The home furnishings industry has endured a tumultuous period as demand has fallen off COVID-19-induced highs. As the industry seeks to regain its footing and stakeholders plan for 2025, it is crucial to examine the factors that are driving home products categories and their implications for brands, retailers and investors in the space.

The industry today: Market normalizes post-COVID-19, prepared for growth

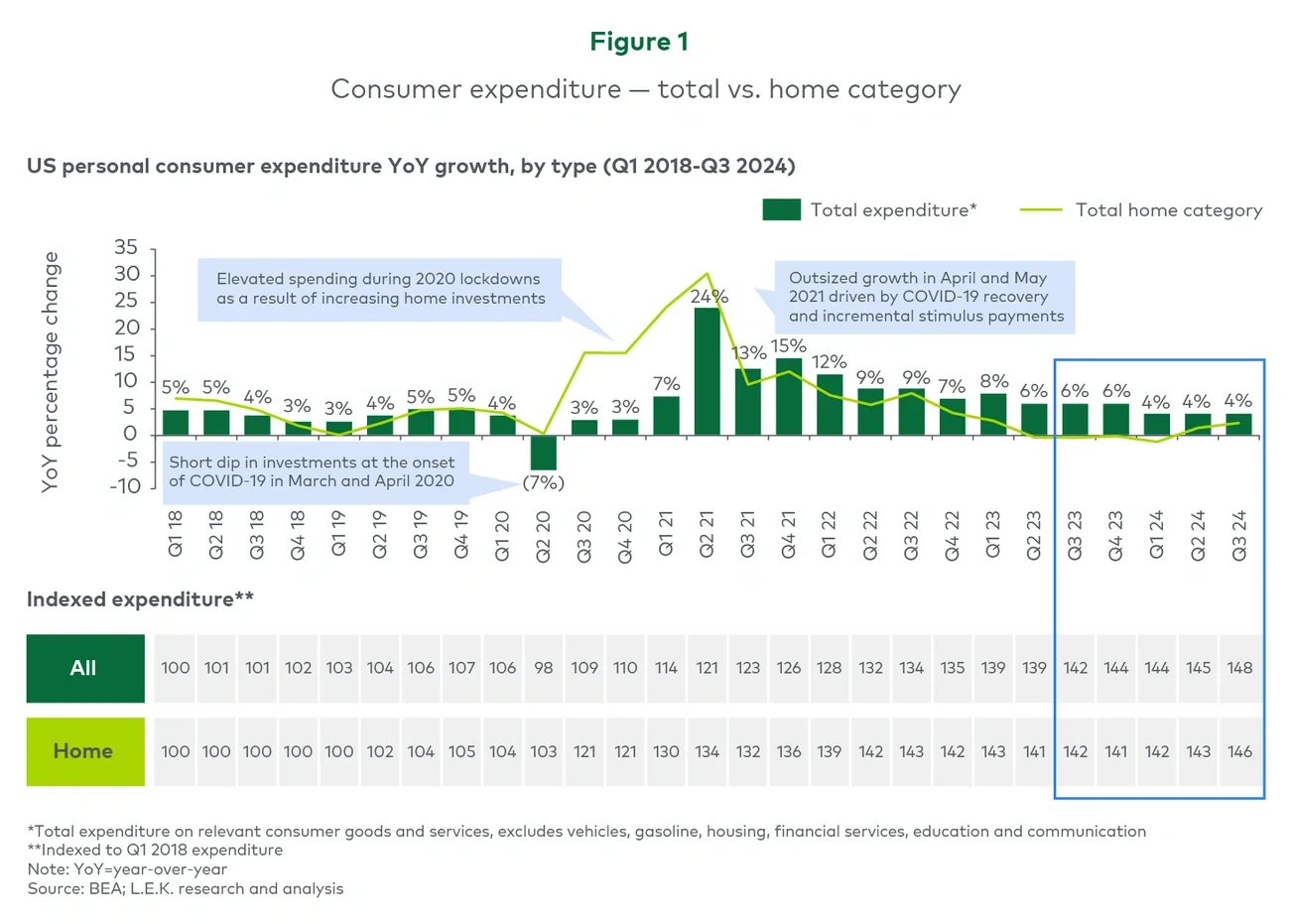

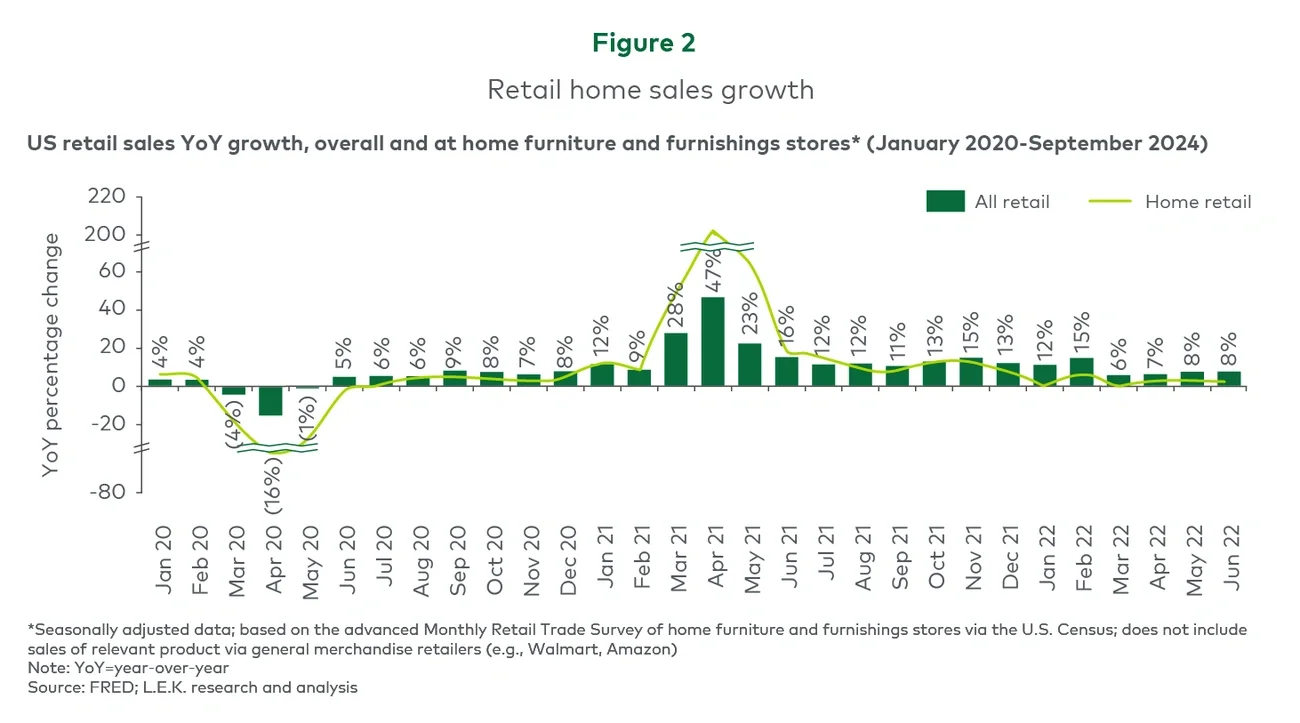

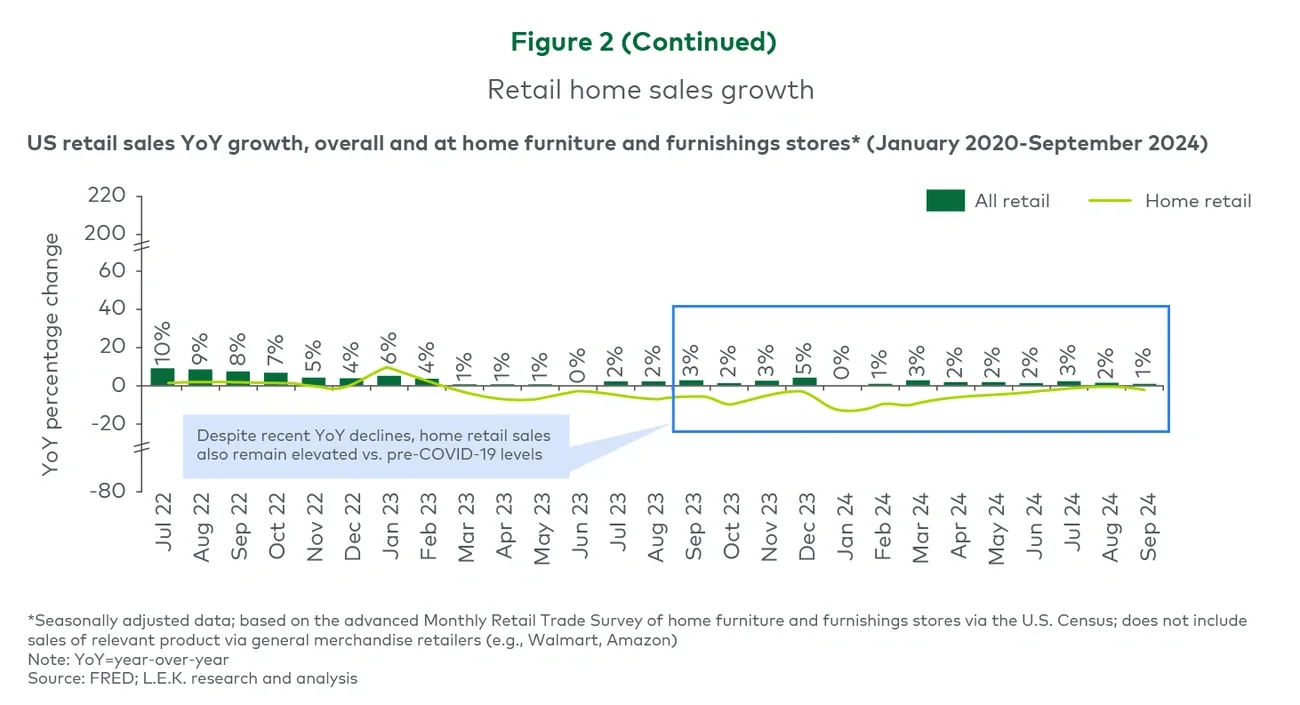

The home furnishings industry is beginning to normalize, following near-flat sales in 2023 and 2024 year to date (YTD) (see Figure 1). Growth in home expenditure has consistently lagged that of broader consumer spending since late 2021, as the industry has had trouble competing against COVID-19-enhanced sales amid high inflation and headwinds from declining home sales and subsequent lower R&R spend.