Key takeaways

- U.S. infrastructure spending is poised to grow in the long run, as current levels of underinvestment in vital infrastructure systems are unsustainable.

- Infrastructure spending has consistently been resilient during prior recessions and has at times reached prerecession peaks sooner than other building and construction categories; federal intervention has been critical to this pattern during acute recessions, such as the global financial crisis.

- We currently stand at an inflection point, and the federal government’s decision on whether to support infrastructure activity will have a material impact on the shape of the curve going forward.

- Future developments are likely to fall on a spectrum between two scenarios.

- In the first scenario, if history provides the federal government's playbook on infrastructure investment through this recession, there could be a sharp increase in infrastructure spending over the next 18 months.

- In an alternative scenario, in which the federal government refrains from intervening altogether, infrastructure spending would likely be under more pressure than during previous recessions.

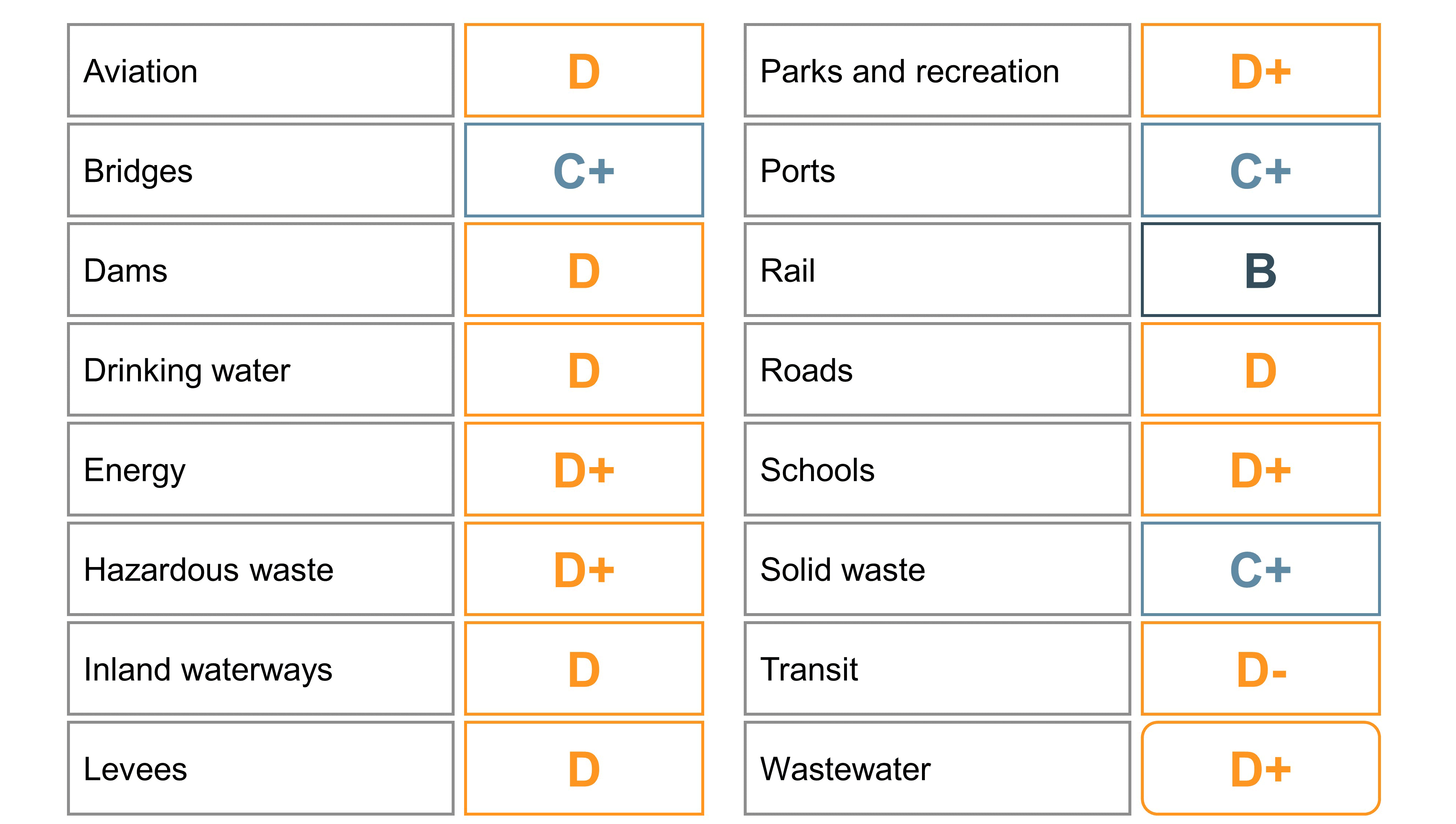

In these times of uncertainty, one thing remains certain: The need for an increase in infrastructure investment is as high as it ever was. The American Society of Civil Engineers (ASCE) has consistently given a D rating to overall U.S. infrastructure quality, with railway infrastructure being the only type of infrastructure ranked above C+ (see Figure 1).

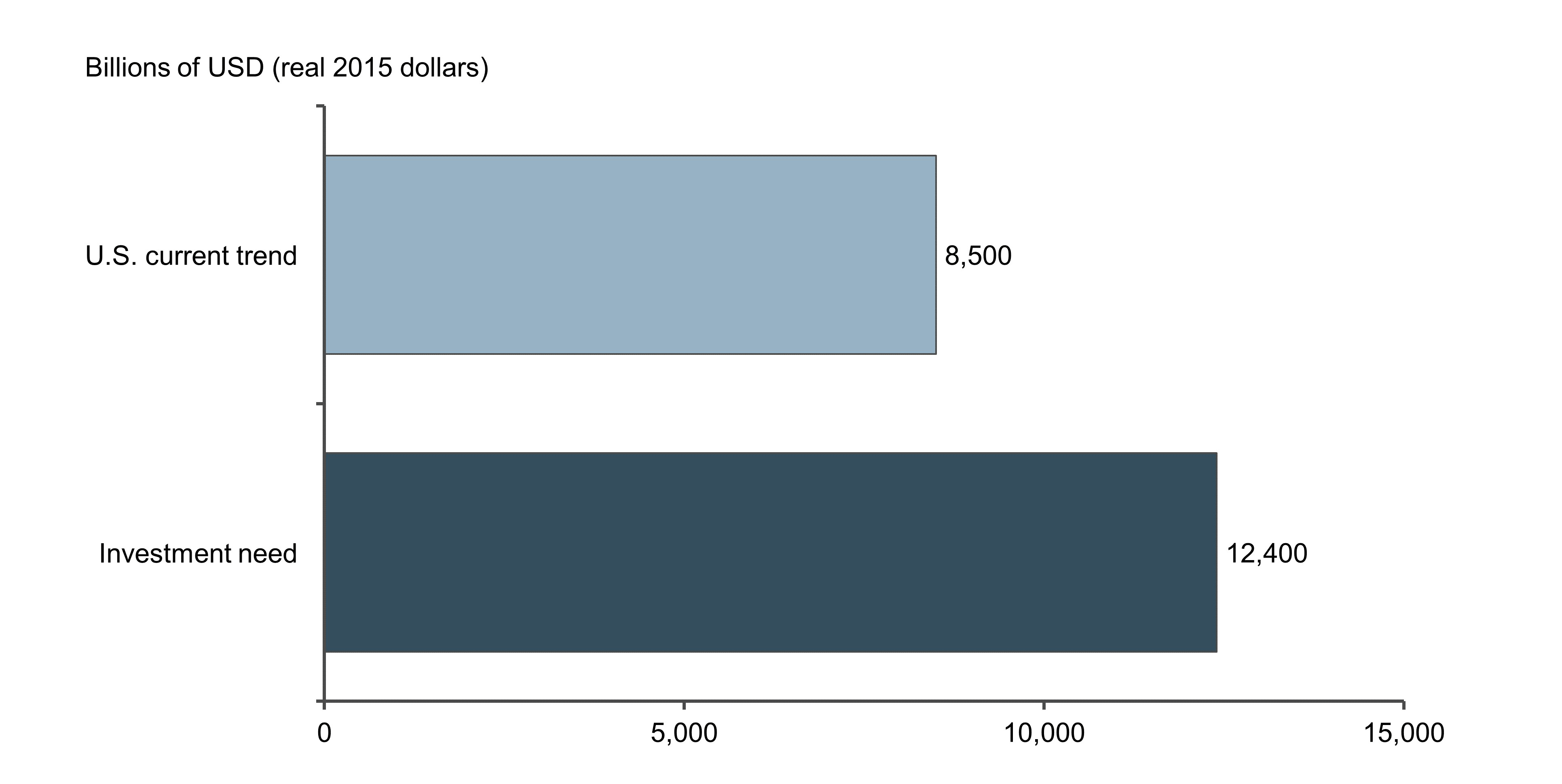

Going forward, Oxford Economics estimates that if infrastructure spending continues to grow in

In other words, current levels of underinvestment are simply not sustainable in the long run, as they would eventually lead to life-threatening failures in vital infrastructure systems. As much as new, high-speed train or urban transit projects can be postponed indefinitely, failing bridges and water systems will ultimately require immediate fixes. This, in turn, points to U.S. infrastructure spending needing to grow in the long term.

Infrastructure spending during and after prior recessions

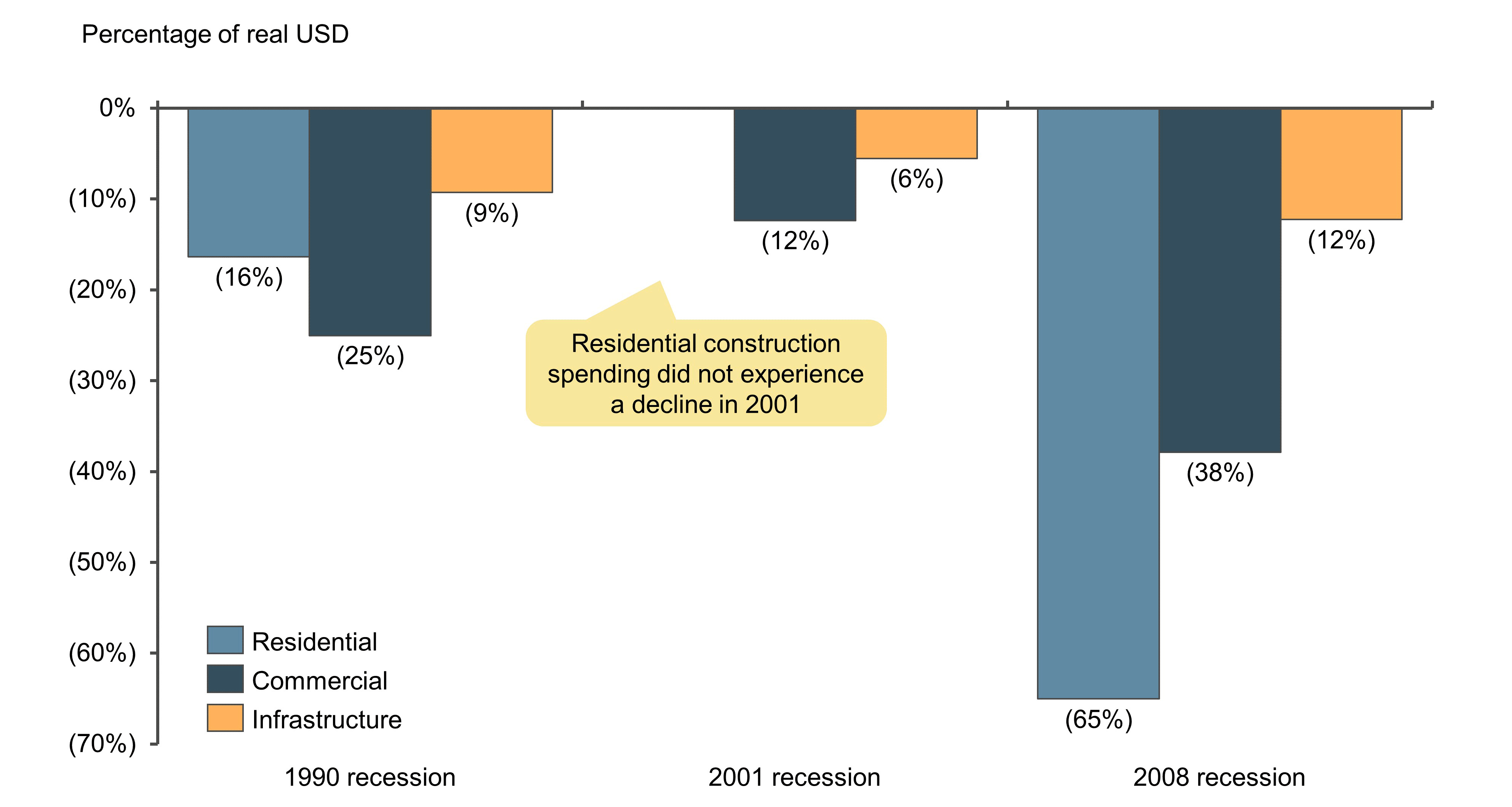

Infrastructure investments have consistently proven more resilient than other types of building and construction categories during prior recessions (see Figure 3).

Figure 3

US construction spend put in place peak-to-trough recession decline, by spend type (1990-2019)

In acute crises, federal interventions are critical because state and local governments are under an obligation to balance their budgets. Without federal support, they would typically have to cut down on all discretionary spending — including infrastructure — in the short term.

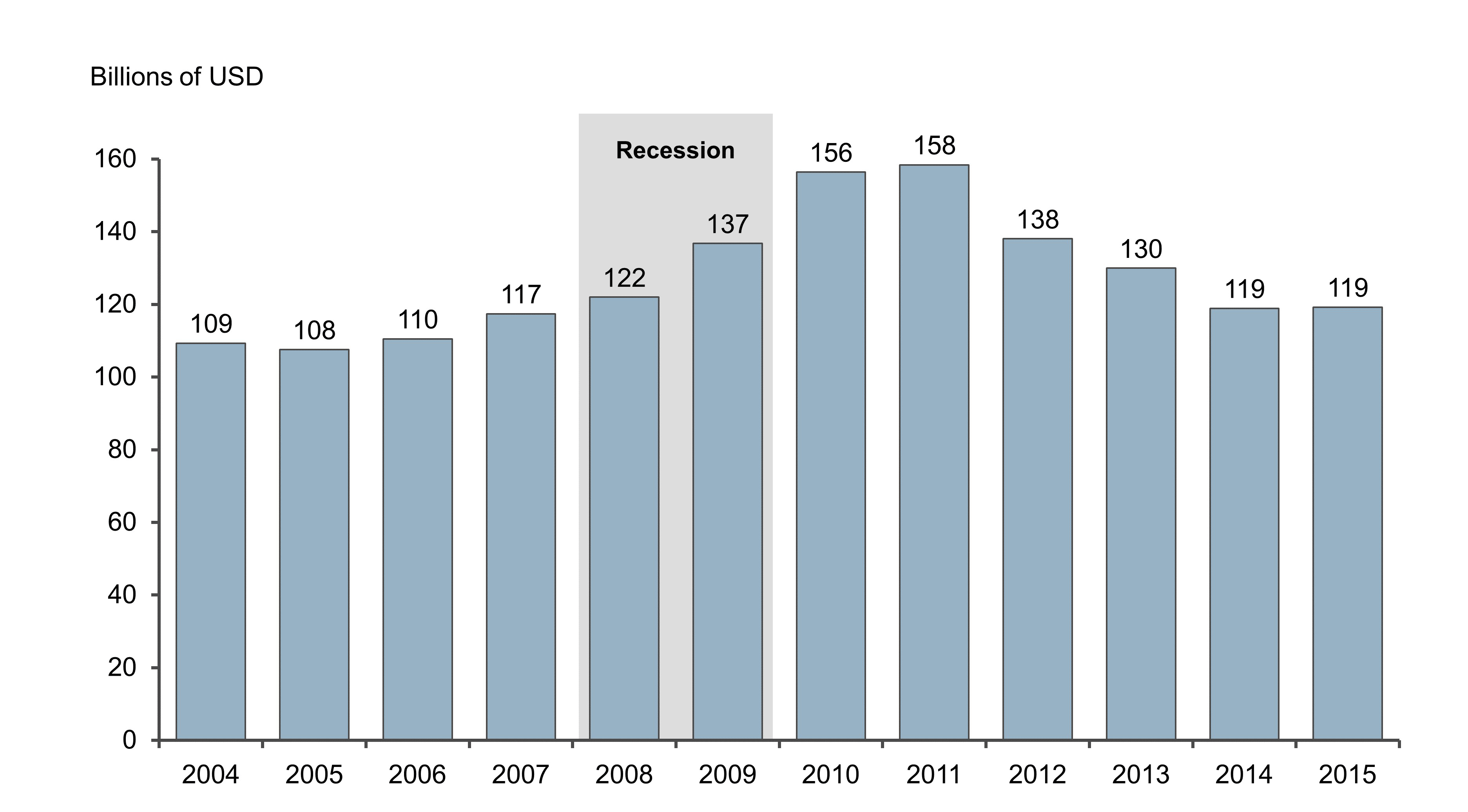

In the case of the 2008 recession, the relative stability of public infrastructure spending was made possible by a significant intervention by the federal government, the American Recovery and Reinvestment Act of 2009 (ARRA), which allocated ~$105 billion to infrastructure projects. About two-thirds of overall ARRA investments were made from 2009 to 2011, with a peak in 2010.

As a result, federal investment in infrastructure reached an annual average of ~$147 billion1 from 2009 to 2012, compared to an annual average of ~$114 billion over the 2003-2008 period (an approximate 30% increase, while private spending across residential and commercial building and construction declined by 55% and 15%, respectively, on average per year during that same time period). This largely explained the resilience in public infrastructure investment during the global financial crisis, as the increase in federal investment compensated for the financial difficulties of state and local governments. After that surge, federal investment receded to close to its prerecession levels, reaching an annual average of ~$119 billion from 2013 to 2018.

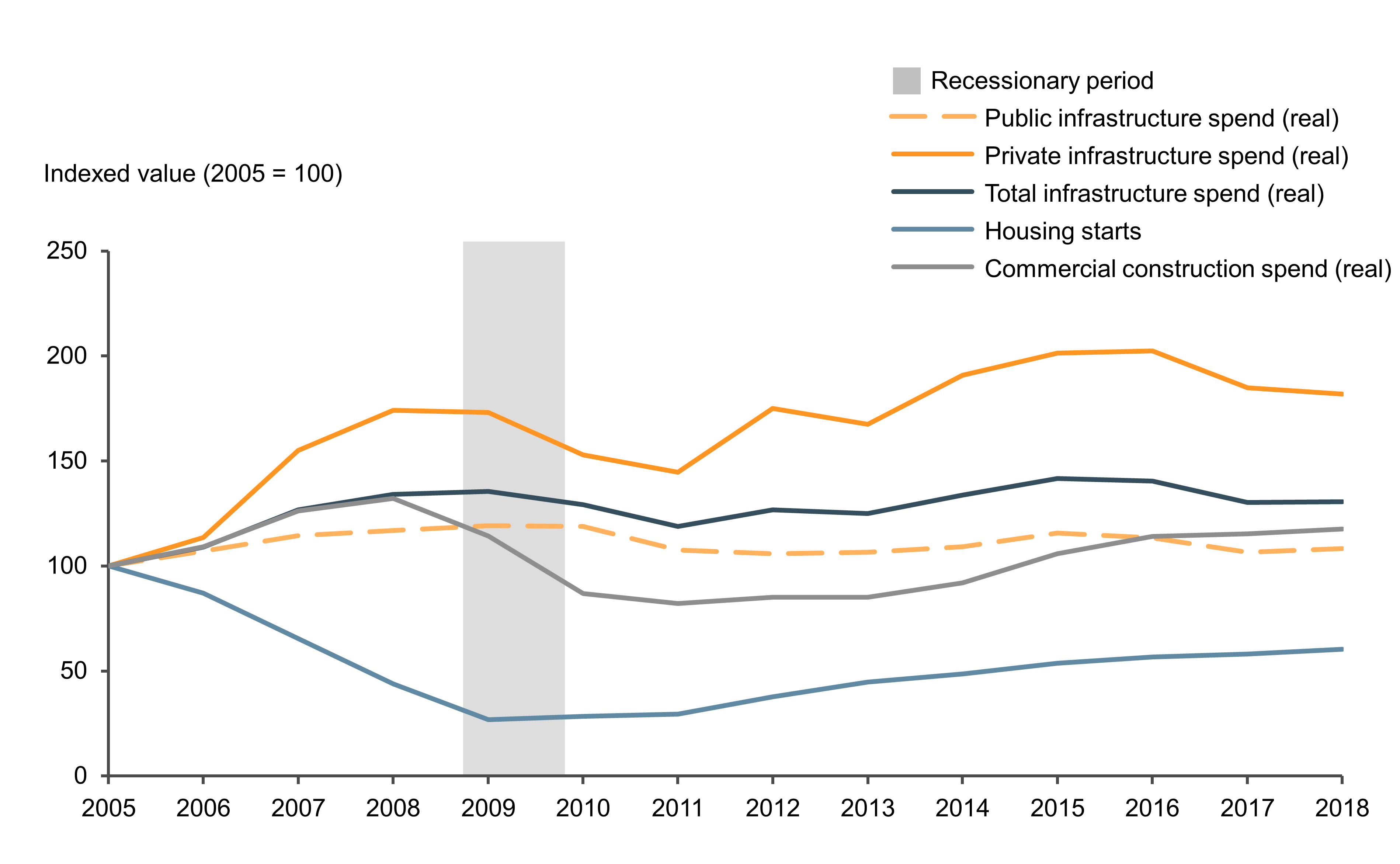

After the 2008 recession, overall infrastructure spending also reached prerecession peaks sooner than other spending categories, through the combination of 1) a slight increase in total public investment, starting in 2013, and 2) a sharp recovery in private investment, starting in 2012 (see Figure 4).

Current environment and possible scenarios

To date, infrastructure construction has been considered a critical activity and exempted from stay-at-home orders in a majority of states — including states where some building and construction projects are not exempt from stay-at-home orders.

As an example, Washington state has excluded transportation and energy projects from its otherwise strict stay-at-home order among exceptions for “construction related to essential activities like health care, transportation, energy, defense and critical manufacturing; […] construction to further a public purpose related to a public entity.”

The fact that very few infrastructure projects have been stopped so far suggests that if it were to happen (see our range of scenarios in Figure 5), a possible slowdown would likely occur later in 2020.

Figure 5

US construction restrictions by state

Federal interventions to support infrastructure spending have, however, remained very limited so far. They have primarily taken the form of financing support through the Federal Reserve’s unprecedented decision to purchase municipal bonds. Direct federal investment in infrastructure through the CARES Act has been mostly focused on ensuring the continued operation of critical infrastructure such as airports.

Future developments are likely to fall on a spectrum between two scenarios:

- Scenario 1: As it has in past cycles, the federal government intervenes and injects stimulus investment into infrastructure — either directly or by supporting the ability of state and local governments to invest in infrastructure.

- Scenario 2: The federal government refrains from supporting infrastructure spending.

Although the ultimate decision of the federal government is anyone’s guess, understanding the implications of these scenarios is an important exercise — and one that highlights the criticality of a potential federal intervention to the future of the industry.

Scenario 1: The federal government steps up

While the specifics remain uncertain, if history provides the federal government’s playbook on infrastructure investment through this recession, there could be a sharp increase in infrastructure spending over the next 18 months.

The infrastructure package that is currently being debated would exceed ~$2 trillion, compared to an average ~$119 billion annual federal infrastructure investment from 2013 to 2018 and broken down as follows:

- ~$800 billion in reauthorizations (~$600 billion in 10-year Highway Trust Fund reauthorization plus ~$155 billion in Federal Transit Administration reauthorization)

- ~$200 billion in “emergency/stimulus” funding

- $1.1 trillion-$1.3 trillion in private spending estimated as a result of the emergency/stimulus funding (also referred to as “leveraged” spending)

In total — and if leveraged private spending materializes as planned — this package would amount to $1.3 trillion-$1.5 trillion in additional infrastructure spending (the combination of emergency/stimulus funding and private spending), likely to be spread over several years. As a point of comparison, the U.S. Census Bureau reported total infrastructure put in place to be ~$300 billion in 2018 (~60% in public spending and ~40% in private spending).

Stimulus spending would not go to construction investment only, as the operation of critical infrastructure may require urgent federal support. Nevertheless, a total spending increase of $1.3 trillion-$1.5 trillion would generate very significant tailwinds for the industry.

If voted on rapidly, this infrastructure package could start generating significant additional investments in mid-to-late 2020. The ARRA stimulus package, established in February 2009, led to a 12% increase in federal investment during that same year, before federal investment peaked in 2011 (see Figure 6).

In the event of a significant federal intervention, contractors and building material manufacturers most exposed to infrastructure spending would likely fare better than other categories of construction players.

Scenario 2: Spending bucks the historic precedent and no federal investments are made

Although historical precedent suggests that some form of federal intervention is a likely outcome, there is also a possibility that the federal government will refrain from intervening altogether. In that scenario, infrastructure spending would likely be under more pressure than during previous recessions, for several reasons.

First, state and local government budgets could be likely to see 1) a sharp decrease in tax revenues (particularly gas taxes, which are critical to infrastructure financing), 2) cash management challenges due to delays in tax collection, and 3) an increase in healthcare-related expenses. Full-year reforecasts or budget adjustments have not yet been published, but as an example, New York state currently estimates a $10 billion-$15 billion budget shortfall as a result of COVID-19. Similarly, New York City announced on April 16 a revised 2020 budget that was $6 billion lower than its original budget and included cuts to core services such as public sanitation and public safety.

With all the CARES Act spending being earmarked for specific purposes (e.g., healthcare spending, supplementary unemployment help), the federal government would not compensate for this general budget shortfall.

Being under the obligation to have balanced budgets, state and local governments would then likely be forced to cut discretionary spending — including nonurgent infrastructure projects. As of April 7, the nonpartisan American Association of State Highway and Transportation Officials estimated that ~$50 billion would be necessary to offset the loss of state transportation revenues over the next 18 months. This amount points to a much larger overall infrastructure funding shortfall, as it includes only road transportation spending (exclusive of all other infrastructure categories) for the purpose of replacing planned investments (not to finance new projects) at the state level (exclusive of local government budget shortfalls).

In addition, private investment in the energy infrastructure sector is also likely to decrease as a result of low oil prices (utilities are expected to be relatively resilient in spite of lower electrical usage and a potential increase in bad debt, but oil-and-gas-related investments are expected to decrease sharply).

Assessing the magnitude of a potential decline in infrastructure spending in the absence of federal intervention is made challenging by the lack of recent historical precedent.

What can be said for certain, however, is that we stand at an inflection point, and the federal government’s decision on whether to support infrastructure activity will have a material impact on the shape of the curve and the implications for value chain participants, from upstream material producers to downstream service providers.

Endnote:

1Congressional Budget Office (CBO) — based on federal investment in nondefense physical capital

01052022150119