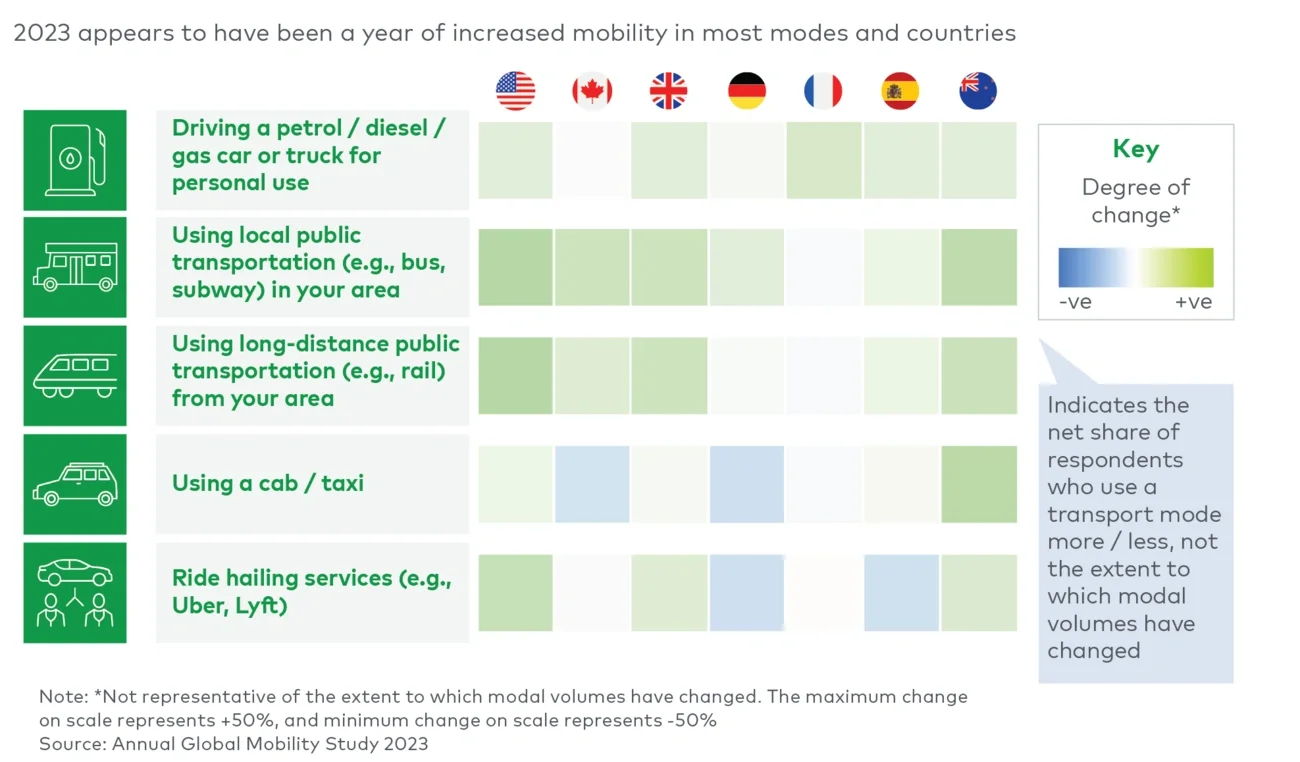

Now in its eighth year, L.E.K. Consulting’s 2023 study of global mobility trends shows a world returning to travel, though levels are yet to match pre-pandemic highs. While the penetration of transport modes appears to have mostly recovered to pre-COVID levels, lifting the lid on suppressed levels of travel, the key question remains, is this sustainable in the face of changing attitudes and new technologies?

Green and healthy are important, with green modes of transport such as electric vehicles (EVs), micro mobility, and healthy options such as cycling and walking, being key winners.

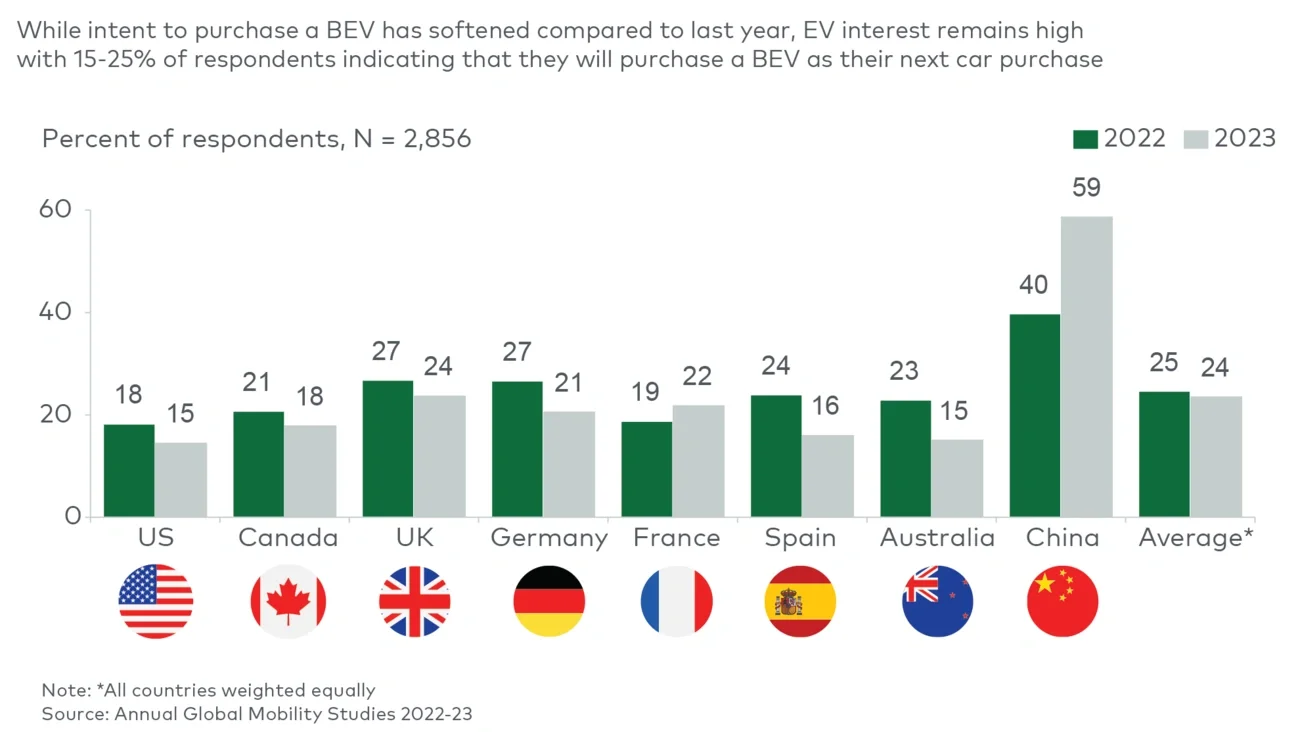

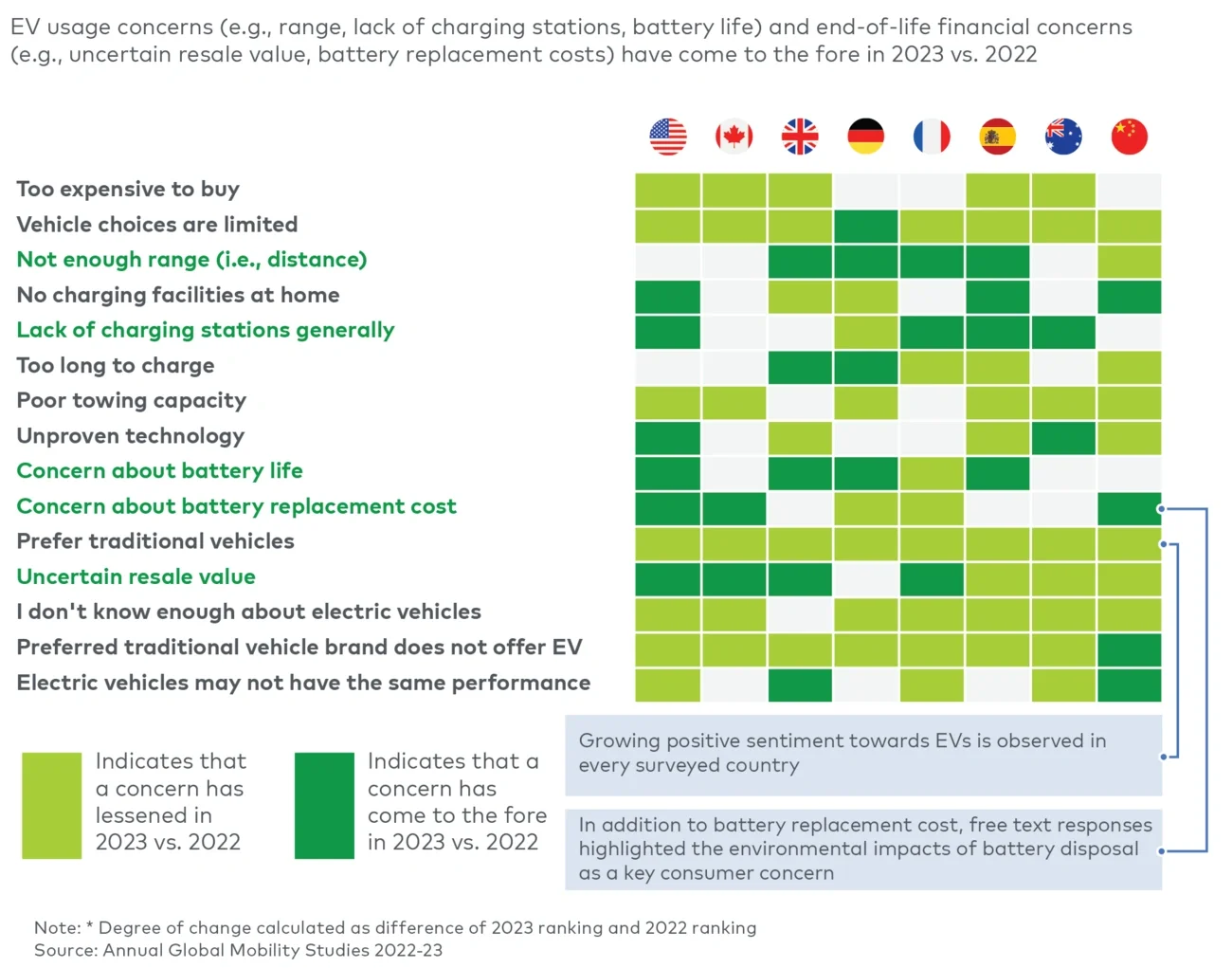

Importantly, there has been a significant shift in barriers to EV adoption, as cost continues to decrease, and technology continues to improve. A good example is that top-of-the- range EVs available today have range specifications that meet the needs of 70%-80% of respondents. This change sees cost no longer the number one barrier to EV adoption in UK, US, and AUS, for the first time since we launched the study. Replacing price worries are anxieties around access to charging and battery life/replacement.

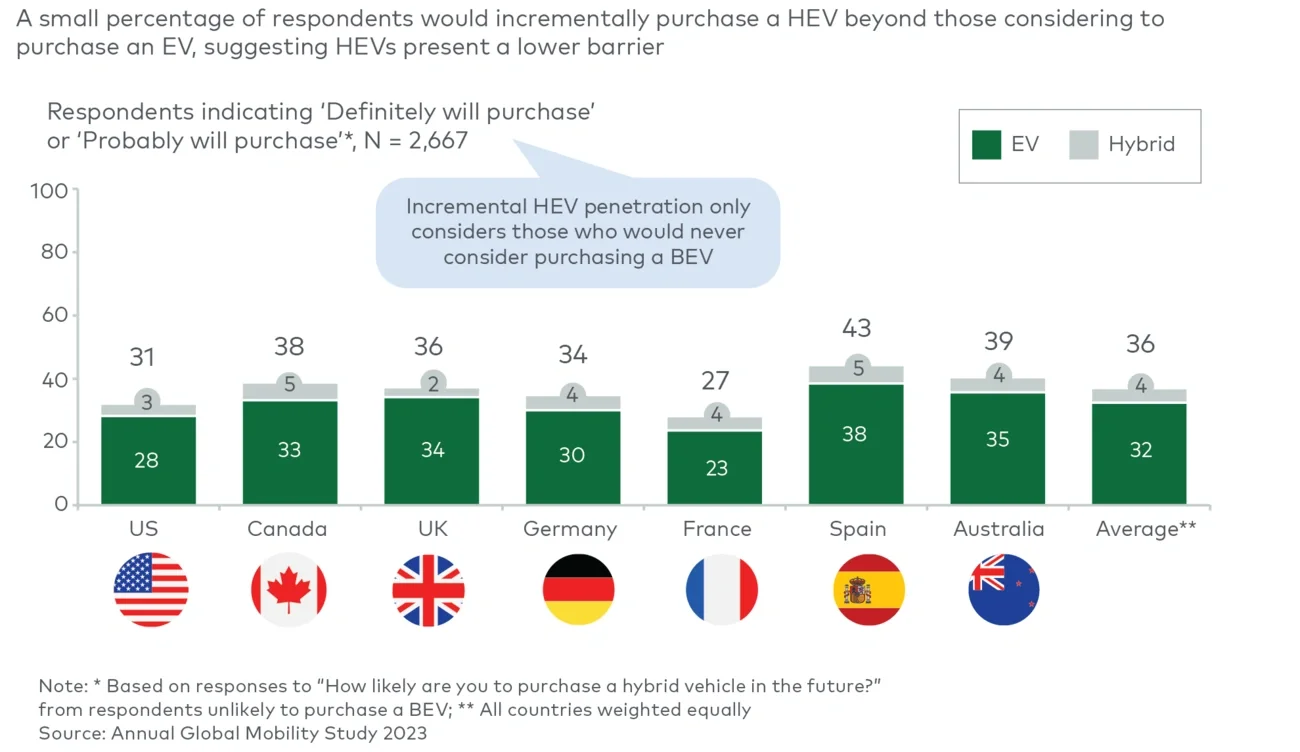

Despite recent sales blips, lower cost EVs entering the market and improvements in charging networks point towards the potential for a near-term acceleration in EV adoption. We set out to better understand the consumers who can drive this trend.

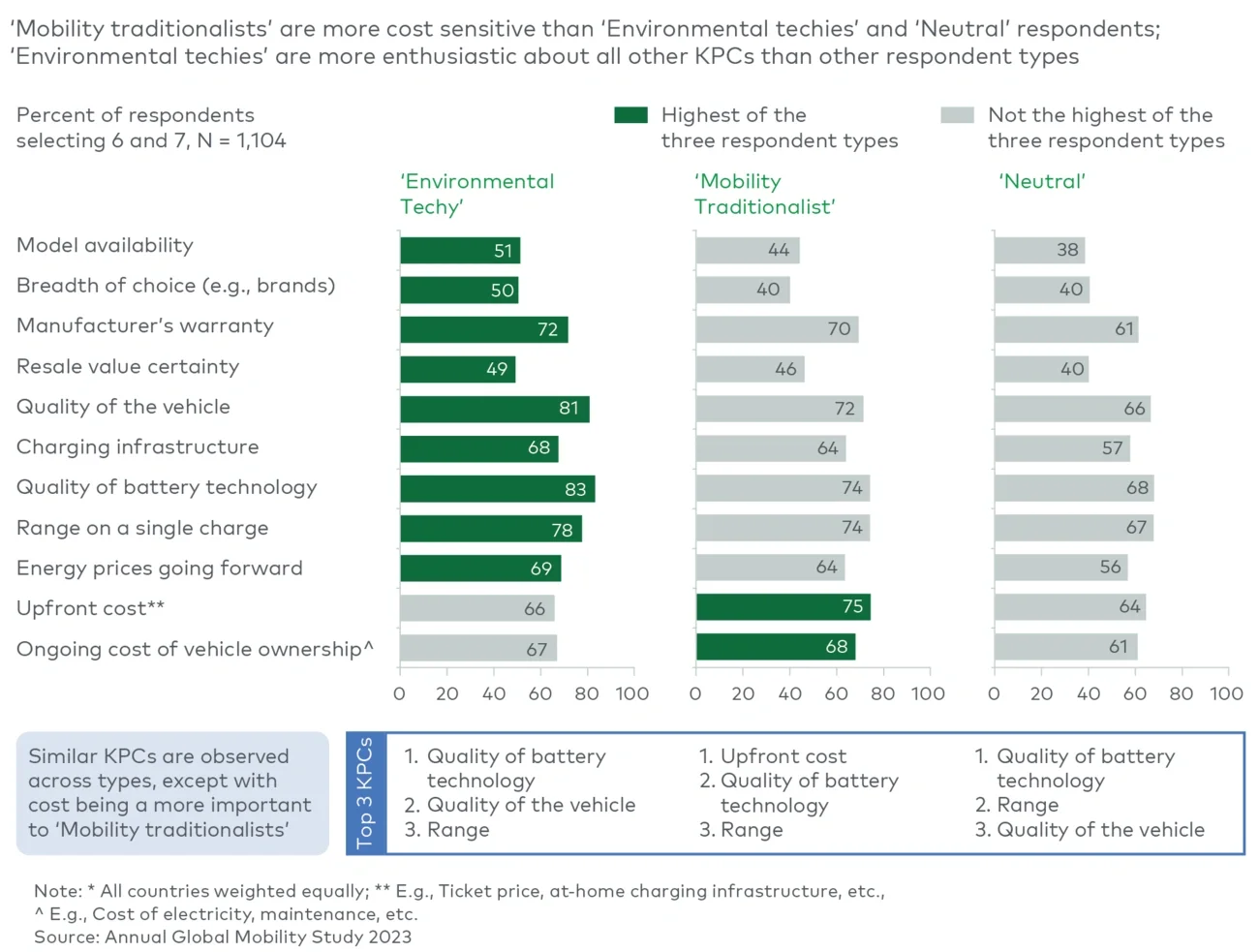

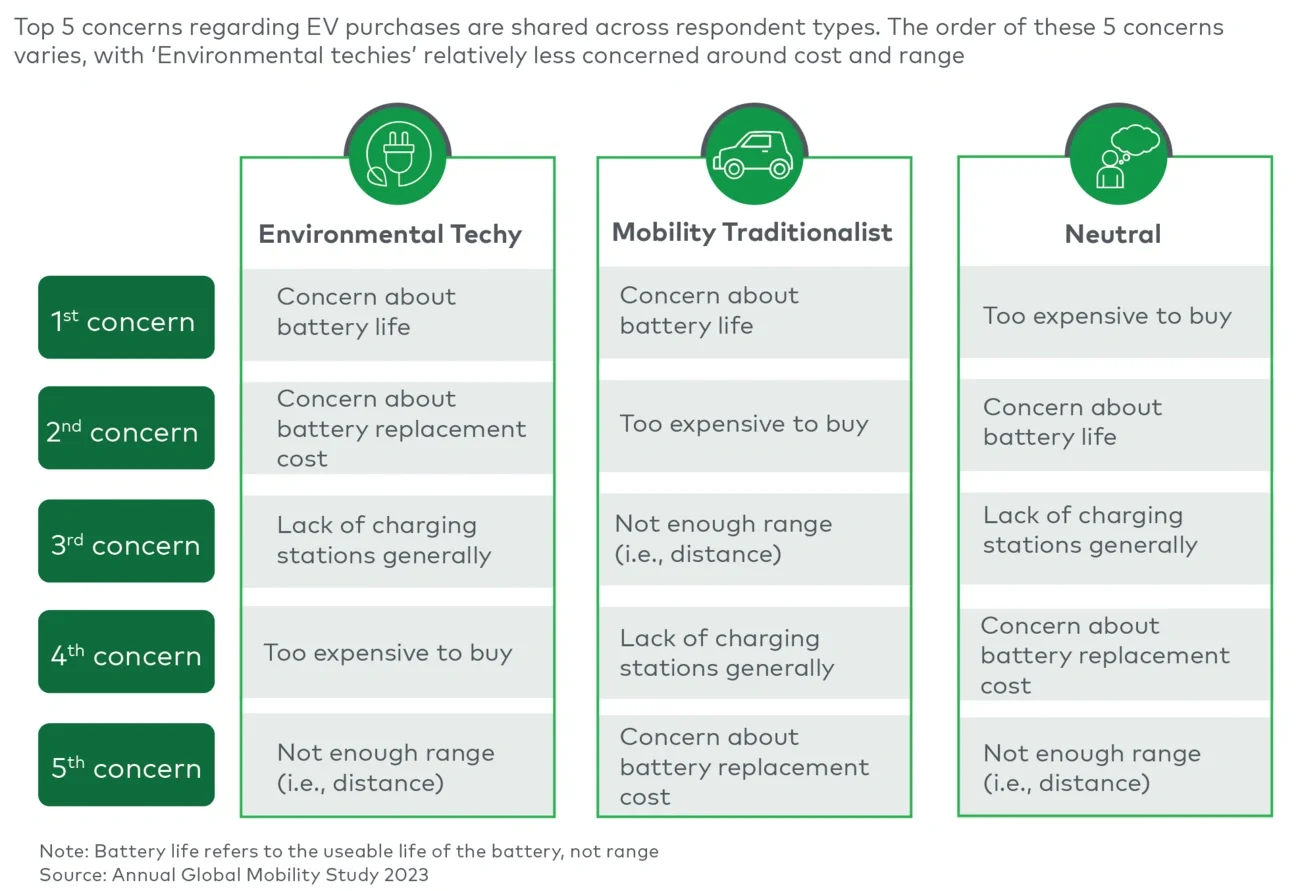

We identified three self-reported categories of mobility personalities: ‘Mobility Traditionalists’, ‘Environmental Techies’, and ‘Neutral’. Each have different attitudes to travel, likelihood of EV adoption, perceived barriers to adoption, and key purchasing criteria. A fluent understanding of the nuances of these mobility personalities will be key to creating a thoughtful EV strategy, and navigating the ever-changing EV landscape.

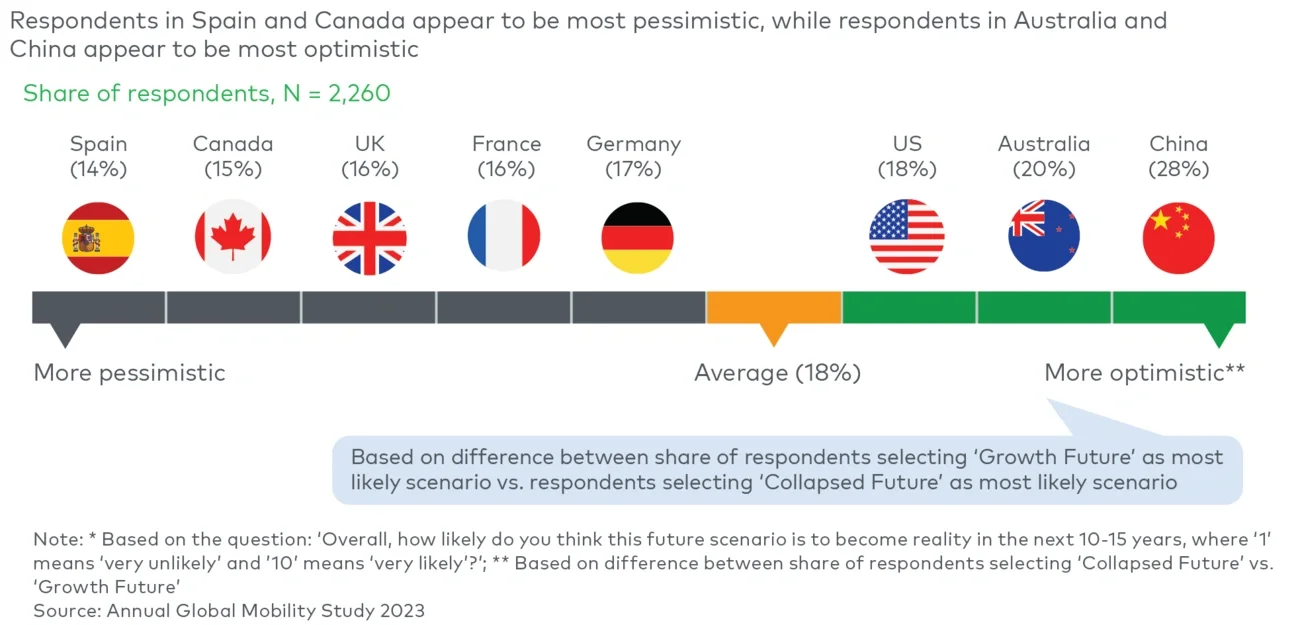

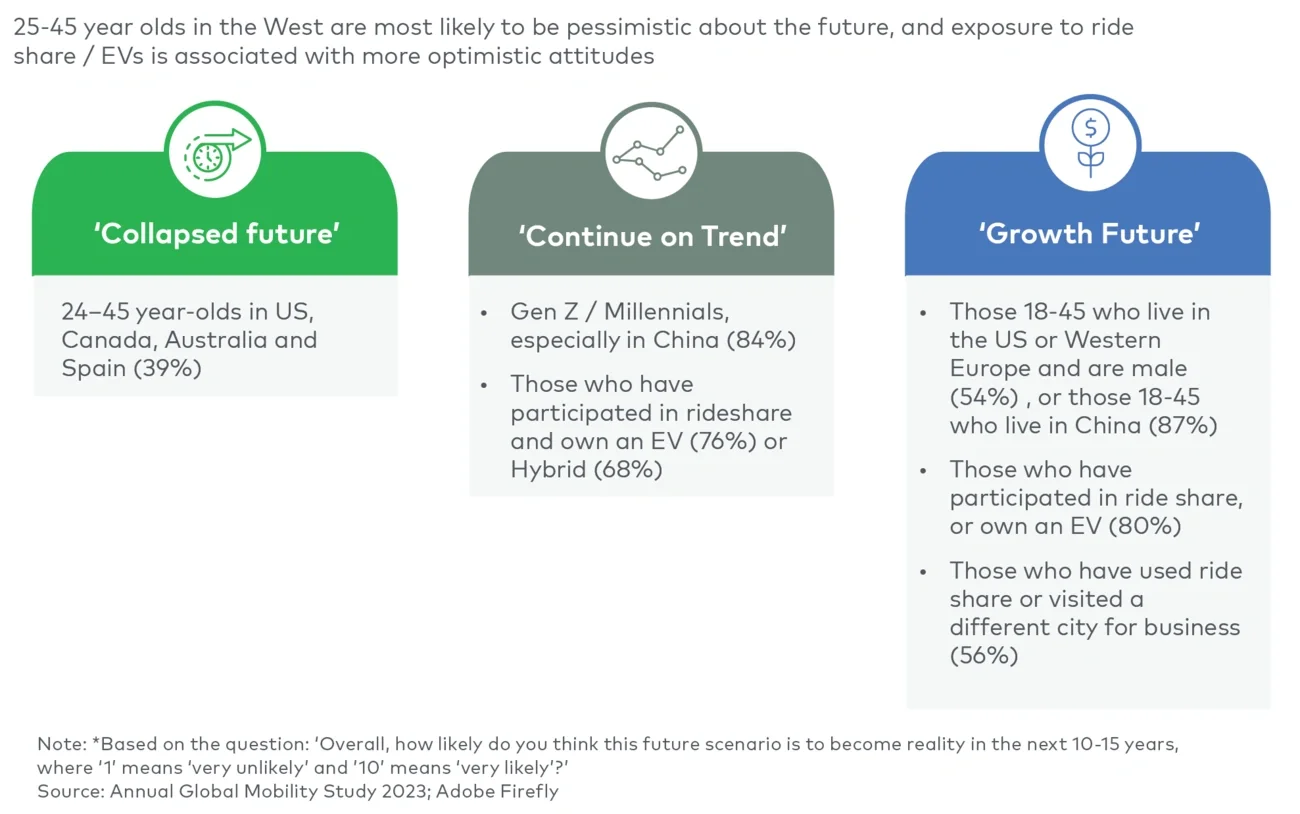

Our study reveals plenty of reasons to be cheerful, with respondents overall appearing more optimistic about the future than pessimistic, a strong suggestion that they are happy with the current pace of mobility innovation and enjoying positive exposure to EVs and ride- sharing. A future with personal BEVs (Battery Electric Vehicles), autonomous taxis, and eVTOLs (electric Vertical Take-off and Landing) was considered the most likely scenario for 2040. With most of those surveyed rejecting the idea of a future of less affordable private vehicle ownership and a reliance on micro-mobility and autonomous fleets. But not all demographics are created equal, and it’s 25–45-year-olds in the West that are most likely to be pessimistic about the future.

Key mobility issues are changing

The main issues affecting mobility have changed in recent years. 2019 saw increasing environmental concern, new regulation, and an interest in renewable energy and shared mobility on the rise. But the 2020 Covid pandemic decreased mobility and the start of the energy transition journey – fuelled by a growing recognition of the environmental issues we face on a global basis – brought further change.

2021 saw EVs beginning to gain prominence, but 2022 brought the cost-of-living-crisis, putting the brakes on EV purchase for many, but not stopping the rapid evolution of EV infrastructure.

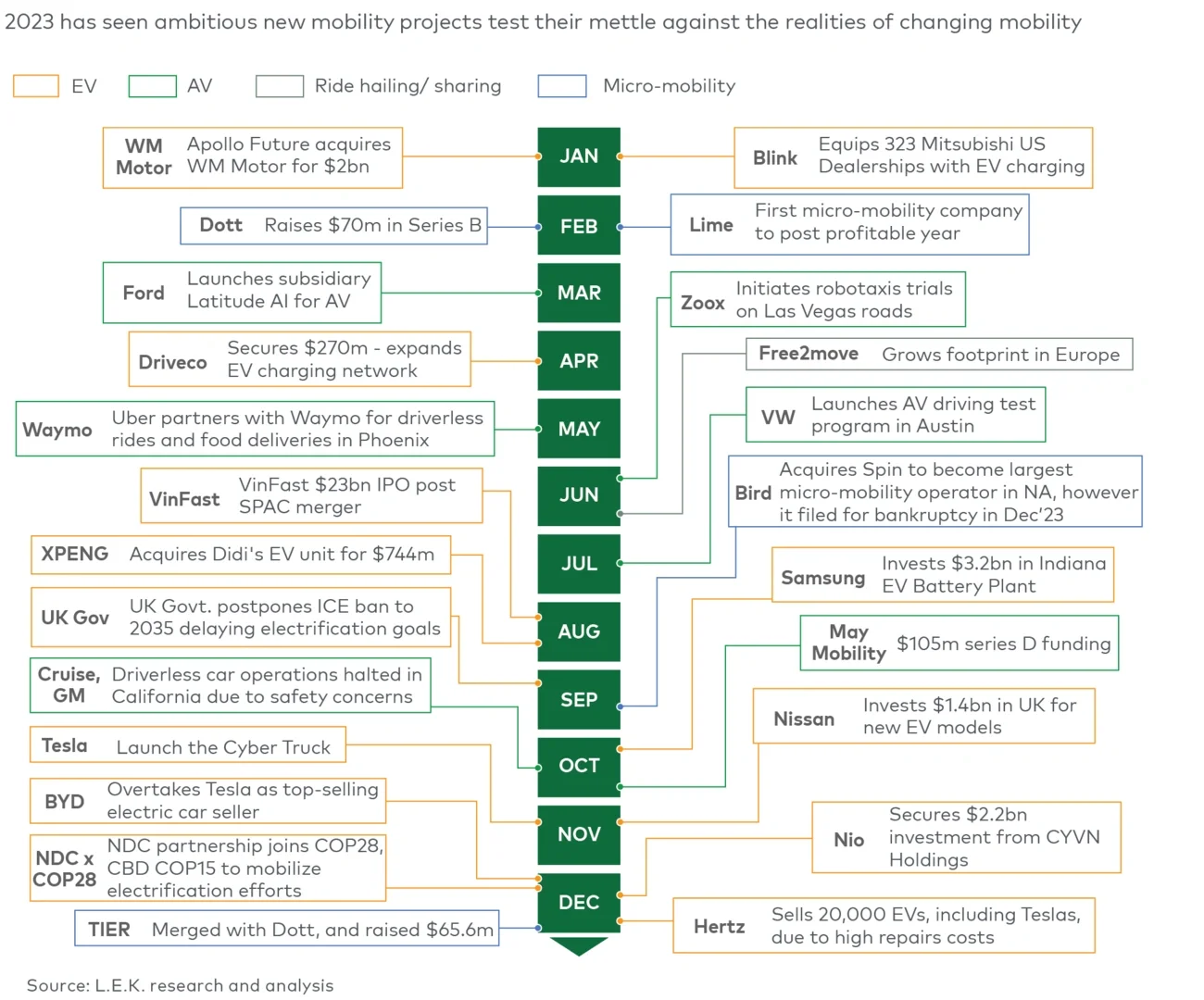

Fast forward to 2023 and the world has returned to travel and EV concerns are shifting. The year saw ambitious new mobility projects test their mettle, such as Lime becoming the very first micro-mobility company to post a profit in January, and the $65.6m funds raised in December by TIER on their merger with Dott. A glance at the chart below demonstrates just some of the activity that has pushed mobility forward (see Figure 1).