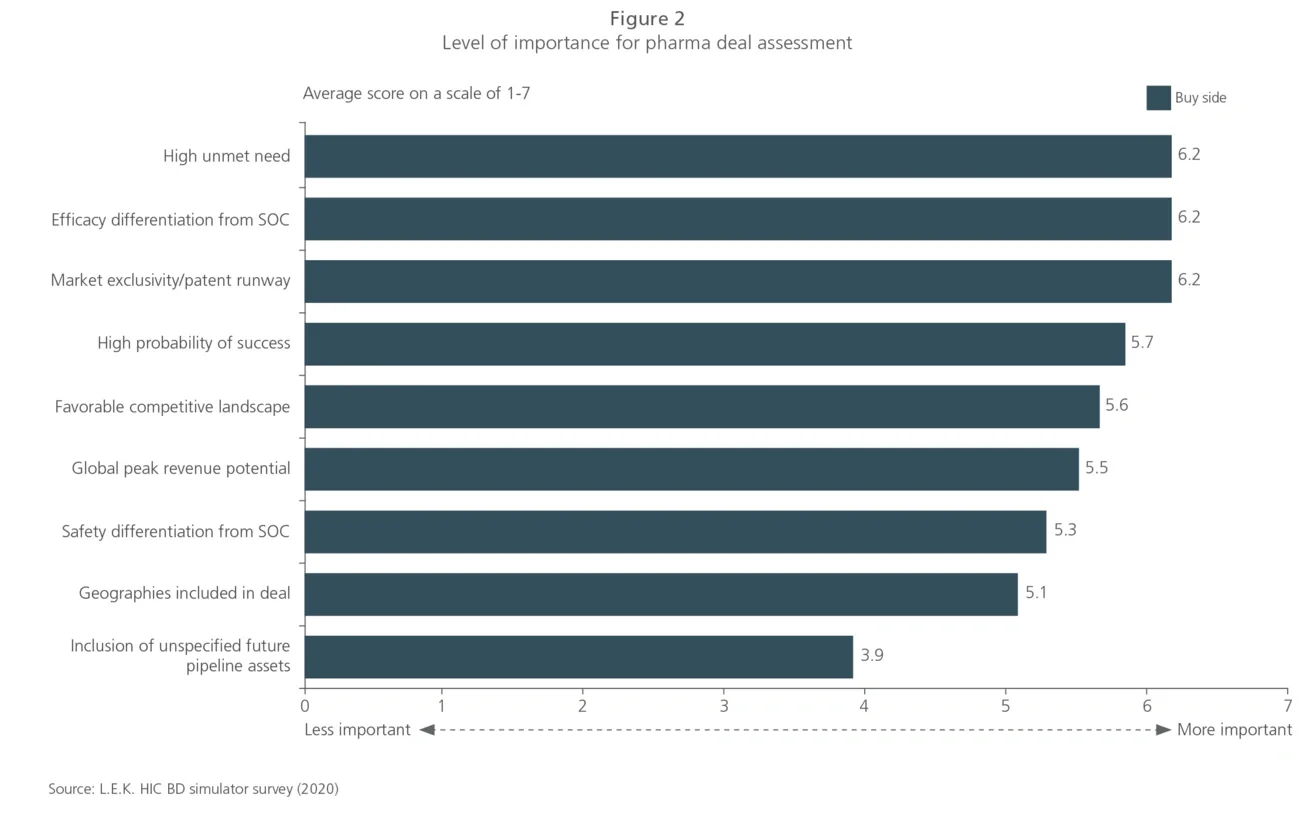

Key factors driving asset value for licensing

As expected, therapeutic areas with high unmet need, market exclusivity and differentiated efficacy over the standard of care (SOC) are among the most important attributes for BD teams considering asset in-licensing. As a sign of the synergy licensing brings, companies that are out-licensing assets rate commercialization capabilities and disease area expertise as key determinants of suitable acquirers. Encouragingly, these complementary expertise areas converge to increase the probability of bringing treatments to patients in need. Factors of greatest importance to buyers during asset evaluation and deal negotiation ― differentiation, high unmet need and exclusive rights — outweigh other considerations (see Figure 2).