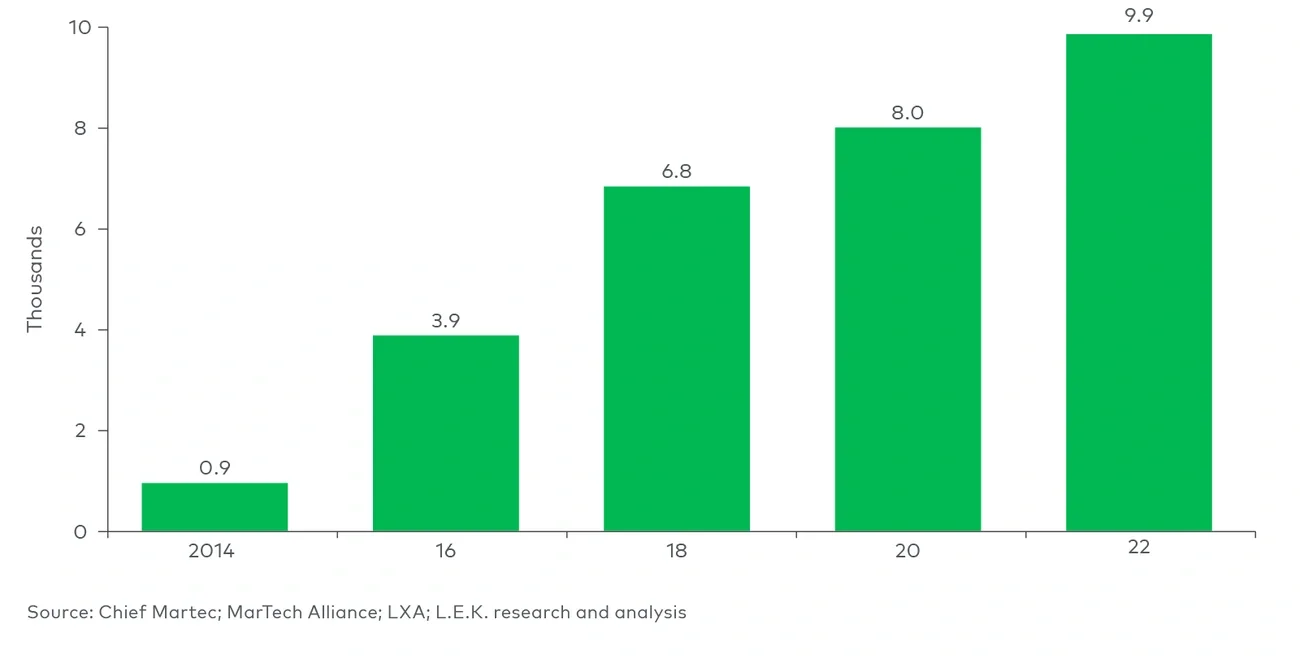

Marketing technology (MarTech) is a large and growing segment of enterprise SaaS. Used by several marketing and related functions to engage customers, martech has been around for decades but continues to evolve with new capabilities. Large organizations often have more than 100 different martech tools in use. But what does this mean for today’s martech stack and investment opportunities to capture the next phase of growth?

Despite its relative maturity, we believe today’s martech stack offers plenty of opportunity to catch a new wave of growth. In the U.S., spending on marketing and adjacent customer experience and engagement technologies exceeded $50 billion for 2022. And signs point to continued growth: 90% of chief marketing officers (CMOs) are expected to maintain or increase martech investment over the next year.

Will those expectations hold up? Likely yes. MarTech is more resilient to macroeconomic conditions than other marketing spend. Part of the reason is that many martech initiatives currently underway are multiyear transformation efforts that require ongoing investment to complete. But CMOs often double down on customer experience during times of economic uncertainty. And many companies want to retain their ability to attract and retain customers so they can emerge from a downturn in a stronger position.

In this L.E.K. Consulting Executive Insights, we unpack the key trends and priorities driving martech’s growth and what they mean for investors as they weigh their bets in this dynamic market.

Consumer trends and CMO priorities

Seven key trends are contributing to the rise in martech spend.

1. The continued growth of ecommerce

Despite a significant pull-forward due to COVID-19, U.S. ecommerce spend shows no signs of slowing down. eMarketer expects ecommerce sales to grow roughly 12% a year, reaching $1.7 trillion by 2026. The boost in sales has led to increased competition from both direct-to-consumer and business-to-business brands, as well as from brick-and-mortar retailers intent on developing omnichannel sales.

2. Customer expectations for personalized, engaging experiences

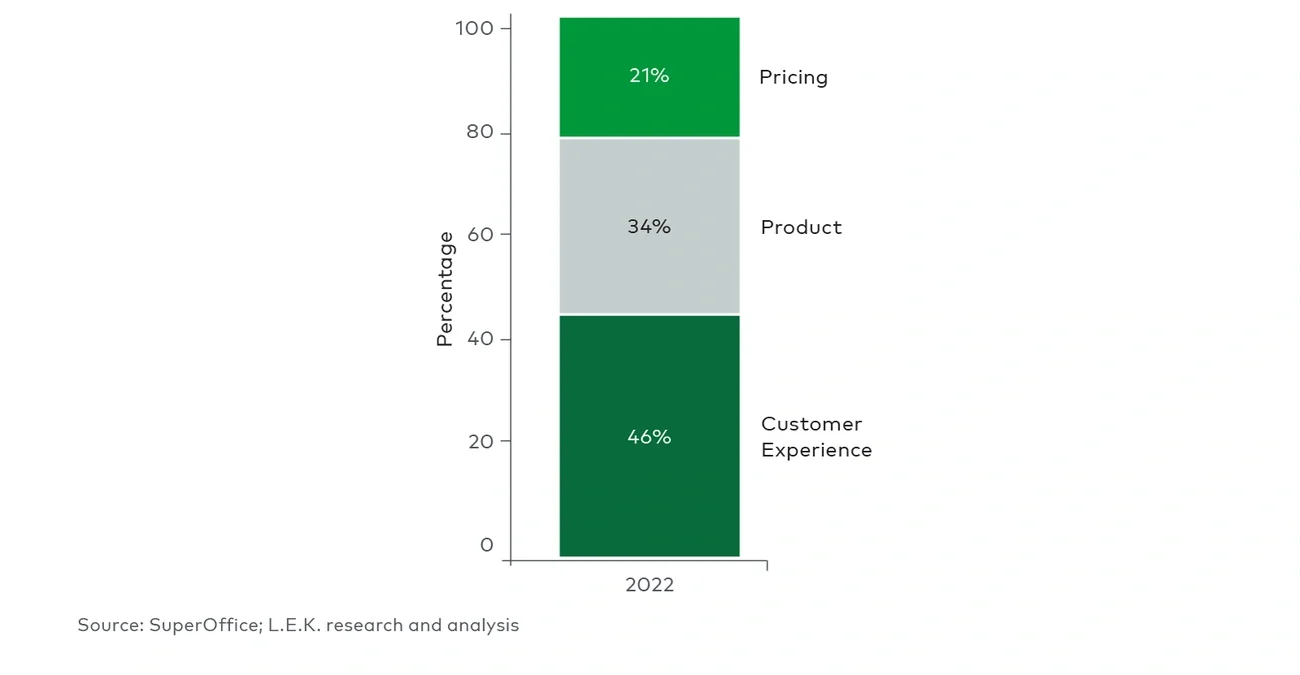

Investments in customer experience can pay off with greater loyalty, satisfaction and engagement. Research from data-marketing company Epsilon, for instance, reveals that 80% of customers are more likely to buy from a business if they feel their experience is personalized. And 80% of customers in a Qualtrics-ServiceNow survey say poor customer experience has caused them to abandon one brand for another. As a result, customer experience has become a top priority for brands, ahead of product or pricing initiatives (see Figure 1).