This year, we’ve seen a marked acceleration in investor interest in UK professional services firms focused on audit, tax and associated advisory services. Collectively referred to as “accounting services” (to the distaste of some market participants), this sector is witnessing a sustained surge in transaction volumes. Maturing business models and an expanding pool of willing investors are creating favourable conditions for successful investment outcomes, with reduced risks for exits.

Looking ahead to 2025, a wave of private equity (PE)-backed firms is likely to seek new equity and debt investors as they enter their next growth phases. This trend aligns with the natural conclusion of investment periods and a growing track record of successful transactions.

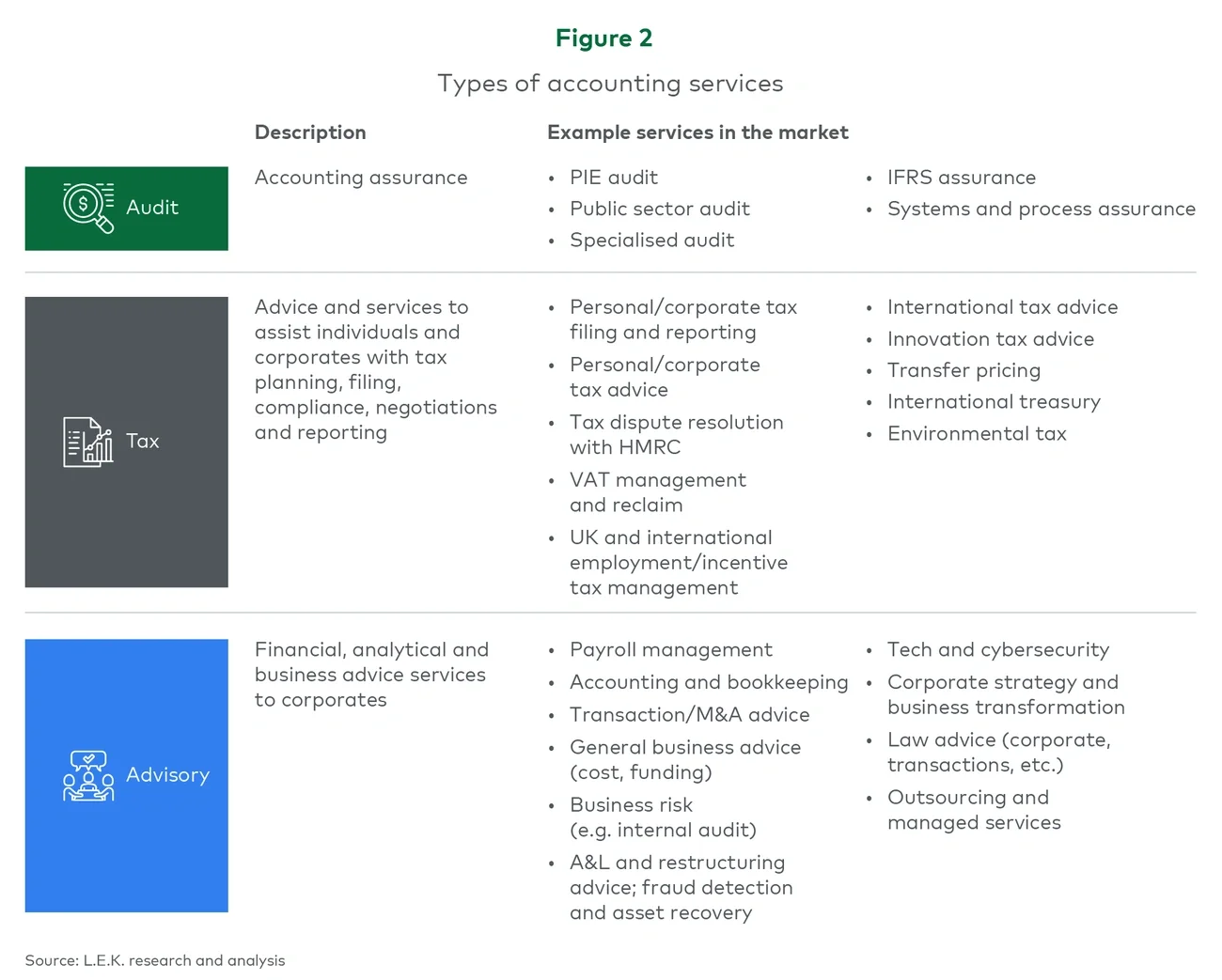

Accounting services present a compelling case for PE value creation. Many parallels can be drawn with established professional services markets, such as actuarial consulting, employee benefits consulting, investment consulting and risk consulting. However, accounting services may offer even greater potential, driven by:

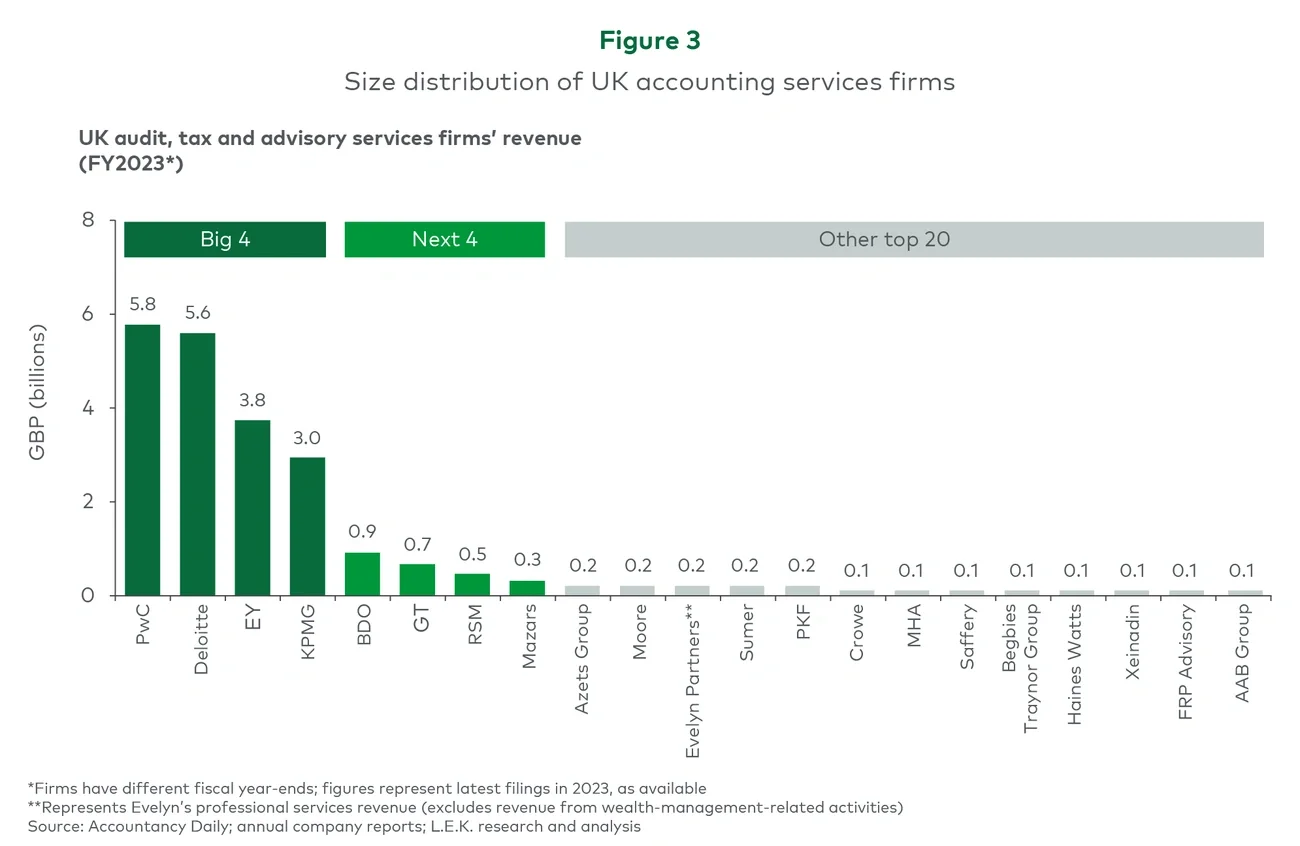

- Market size and resilience: The competitive structure is segmented into tiers, and fragmented underneath a set of global or international majors, with plenty of headroom for consolidation

- Revenue quality: High client retention and recurring revenue streams underpin robust earnings

- Growth potential: New business opportunities are ample, as attractive demand “trickles” down from major players’ increasing focus on multinationals

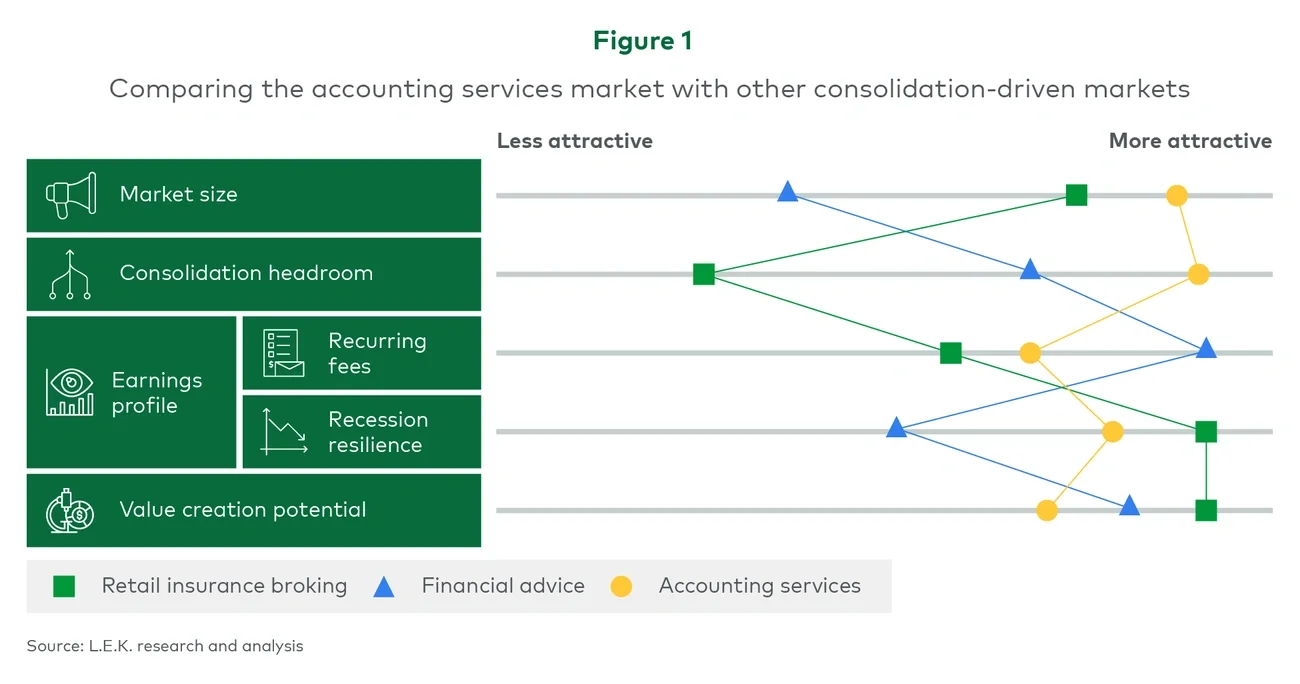

Experienced business services investors are familiar with these opportunities. We’re also finding that the boundaries between business services and financial services are blurring, with professional services assets of interest to both. Financial services investors are increasingly looking to read across past successes in now significantly more mature verticals, such as insurance broking and wealth management. Figure 1 illustrates some of these similarities.