers and other critical infrastructure. Finally, as energy storage reaches a critical mass within utility service areas, utilities will benefit from aggregating disparate systems into a connected virtual power plant that can serve as a low-cost source of generation while avoiding the cost of adding new generation sources.

Perhaps the most critical use case, though, is battery energy storage paired with a new solar installation — whether utility-scale, commercial and industrial, or a residential project — enabling dispatchability for what would otherwise be an intermittent resource. However, this creates a governor for storage demand, in the near term at least, as storage demand is driven in part by new solar demand.