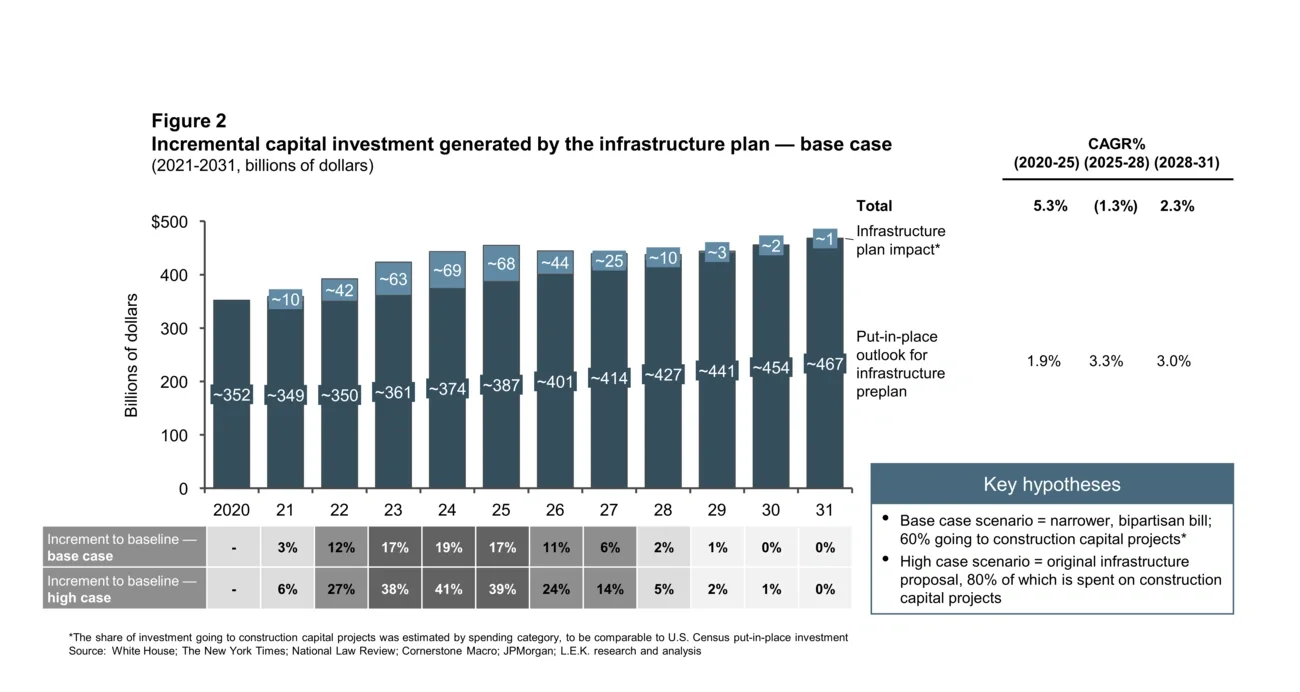

The magnitude of the U.S. infrastructure plan, which was passed in November 2021 — $550 billion, front-loaded over 2022-25 — is without precedent in modern history. It comes at a time of very strong residential demand and recovering commercial construction. Combined, these factors amount to an extremely robust demand outlook in the building and construction industry.

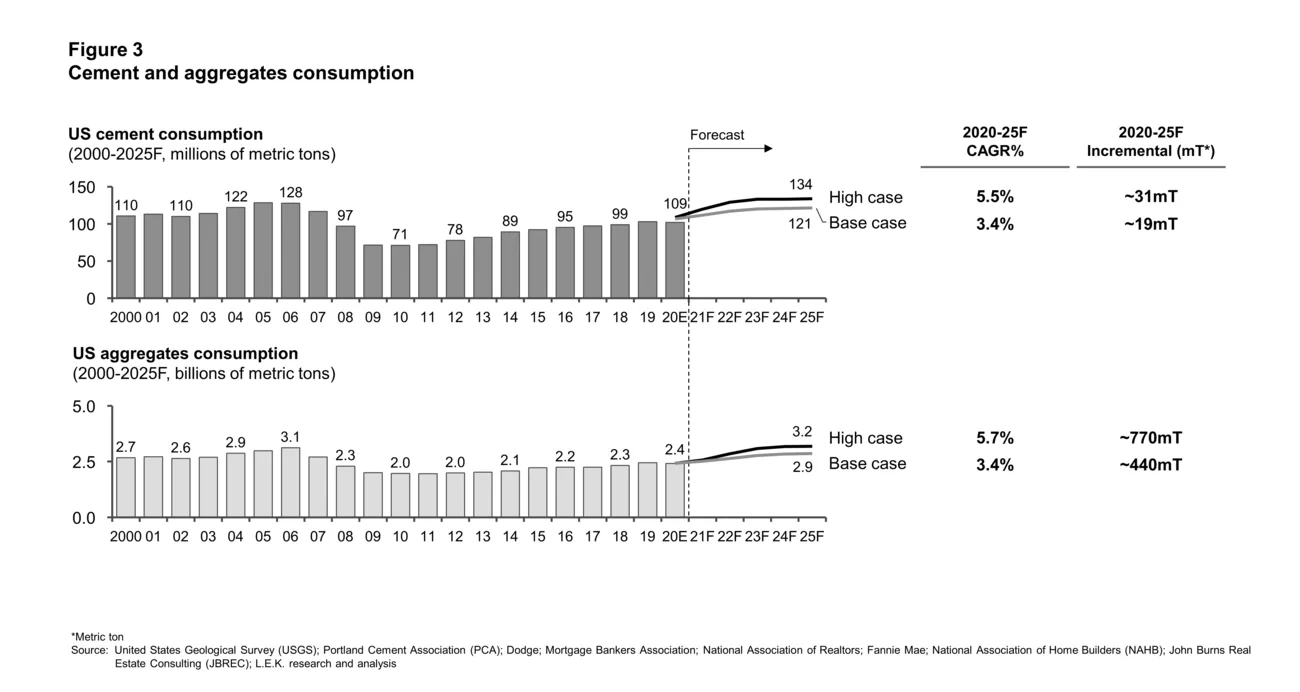

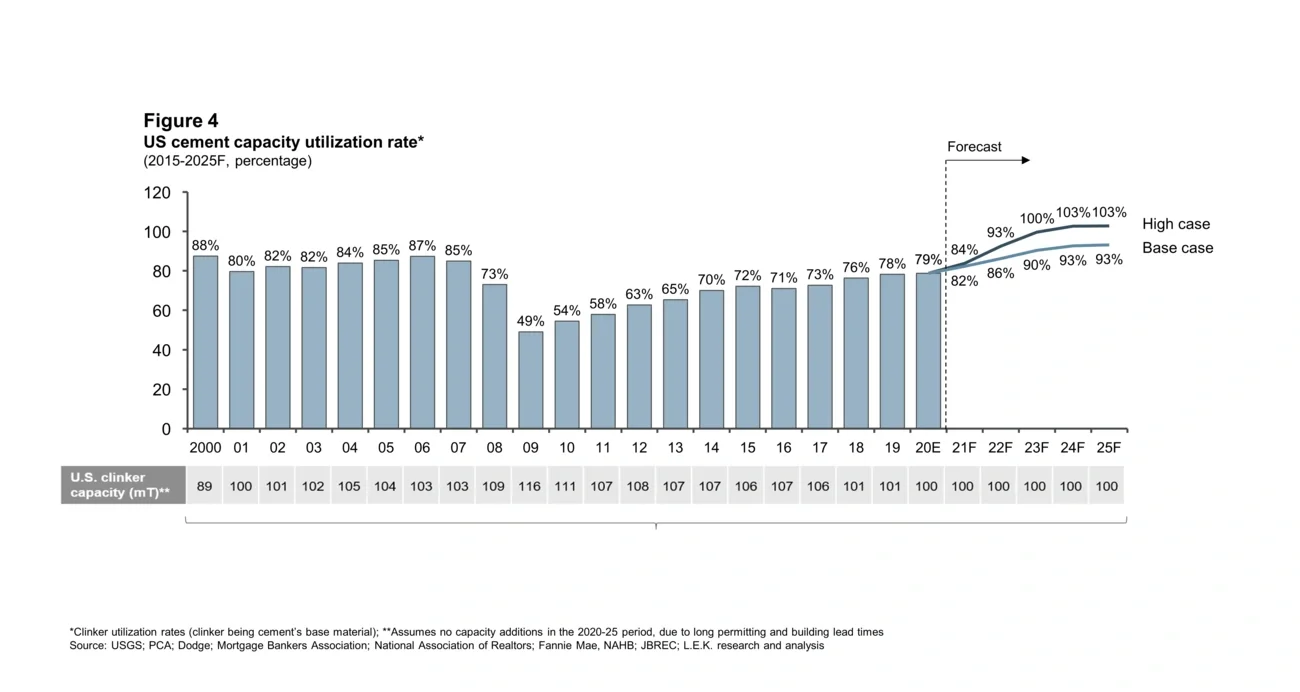

Supply, on the other hand, is expected to be tight. Utilization rates for key construction inputs such as cement, concrete and asphalt are already high, while industrial metal prices have soared and labor shortages are back to their highest levels.

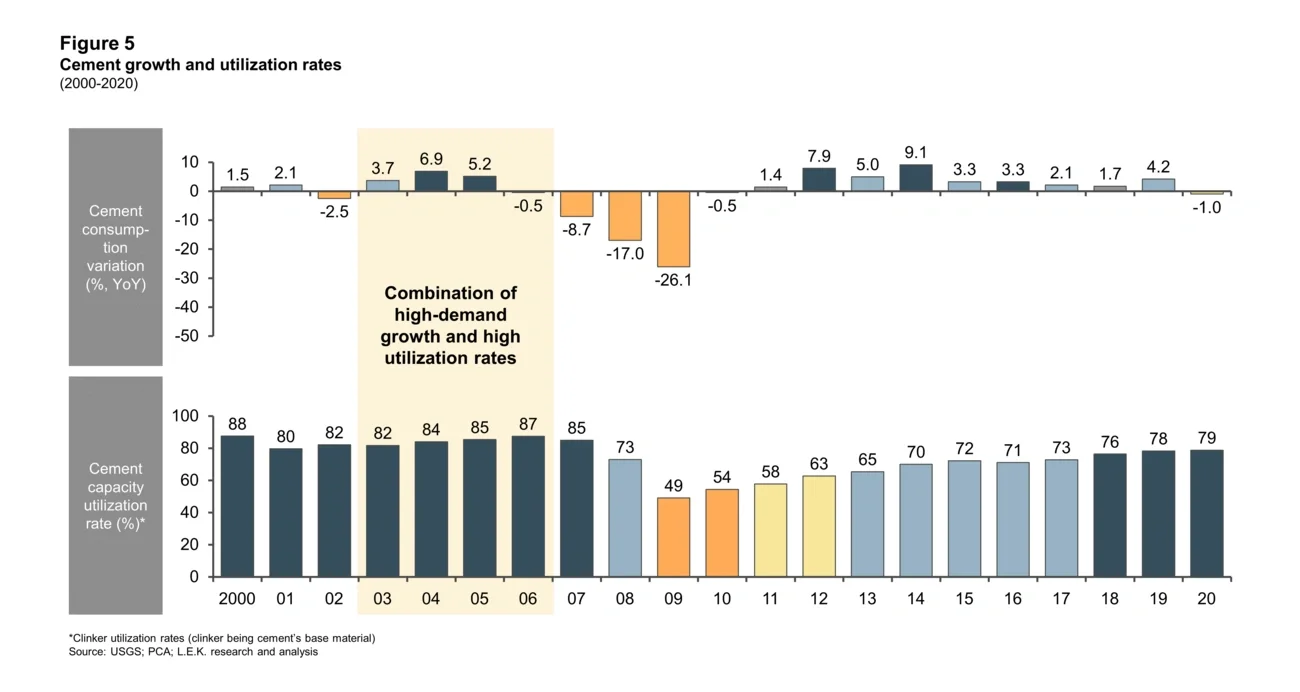

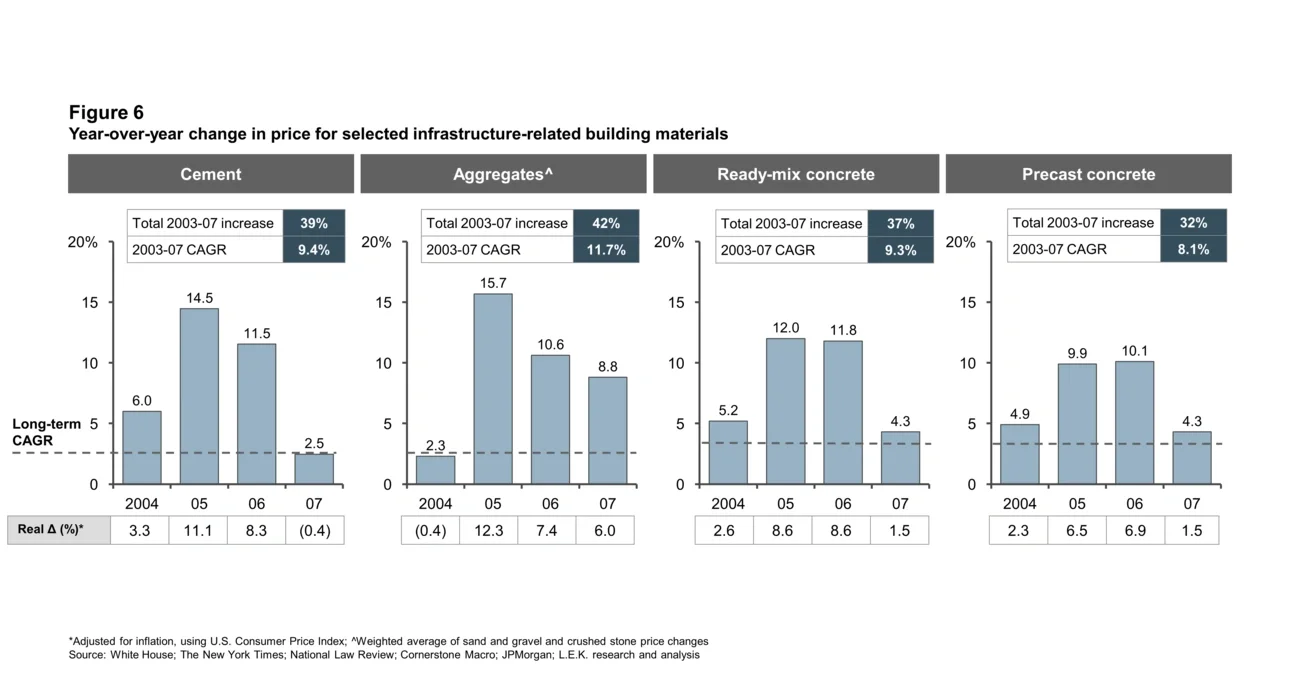

In the past, such as during the housing boom of the early 2000s, milder increases in demand combined with high utilization rates have led to substantial price increases, well above underlying inflation, and generated significant profit upside for industry participants.

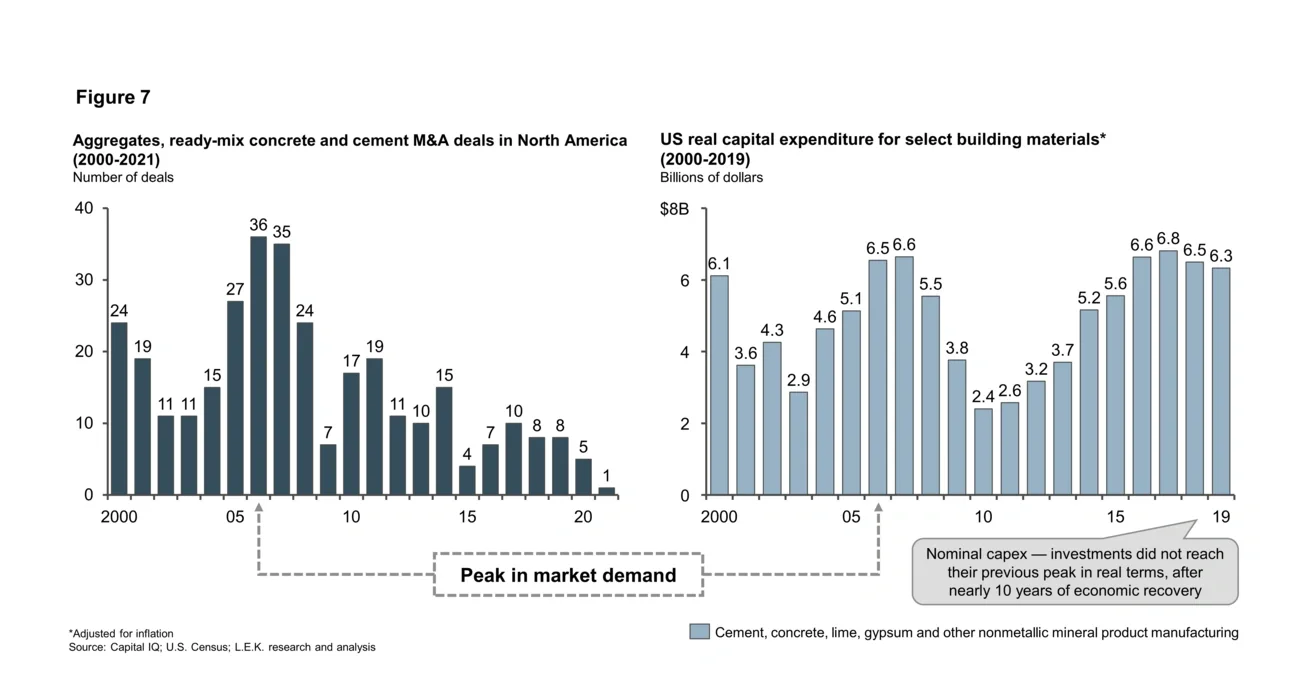

Historically, market participants have tended to be reactive to situations of profit expansion, but they currently have a window of opportunity to invest tactically before production capacities are saturated and profits surge.

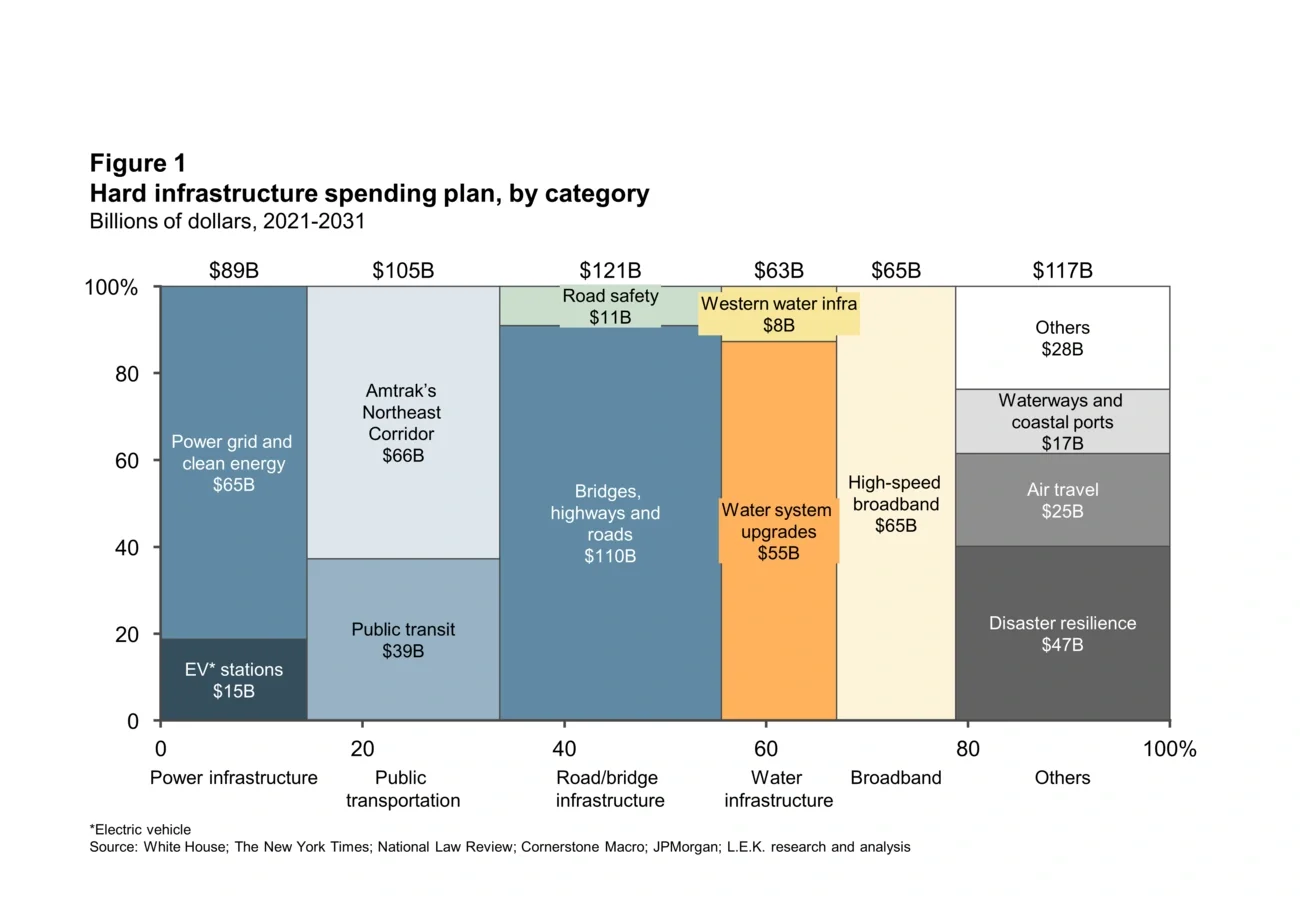

Allocations in the Bipartisan Infrastructure Framework and the reconciliation bill

Two funding streams for infrastructure are currently in play. The Infrastructure Investment and Jobs Act (see Figure 1), which passed the Congress in November 2021, focuses on “hard infrastructure” (roads, bridges, tunnels, public transportation and the power grid) with an overall allocation of $550 billion. We regard it as our “base case.”