Extended COVID-19 lockdowns gave consumers a chance to reflect on their lives. That’s led to a “priority reset” of how they intend to behave going forward.

In an April pulse survey, we asked U.S. consumers what they expect to spend their time and money on once the outbreak is contained. Edition 1, Part 1 of The Great Reopening and Priority Reset Series covers the macro themes that the survey revealed. Now, in Part 2, we’ll dive into the specific behaviors and shifts in spending that appear to have staying power in the wake of the crisis. (Note that all forward-looking data reported is a reflection of consumer sentiment or expectations and is not an official L.E.K. Consulting forecast.)

Consumers are rethinking their pre-pandemic choices

Among the respondents in our survey:

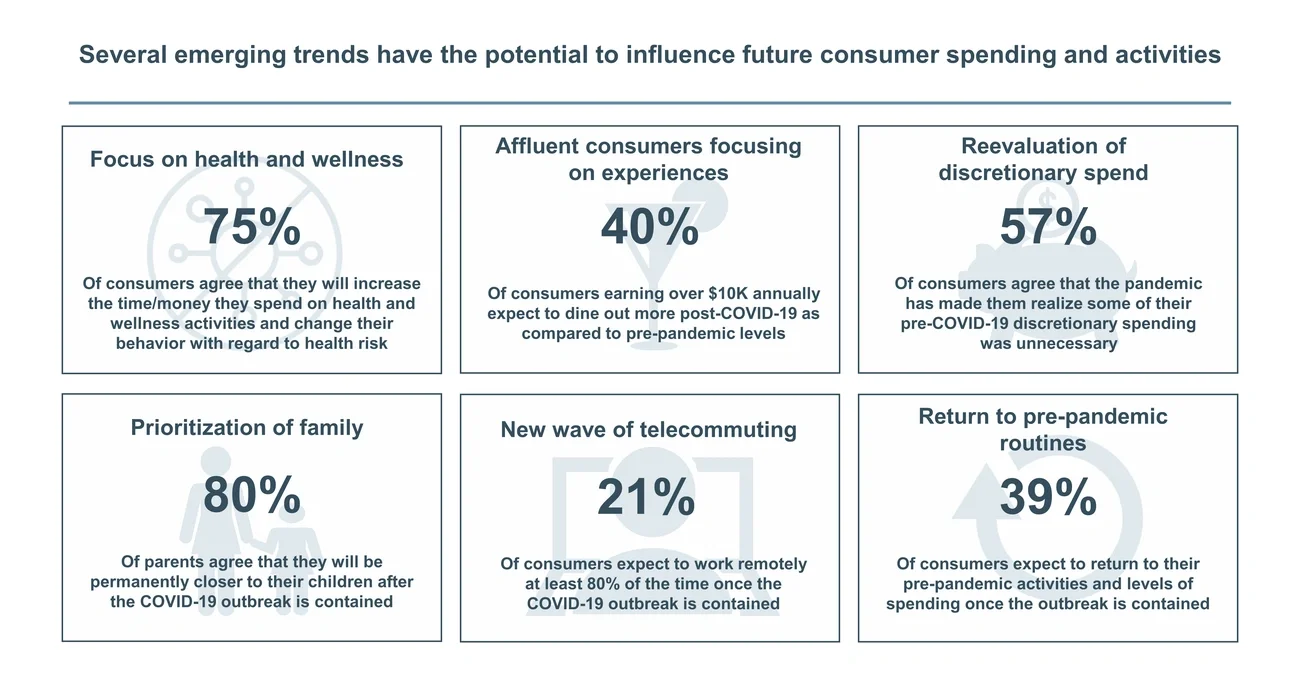

- Most (75%) say they will increase the time and money they spend on health and wellness activities as a result of heightened sensitivity to health risks

- A majority (57%) agree that reflection during the pandemic made them realize that at least some of their pre-COVID-19 discretionary spending was unnecessary

- Most parents (80%) believe they will be permanently closer to their children as a result of the pandemic