Key takeaways

-

We expect that repair-and-remodel (R&R) and the retail channel will outperform other sectors of residential construction — early indications are that they are already doing so.

-

Building products manufacturers need to adapt their go-to-market approaches to serve more-resilient and relatively higher-growth segments.

-

Manufacturers exposed to retail can enhance their marketing programs (e.g., in the digital category, professional solutions such as product selectors) and level of retail partnership.

-

R&R-exposed manufacturers with less retail exposure can enable pro contractor customer sales activities to deliver product and program enhancements that enable their contractors to close and drive more sales.

The building and construction industry is experiencing a downturn overall, but some sectors will prove to be more resilient, as outlined in the April 7 article, COVID-19: Which Building and Construction Segments Can Weather the Storm? Two of those more resilient segments — R&R and retail — are worth exploring in more detail, with implications for building products manufacturers.

The record of R&R and retail

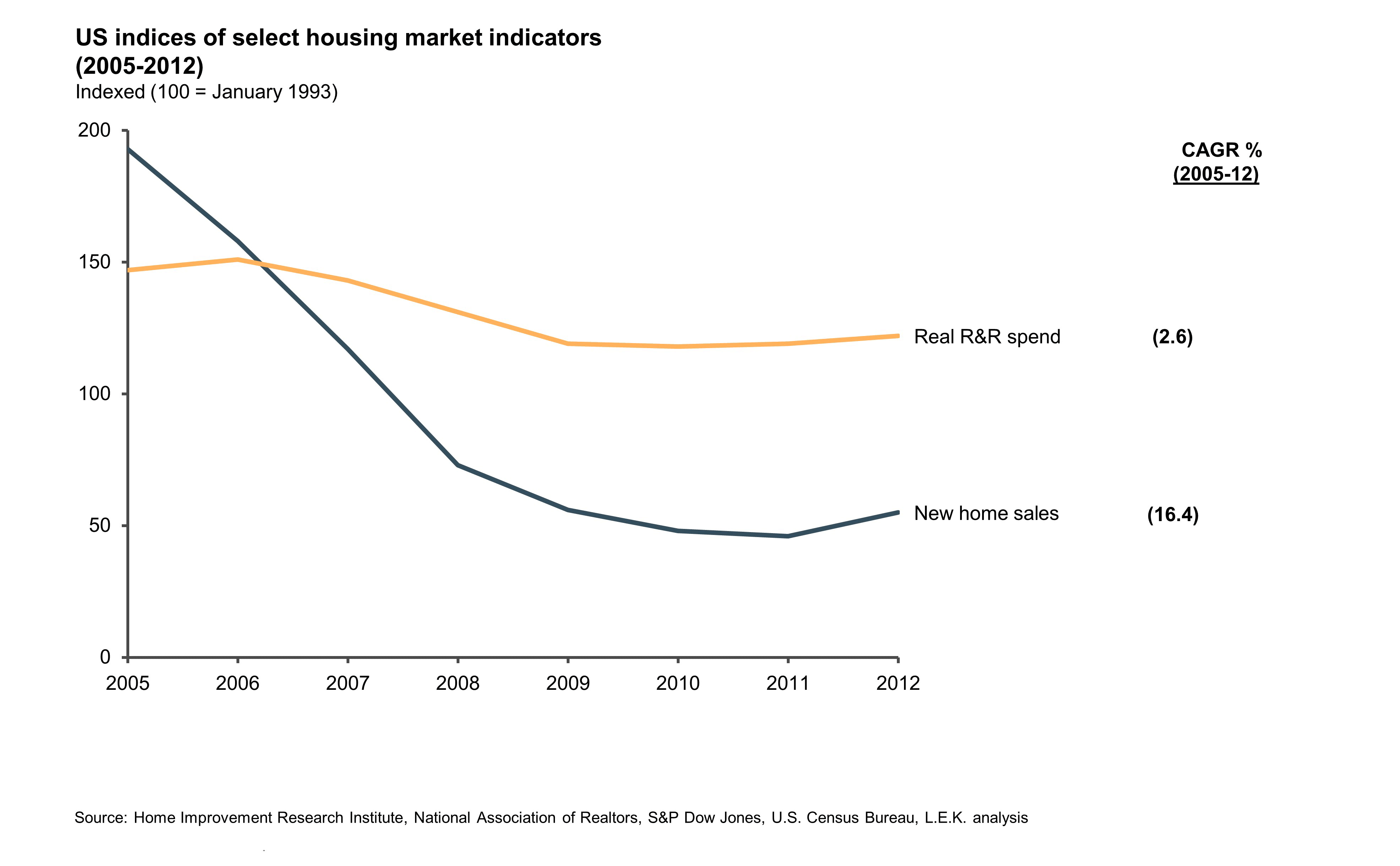

Historically, R&R has outperformed new construction in a recession (see Figure 1).

R&R is more resilient than new construction because homeowners consider many small repairs as essential and immediate.

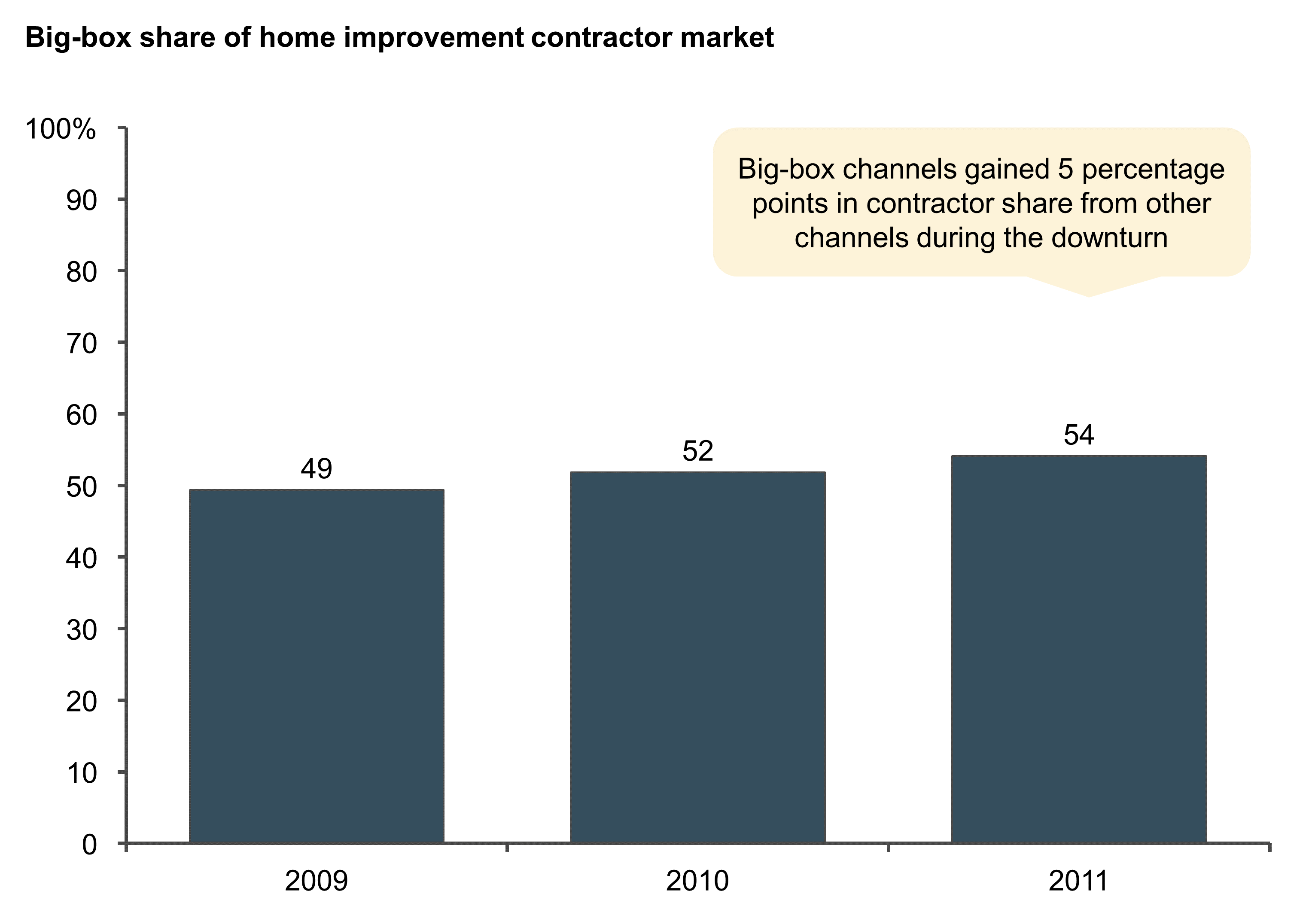

Similarly, retail has also shown historical resilience. In the last recession, big-box retail experienced a gain in share within the contractor segment (see Figure 2).

What is the outlook for R&R?

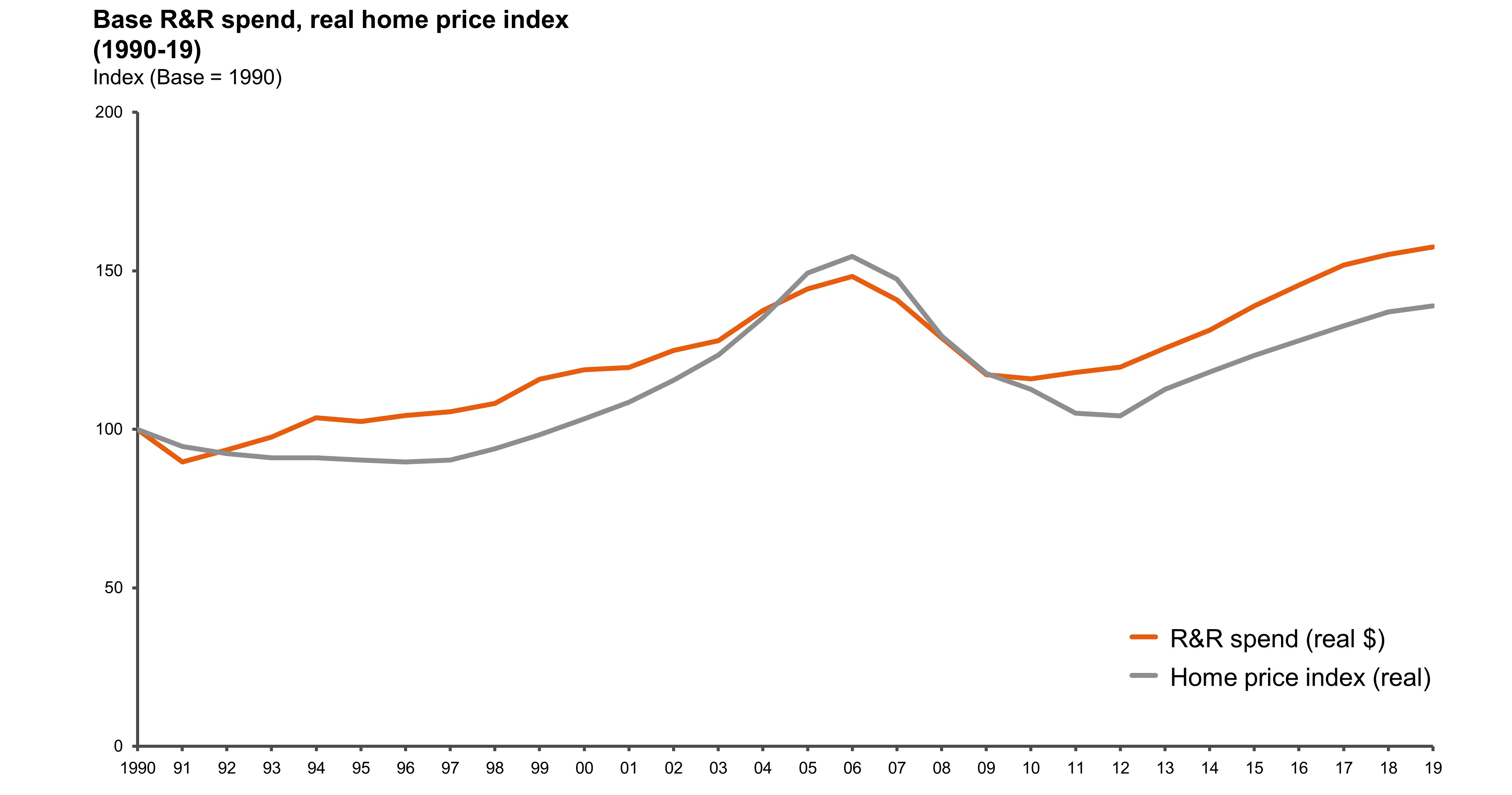

How is R&R likely to perform in 2020? R&R has tracked home values historically (see Figure 3). While there are other factors that also influence R&R (e.g., existing home sales, HELOC rates), home prices are a critical factor. As the COVID-19 crisis unfolded, many builders have not appeared to reduce their prices. According to Myers Research, 72% of builders did not initially reduce prices, perhaps because March listings fell by 34% compared with the prior month. The experience from 2008 shows that house prices can fall when there is income contraction and that the potential impact will likely vary considerably by geography. Understanding the likely performance of R&R requires keeping a close watch on home prices at the local and national level.

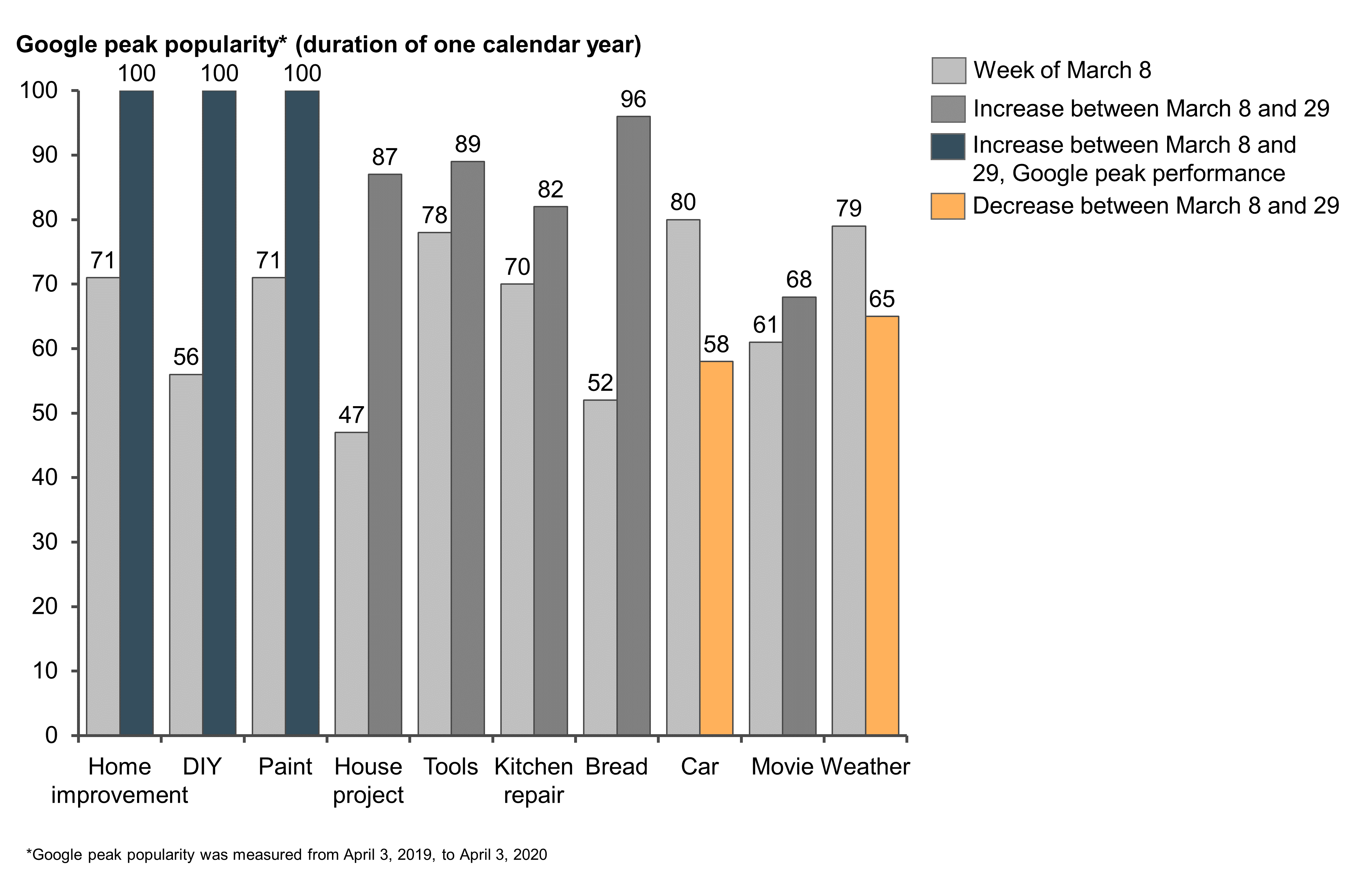

Most commentators expect a decline in R&R demand. Nevertheless, as homeowners have been spending more time at home, they are giving more thought to their homes. Media and web searches signal homeowner interest in R&R planning, once markets have stabilized. Equally, consumers are interested in do-it-yourself (DIY) activities for high-utility improvements around the house, especially with stay-at-home orders in place for 317 million Americans.1 Home and renovation magazine subscriptions on Readly are up 24% since last month and 6% since this time last year. Terms such as “home improvement” and “DIY” are at a “peak” level of Google searches (defined as the most a term has been searched over the prior year). While other searches reflecting household interest have also increased, home improvement has been particularly high (see Figure 4).

Beyond web searches, early indications are that R&R is performing relatively well. As an illustration, one lumber company reports experiencing a stream of business in DIY product categories and attributes it to people seeking to take advantage of the time they’re spending at home by investing in home construction projects.

Retail in 2020 and current indications of performance

Although home improvement and hardware stores have been deemed “essential” businesses by state governments across the country, big-box retailers such as Lowe’s and The Home Depot have reduced store hours and set limits on the number of customers allowed inside a store at any given time.

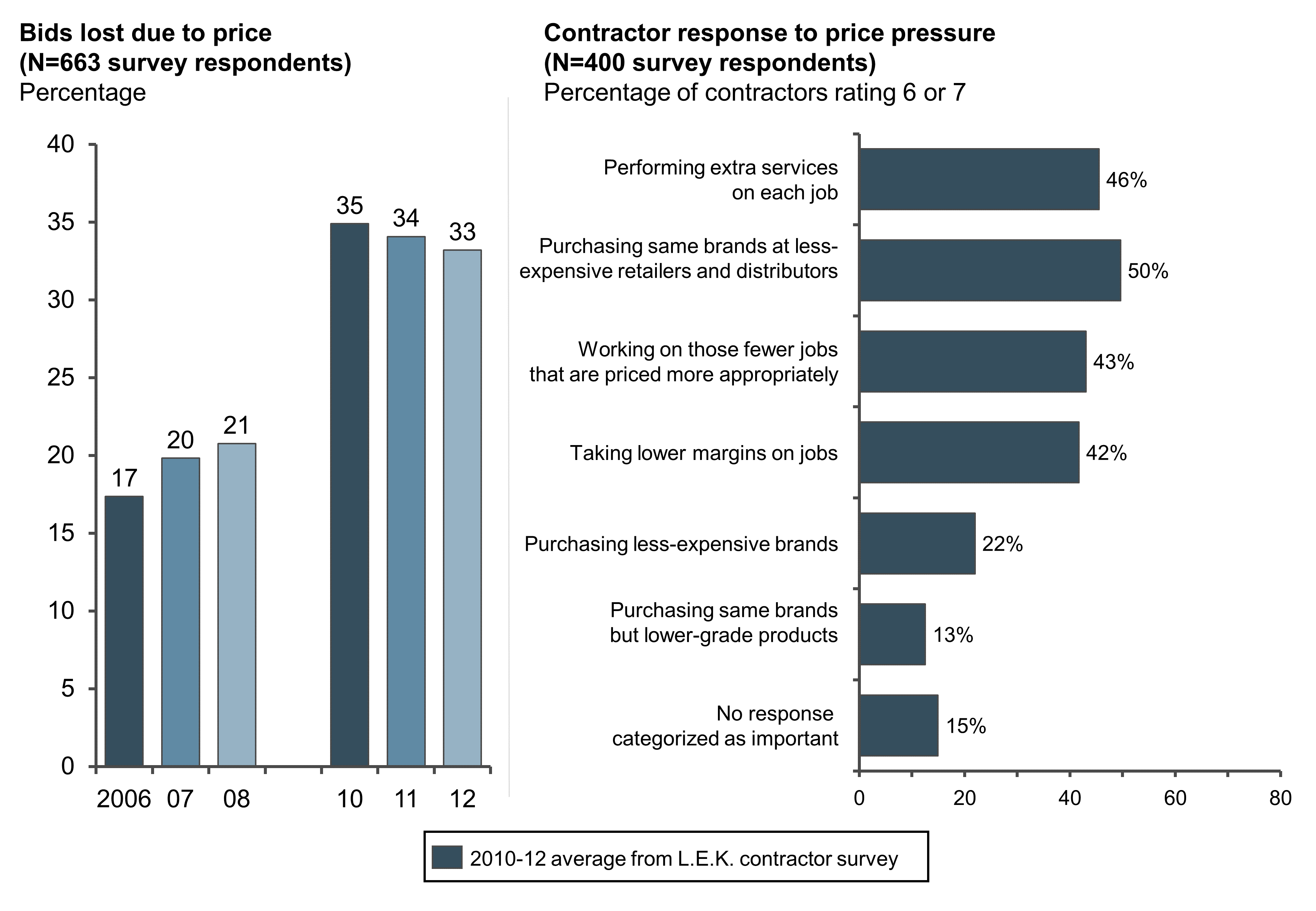

Despite the challenging stay-at-home and social distancing guidelines, the retail channel appears relatively well positioned to succeed in this environment, factors borne out through L.E.K.’s proprietary contractor survey, which has been conducted since 2010. During the Great Recession, many contractors put less premium on value-added services, given that their workloads had decreased. Rather than relying on value-added distribution, some contractors preferred to group, buy and transport materials to construction job sites themselves. Contractors were also more willing to bid for jobs across categories and to “trade down” from larger new construction projects to smaller R&R projects. The broad category offerings and competitive pricing of big-box retail made this channel ideal for supporting contractors’ needs. In addition, during a recession, contractors face more competition and find themselves competing on price, driving them to elevate material costs in their purchase criteria and seek better prices across channels, as L.E.K.’s contractor survey showed (see Figure 5).

As a result, as stated in Lowe’s 2009 annual report, “Customers continued to focus on routine maintenance and repairs instead of larger discretionary projects during fiscal 2009. We experienced solid sales performance in paint and nursery as a result of the continued willingness of homeowners to take on smaller do-it-yourself projects to maintain their homes and improve their outdoor space.” John Burns Real Estate Consulting showed a decline in average spending per homeowner R&R project from 2006 to 2012, while smaller projects, after declining slightly between 2007 and 2009, showed much more resiliency.

This dynamic of retail share gain through R&R played out after 2008, and there is every reason to believe that the dynamic could replay in 2020, magnified by the impact of online investments by big-box retail that foster an even greater connection between big-box stores and end customers. For instance, The Home Depot has committed to a $1.2B investment through 2023 to enable faster online order pickup and 90% U.S. coverage for same- or next-day shipping.

The early indications are that retail is performing relatively well. Lowe’s CEO Marvin Ellison recently said, “As customers are sheltering in place, they’re looking at that deferred list of home projects. As they spend time around the home, they now have more time on their hands to tackle some of those things.” Ellison noted that Lowe’s has seen an increase in sales across nearly every category as customers stock up on supplies for DIY home projects. Some small hardware stores have also seen an increase in sales. As an illustration, Alain Mongeon, store manager of Aubuchon’s, commented, “Generally, this time of year we have an increase in business anyway because of the spring, but this is just on top of that. You can order online and have curbside pickup — that business has jumped 98%.”3 Mongeon cited paint, plumbing and electrical supplies as being particularly popular.

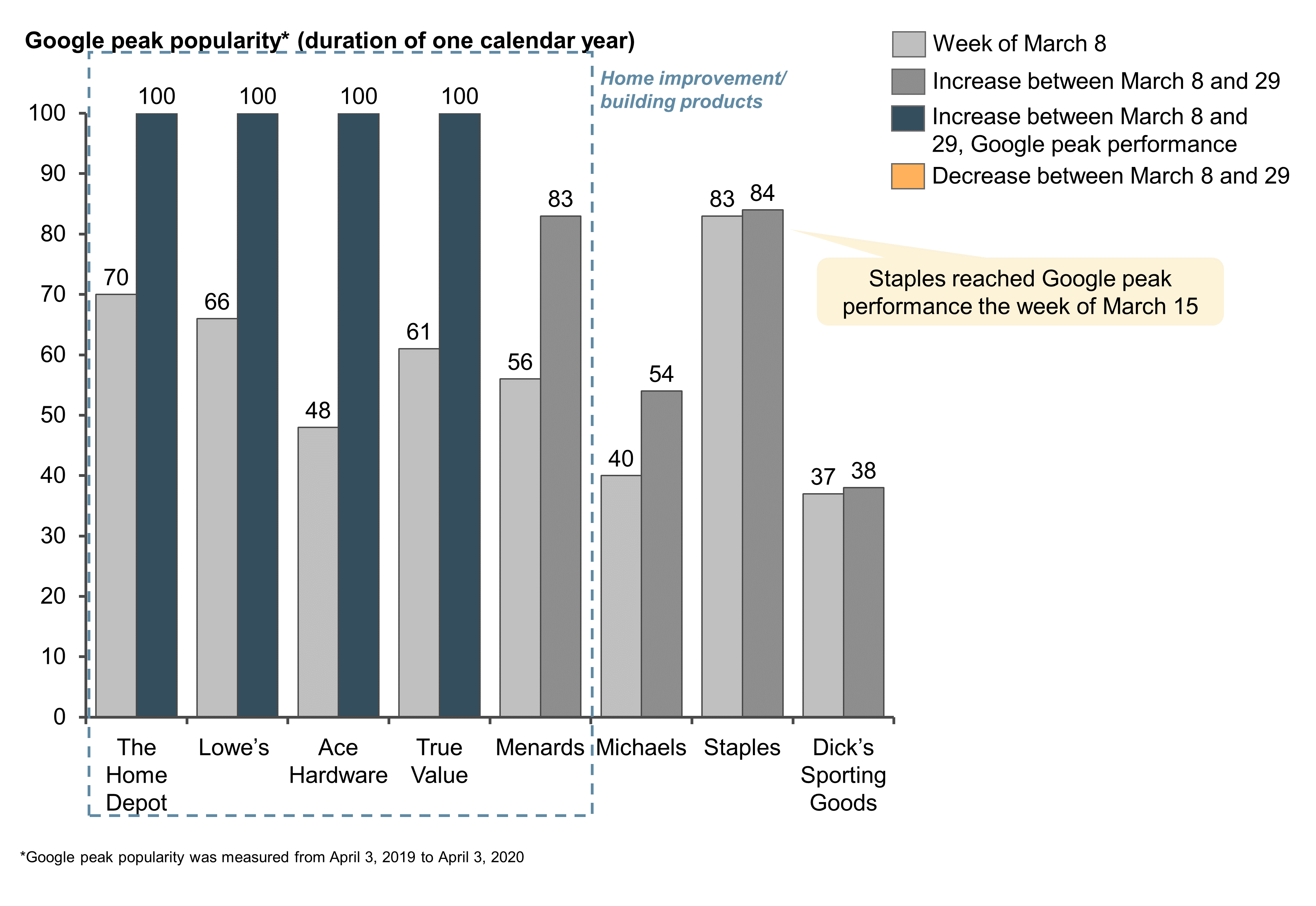

Media and web searches also show relatively strong retail performance. “Consumer purchase intent mentions” are up 75% year-over-year for The Home Depot and 55% year-over-year for Lowe’s.4 Home improvement retailers are now outperforming other retailers at peak popularity levels (see Figure 6).

Some favorable tailwinds for the big-box channel were not as present in 2008. Since the onset of COVID-19, consumers have been spending more time in their gardens and working at home. The outdoor living and home office categories may grow, given that, according to the Home Improvement Research Institute (HIRI), 64% of landscapers use the retail channel as their primary supplier. Other categories (e.g., lighting) could also potentially perform well if more homeowners accommodate space for home offices, a category where big-box retail has a significant presence.

We may also see an increased shift from do-it-for-me to DIY. Homeowners with less income, and in some cases more time, will be more ready to perform home improvement work themselves and to source the materials from a retail store. HIRI found that 66% of those earning between $50,000 and $99,000 per year are DIYers, compared with only 56% of those earning more than $100,000 per year.

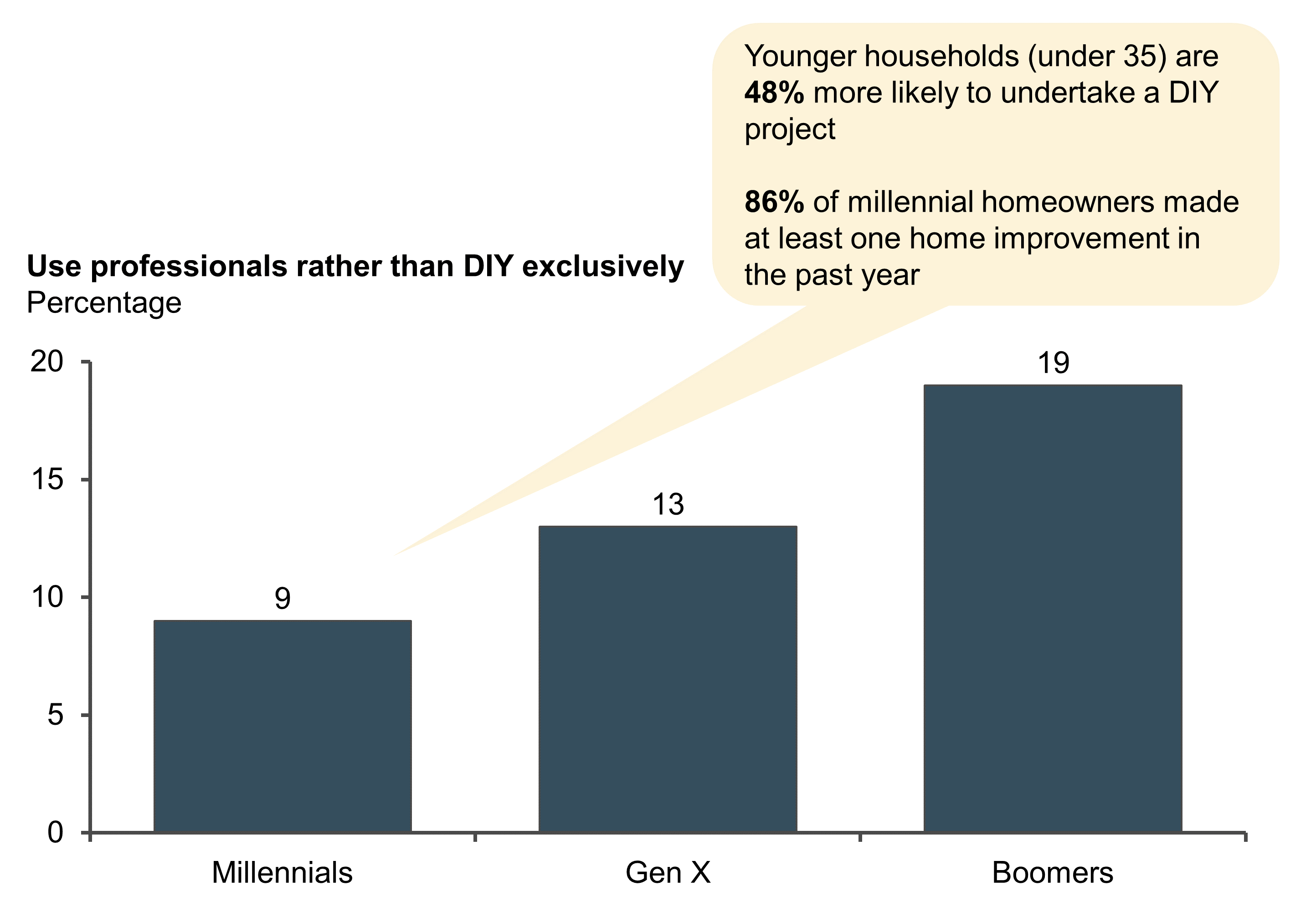

Generational changes could also be a factor. Millennials are now the generation driving household formation. While millennials have shown a willingness to outsource services, such as home improvement, they are now more aligned to the profile of DIY engagement. Millennials are financially insecure, exacerbated by the recession, prone to using self-instruction media (34% of those born between 1980 and 1989 say they perform more DIY after watching YouTube videos[1]), and desire an authentic experience and lifestyle. Hence, as more millennials become homeowners, the current situation could drive them to increase their use of DIY. (see Figure 7).

With a network of partnerships to deliver powerful upstream content, home improvement retailers have the scale to take advantage of millennial needs and play a central role at the intersection of ideation and execution for these DIYers.

Implications for building products manufacturers and distributors

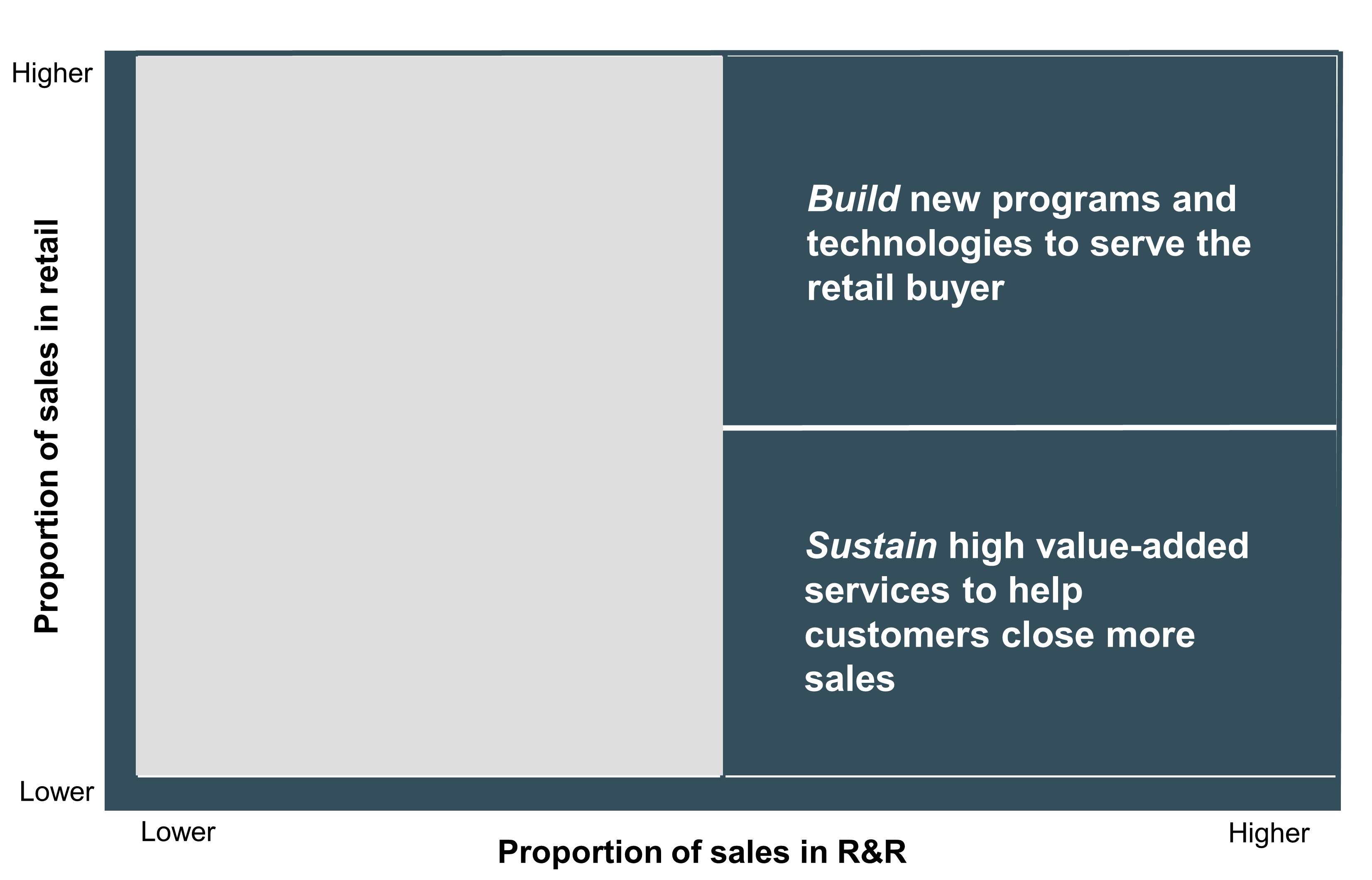

The potential shift in business to R&R and the retail channel, as well as a potential increase in DIY, has implications for building products manufacturers, as well as for distributors that sell into and distribute for big-box stores such as Lowe’s and The Home Depot (e.g., special-order items). As such, manufacturers and distributors should consider the following strategies (see Figure 8).

Figure 8

Manufacturer and distributor strategies to address outperformance of R&R and retail sectors

Manufacturers and distributors that are more exposed to retail and R&R need to build new programs and tools to serve the retail buyer. The goal for manufacturers in this space is to determine how best to serve these smaller contactor customers in a recession through marketing, programs and/or partnership.

- Sharpen the digital messaging — Manufacturers and retailers with traction online can leverage their digital footprints and understanding of customer (and consumer) segmentations to tailor each step in the digital customer experience — from idea generation and research to product selection and purchase, and even within installation support and post-sale services. For example, educational content and greater information give homeowners confidence in the product and DIY project. Kitting (packages, bundles) is another method to nudge purchases. Some manufacturers will need to “up their game” in digital marketing and education to the standards of some of the leading brands. For example, Cambria, a quartz countertop manufacturer, has best-practice images that show the texture of its quartz, as well as engaging videos. Digital processes and online education will move from being a necessary service to a key factor in vendor selection.

- Build/adapt programs to serve the retail customer — Manufacturers need to ensure that they are building loyalty programs tailored to retail customers in recessionary times. For instance, rather than encouraging product trade-up or retail-installed sales, a manufacturer may want to preserve loyalty with its base products. Manufacturers and distributors can determine ways to support a next-generation retail offering for pro contractors that leverages technology for digital takeoffs and coordinates inventory and delivery.

- Address customer cash flow — DIYers and small professional contractors are more likely to have cash flow issues in a recession. There may be an opportunity for manufacturers to be of some assistance, perhaps through partnership with fintech companies that work with manufacturers to provide financing to small businesses (e.g., On Deck Capital) when a manufacturer is interacting directly with end customers. By leveraging data analytics to make better lending decisions, these companies can reduce credit risk in a recession.

- Enhance retail partnerships — In a recession, big-box retailers need their vendors to bring new ideas that can grow manufacturer as well as big-box business. Where might these ideas come from? Forward-thinking manufacturers and distributors need to grasp one or two trends and convert them into suggested programs that can help grow retail sales. Other manufacturers will need to expand their partnerships with retail third parties. For example, The Home Depot worked with the design firm WD Partners to help develop a new store design,6 and in 2018 it announced a partnership with Women Who Code to develop initiatives that support the growth of women engineers and technology leaders at local and international levels.7 These are just two examples of the range of big-box partnerships that manufacturers and distributors can leverage and support to drive joint business.

Manufacturers more exposed to R&R but less exposed to retail need to sustain high value-added services to help customers close more sales. Manufacturers in this space may still experience a decline in R&R sales and their contractor customers might be finding it harder to close sales. Manufacturers’ goal should be to help their customers maximize closed sales.

- Deliver product innovation that differentiates contractors — Manufacturers can focus on innovations that help their customers stand out. That might be through new features or through customization. For instance, Vent-A-Hood, a manufacturer of premium ventilation solutions, implemented building information modeling and a 3D rendering platform to allow customers to customize their ventilation hood while staying within the parameters of architectural design.8

- Pursue financing — Manufacturers and distributors may want to rely more on financing solutions to help consumers spread the cost of “big ticket” building projects. After the Great Recession, there was increased conservatism from banks toward homeowner financing, while at the same time many consumers were more cautious about borrowing. Over the past few years, financing has grown and new lending platforms have emerged (e.g., GreenSky partners with manufacturers to provide homeowner financing programs through the contractor). These financing programs are likely to continue, giving manufacturers and distributors a lever that was less available in the last recession. Manufacturers and distributors may even choose to get involved in lobbying efforts for government-backed lending facilities.

- Explore new channels — Some manufacturers are partnering with online providers to connect with homeowners directly, often through lead generation programs in project-centered categories (e.g., replacement windows, R&R siding and gutters, reroofing), providing an opportunity that all manufacturers, and potentially distributors, can explore.

Conclusion

R&R and the retail channel are likely to outperform the rest of the building products and construction sector. As the new recession takes hold, manufacturers and distributors can adapt their go-to-market approaches to the new reality.

Endnotes:

1Myers Research, April 15 webinars

2The New York Times, as of April 7

3Wicked Local

4Ameritrade

5John Burns Real Estate Consulting

6WD Partners

7Women Who Code

8Autodesk.com

01052021090154