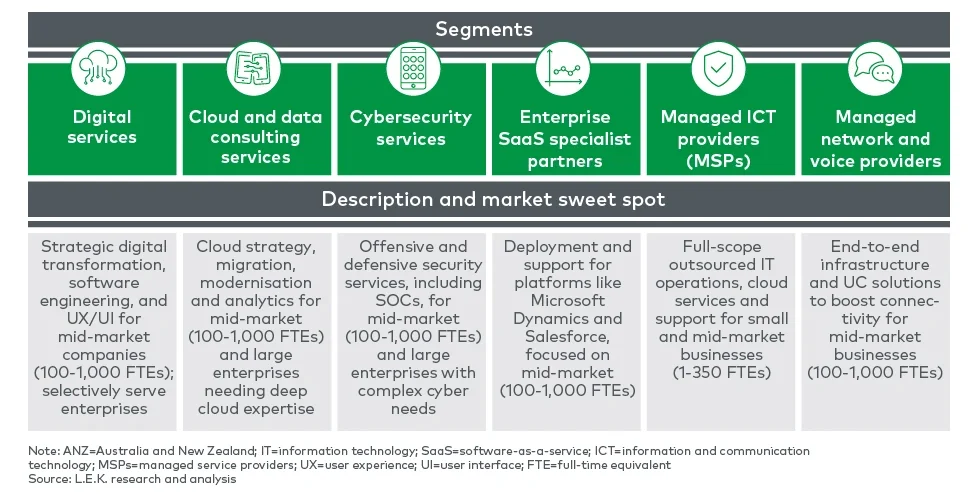

Each segment’s position on the valuation spectrum is shaped by a distinct combination of revenue mix, platform potential and scalability:

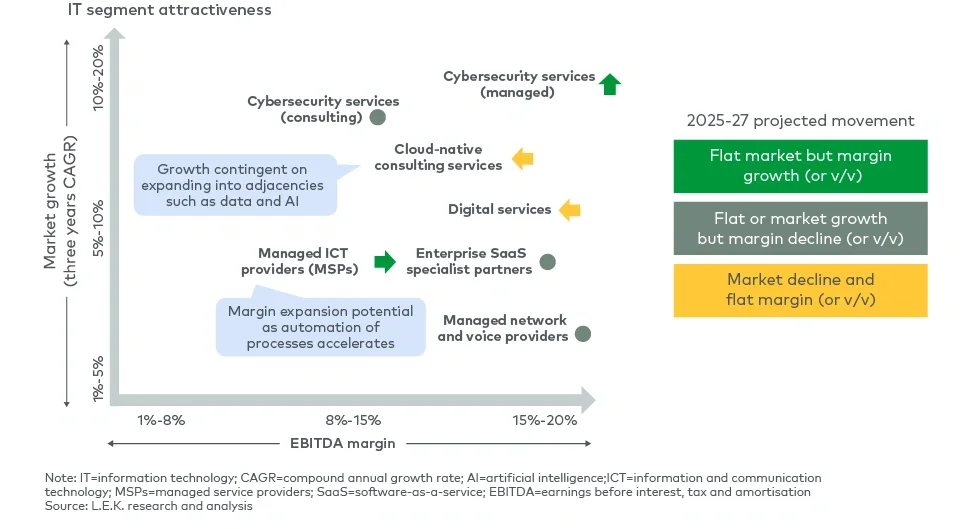

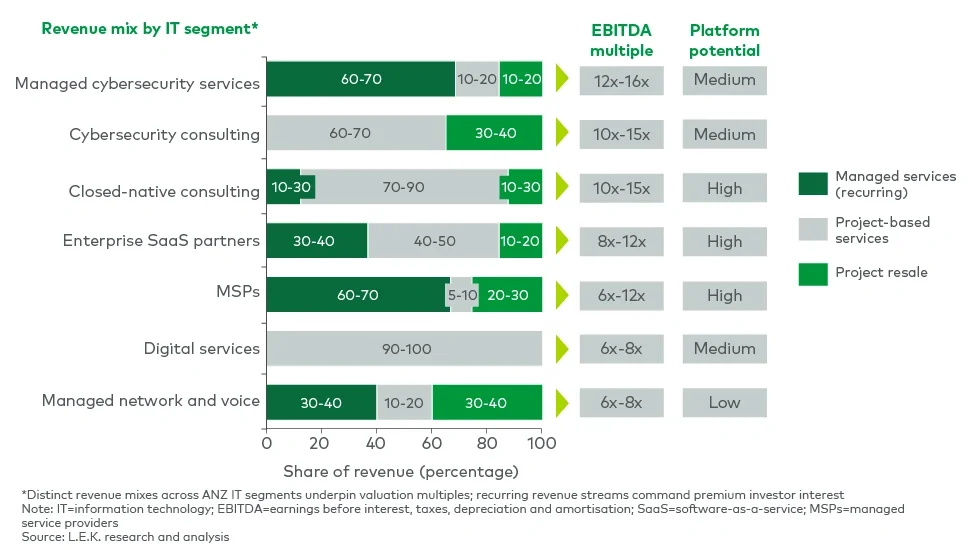

- Managed cybersecurity services lead with 60%-70% recurring revenue and strong platform potential, commanding 12x-16x EBITDA multiples. Growth is driven by increasing threats and regulation, with significant greenfield opportunity. Most cybersecurity work in this space is from organisations that previously had no formal protection, representing true whitespace opportunity rather than displacement of existing providers.

- Cybersecurity consulting earns comparable multiples (10x-15x) despite being more project-based. These businesses benefit from ‘recurring revenue’ — engagements that behave like multiyear contracts despite their project-based nature. Long-term client relationships typically evolve into rolling multiyear statements of work, creating predictable revenue streams.

- Cloud-native consulting (8x-10x multiples) sees only 10%-30% technically recurring revenue but benefits from high client retention and ongoing transformation projects. The most valuable businesses in this segment have evolved beyond basic migration services into data modernisation, AI and application modernisation.

- Enterprise SaaS partners trade at 8x-12x multiples with strong platform potential. Their vendor relationships drive stickiness, with value creation opportunities in vertical accelerators and post-implementation services.

- MSPs maintain 6x-12x multiples with 60%-70% recurring revenue. While operating in a mature market, they offer excellent platform potential for buy-and-build strategies through automation and consolidation. The likelihood of customers using MSPs for both IT work and security decreases as organisation size increases, with specialised security providers becoming more common above 500 employees.

- Digital services remain challenged at 6x-8x EBITDA multiples, with revenue that is 90% or more project-based and margins pressured by offshore competition and AI solutions. Success depends on differentiation or developing managed services offerings.

- Managed network and voice providers face limited growth and margin expansion, with multiples around 6x-8x despite 40% recurring revenue. These businesses typically create more value as bolt-on acquisitions than standalone investments.

These valuation benchmarks are informative, but to gain deeper insight, it’s essential to examine how competition and market evolution are shaping each segment’s strategic outlook.

Market dynamics and emerging opportunities

The competitive environment varies significantly by segment. Specialist independents successfully compete with global firms in high-value segments such as cybersecurity and cloud consulting through their ability to deploy local experts on-site — an advantage global firms often lack in Australia.

MSPs remain absent from enterprise-level engagements dominated by Accenture, Wipro and other global integrators, while mid-market competition occurs primarily among independents.

Service adoption patterns correlate with company size: larger organisations shift towards best-of-breed approaches with multiple specialised vendors, while smaller organisations prefer consolidated providers.

Our in-depth understanding of this industry indicates several high-quality assets will likely enter the market over the next 24 months, spanning MSPs with growing enterprise SaaS capabilities, cloud-native specialists and providers with government expertise. These represent distinct strategic opportunities — from platform acquisitions to transformation plays and bolt-ons — each with specific investment theses focused on cross-selling, margin expansion and consolidation potential.

Navigating the path to value creation

Several strategic implications emerge for private equity investors:

- Segment selection matters: Investment theses must be tailored to specific market opportunities rather than relying on a generic IT services perspective. The varying growth trajectories, margin profiles and competitive dynamics across segments demand deep, segment-level expertise before capital is deployed.

- Revenue mix drives valuation: Recurring revenue should be a central focus across all segments. Investors should prioritise businesses with a clear strategy for transitioning from project-based models to recurring revenue — or those demonstrating strong ‘recurring’ streams through long-term client relationships.

- Scale benefits are segment-specific: MSPs benefit significantly from consolidation-driven operational leverage, while cybersecurity and cloud consultancies gain more from talent concentration and thought leadership. Understanding these differing scale dynamics is essential when setting growth targets and integration strategies.

- Adjacency expansion requires careful orchestration: Cross-selling opportunities must be balanced with the need to preserve specialist positioning. The most successful expansions build on existing technical credibility rather than seeking to replicate the broad service portfolios of global integrators.

- Geographic expansion opportunities vary: Managed cybersecurity and cloud consulting offer viable routes for Southeast Asian growth, whereas other segments face greater challenges when internationalising. Market selection is key — Singapore and Malaysia typically provide more accessible entry points than Indonesia or Vietnam.

The next 12–24 months represent a compelling window for private equity investment in Australia’s independent IT services landscape. The most attractive opportunities will combine strong positioning in high-growth segments with a demonstrated ability to build recurring revenue and enhance both organic growth and margins.

For investors new to this market, understanding the interplay between segment positioning, revenue composition and competitive dynamics is critical to developing a robust investment thesis. Those who can navigate this complexity effectively will be well positioned to capitalise on a market undergoing rapid evolution and consolidation.

Our team brings deep experience in technology strategy, cloud computing, SaaS and M&A advisory. We support investors throughout the full journey — from target identification to value creation — leveraging our proprietary database of 200-plus ANZ providers and a market-sizing model we’ve maintained since 2018, providing robust time-series insights into how these segments have evolved and where they’re headed.

Contact us to discuss how we can help you navigate the ANZ IT services landscape with confidence.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting