Three shifts define the current era:

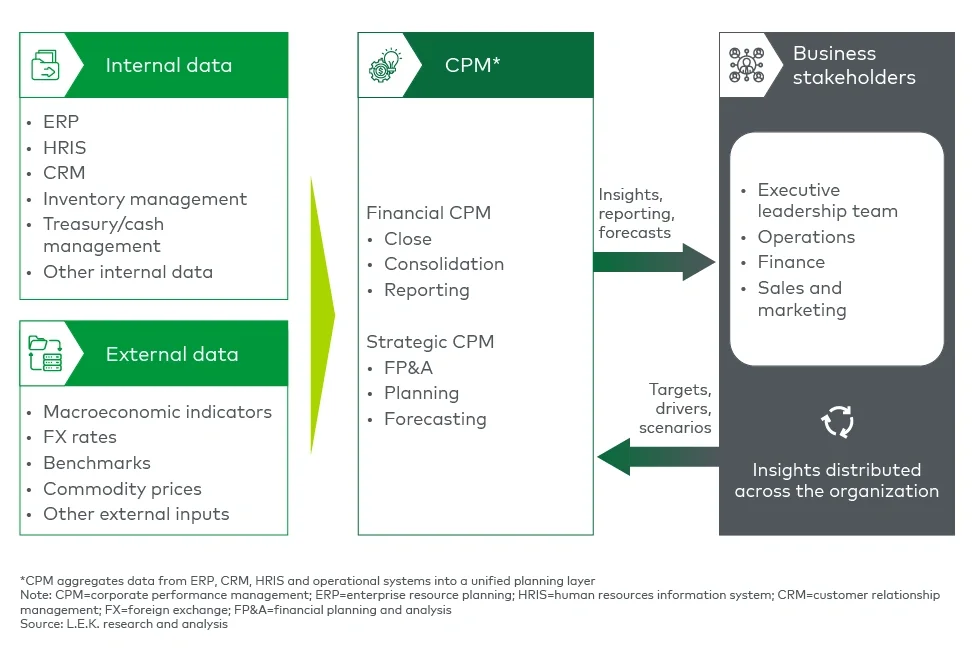

- Cloud and integration maturity: There are more data sources, more connectors and more ability to pull from ERPs, customer relationship management (CRM) systems, human resources information and other operational systems into a unified planning layer.

- Analytics as core, not adjacent: BI-like capabilities have become part of the value proposition rather than a separate system that finance “also uses.”

- Broader stakeholder set: CPM increasingly serves finance plus the rest of the business through xP&A, which changes who influences buying decisions and what features matter.

Buying behavior increasingly favors platforms that unify data and workflows rather than point solutions that create reconciliation headaches. Integration and data security are table stakes. Differentiation comes from usability, real-time analytics, implementation ease and whether the platform can handle complex planning requirements without breaking.

All three shifts raise the same question: What actually differentiates vendors now? AI is often part of the answer, though its role varies in practice.

What role does AI play in CPM?

CPM is well-positioned for AI because it’s data-heavy, recurring and central to how leadership measures performance. The harder question is whether those features land in real workflows, across messy data environments, in ways CFOs trust enough to act on.

AI in CPM isn’t a single story. There’s already meaningful value in machine learning-driven capabilities: predictive forecasting, anomaly detection, pattern recognition and automated data cleansing. Generative AI use cases in CPM solutions are emerging, but adoption remains uneven. These use cases primarily appear in natural language querying, automated variance explanations and narrative reporting layered on top of existing models. The gap between roadmap promises and production deployment matters more for investors evaluating defensibility than it does for buyers focused on immediate workflow improvements.

Beyond AI adoption, the next biggest strategic question facing CPM vendors is platform consolidation.

Will ERPs absorb CPM functions?

This debate keeps surfacing, and it’s the one that most directly affects how durable CPM solution vendors will be.

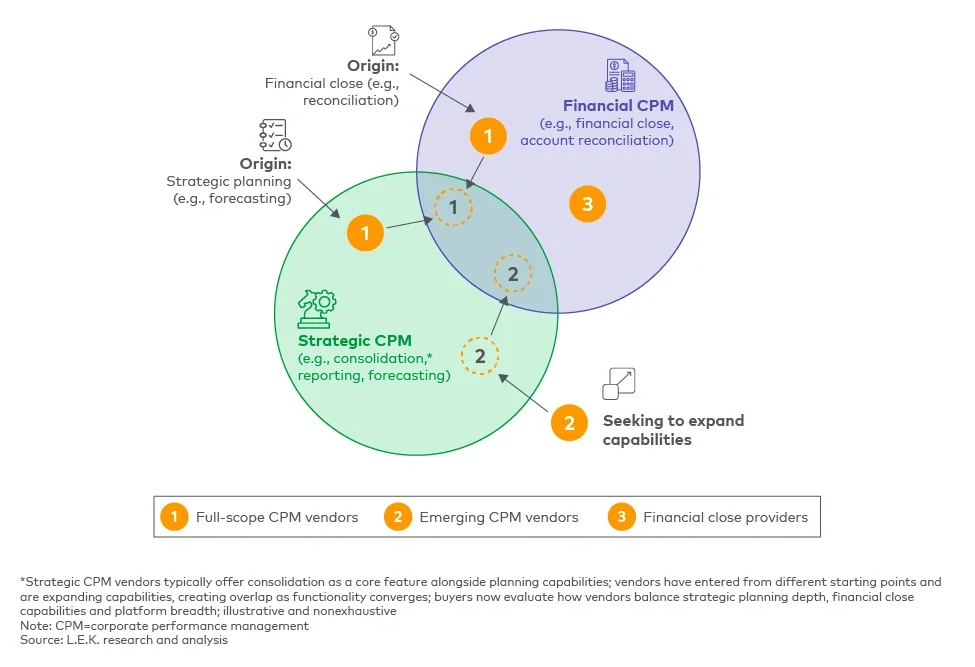

There’s a credible case for CPM solutions as a durable best-of-breed layer:

- Large and complex organizations may have multiple ERPs across entities, so CPM solutions serve as connective tissue that no single ERP can provide.

- CPM solutions pull data beyond ERP (including from CRM systems, operational systems and departmental tools), expanding their role beyond financial data aggregation.

- ERPs have historically been more rigid and slower to deliver the analytics and cross-functional planning capabilities buyers want.

There’s also a credible case for ERP disruption:

- CPM solutions are increasingly viewed as a core operating layer for finance, making them deeply embedded in workflows.

- That centrality makes CPM a natural consolidation target for broader platforms seeking to own planning and analytics end to end.

- If ERP vendors close the gap on analytics, planning user experience and cross-system integration, significant portions of CPM functionality could compress into broader suites.

- Large enterprise buyers often prefer fewer vendors, and ERPs have existing vendor relationships and implementation infrastructure.

CPM capabilities continue expanding even as ERPs improve, sharpening questions about where planning and decision support ultimately reside. Surviving vendors will need clear answers to the question of what they do that ERPs can’t or won’t do and whether that differentiation is defensible.

How should investors evaluate CPM vendors?

CPM remains an attractive category, with sustained demand driven by expanding planning use cases, cross-functional adoption and increasing strategic relevance within the office of the CFO’s tech stack. At the same time, that relevance has intensified competitive pressure as more platforms push into planning and analytics.

Vendors now face pressure from two directions: ERPs are expanding upward with better analytics, and emerging players are competing on faster implementations. Which solutions justify their position in an increasingly consolidated stack?

For investors evaluating CPM vendors, the key questions are:

- Does the product offer genuine differentiation in analytics and planning capabilities, beyond surface-level feature parity?

- Is AI delivering measurable user value beyond roadmap positioning?

- Can the vendor remain durable if ERPs continue improving their planning workflows?

- Will the vendor be able to expand into new customer segments without adding unnecessary complexity?

The category has momentum along with real strategic questions. For most buyers, CPM is unlikely to be swapped out wholesale for ERP-native functionality in the near term. Instead, differentiation will hinge on how vendors defend their role as planning systems evolve, ERPs expand capabilities and buyers reassess where advanced decision support truly belongs.

Our Financial Services team helps investors and software leaders navigate investments across the office of the CFO’s tech stack. We bring deep expertise across CPM, ERP and related financial software to uncover growth opportunities, support transactions and guide strategic decisions. Contact us to explore how we can support your next move in this space.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC