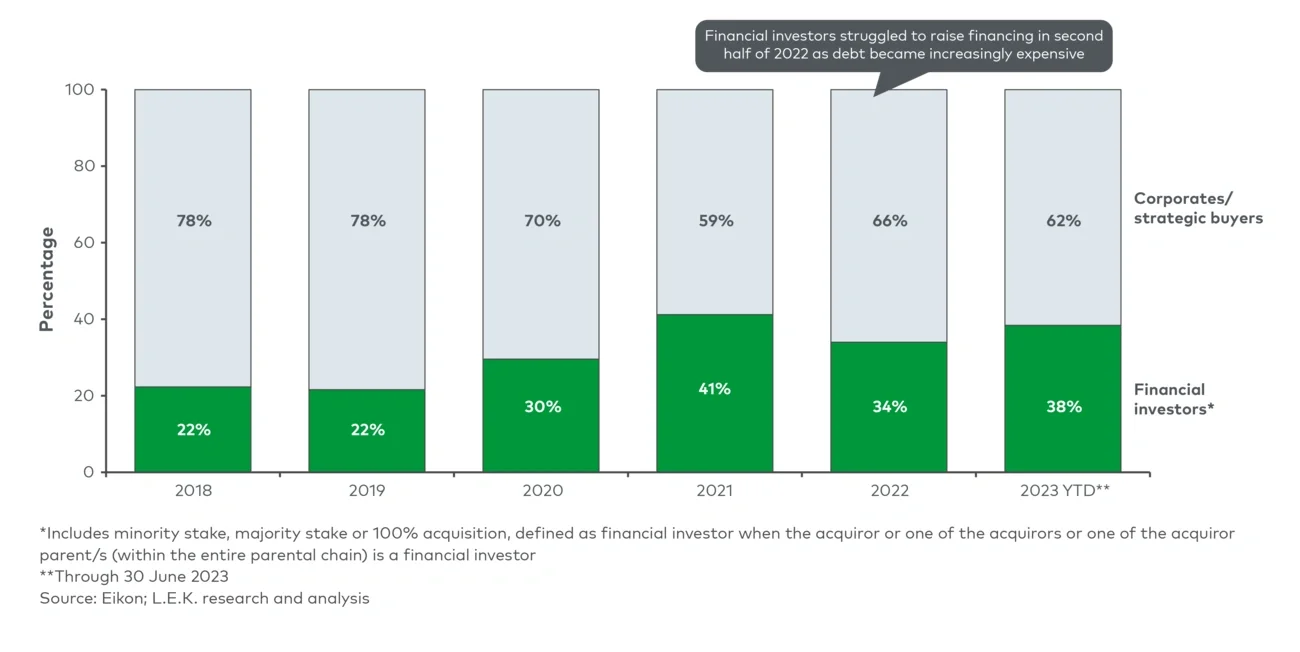

We have identified a trend for corporates/strategic investors to increasingly lose out on acquisitions. Their share of deals won is declining, while financial investors (such as private equity firms, venture capital firms, hedge funds) are winning more of the available pool of opportunities (see Figure 1).

Executive Insights

Creating Winning Behaviours in the Corporate Acquisition Experience

Creating Winning Behaviours in the Corporate Acquisition Experience

Lessons From the Front Line of M&A with L.E.K. Consulting

October 5, 2023

Key takeaways

Corporates appear to be losing out to financial investors in competitive deal processes.

We have witnessed this being driven by issues in speed of mobilisation, lack of focus, limited capabilities, a conservative approach to valuation and lack of agility.

While some issues observed relate to hurdles that cannot easily be removed for corporates —such as governance, ownership and financial setup — there are some behavioural changes that can promote better outcomes.

Corporates currently losing out have much to learn from more successful organisations. L.E.K. Consulting’s work has helped identify five key lessons: (1) a more structured approach to pipeline management, (2) a more suitable governance structure, (3) better focus on critical issues, (4) willingness to make upfront investments and (5) more ambition in valuation.

Figure 1

Share of global M&A deals won by financial investors (by value) (2018-23 YTD)

Image

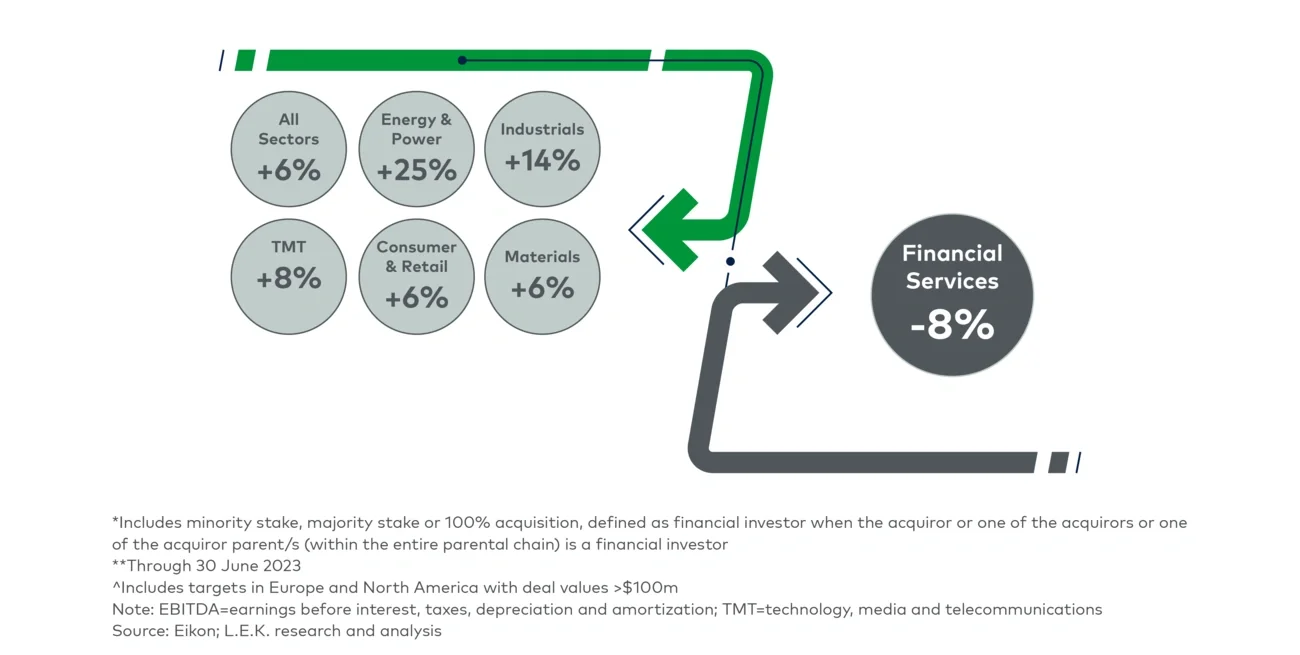

This trend does not appear to be due to financial investors having deeper pockets, as corporates pay a similar, or slightly lower, multiple than financial investors (see Figure 2). This appears counterintuitive, as you would expect corporates to be able to pay a premium as they can incorporate additional strategic value and the impact of synergies in their valuation.

Figure 2

Difference in average EBITDA multiple paid by financial investors* vs corporates (2018-23** YTD)^

Image

While rising interest rates have had an impact on the ability of financial investors to raise debt for large cap deals, this is unlikely to lead to a reversal of the longer-term trend in the competitiveness of corporates in M&A activity. Taking the time to examine your approach to the acquisition journey could pay dividends, and while many corporates manage this activity well, for others there are clear opportunities for improvement.

Our experience has identified five main reasons why corporates might lose out to financial investors:

-

Corporates can be slow to mobilise for a specific deal, so they do not position themselves for success. Reacting to opportunities rather than actively sourcing deals that fit their strategic vision means that they start behind the curve in a process. Financial investors tend to have a more structured approach to pipeline management, and being in the flow of market intelligence means that they know when assets are likely to come to market. Financial investors are also willing to invest in thematic research for a new market space they are considering, so when an asset becomes available, they need to focus only on its valuation. Whereas corporates do not budget for the cost of failure, so they are reticent to invest too much/too early, and when an opportunity does arise, they are left needing to assess both the strategic rationale and potential valuation.

-

Once involved in a deal process, some corporates may experience challenges in maintaining focus during the deal. This is often because they are spending time trying to evaluate different options regarding how they could deploy capital, e.g. executing the deal, waiting for another deal(s) that might be a better fit, developing capabilities internally and returning money to shareholders. This volume of options can result in indecision when reviewing an opportunity. Conversely, financial investors tend to be more decisive, as they are normally focused on moving forward with the deal in front of them and spending their funds to avoid potential reputational damage.

-

Corporates may not always exhibit the same level of nimbleness as do more effective financial investors. They may require more time to get comfortable with a valuation, as they lack the experience or capabilities of financial investors. For financial investors, this is their day job, and generally, they focus on the most critical issues that drive value. They are not the ultimate operators and will own the target for a finite (and short) period of time, so they place less focus during diligence on factors that might not drive value (e.g. HR/people dynamics or health, safety and environment). For corporates without a dedicated team, M&A is not the main day job for most people involved. This puts teams under pressure, and lack of bandwidth can become a serious issue. Those driving the diligence tend to focus on non-critical, longer-term integration considerations that don’t necessarily drive valuation; this only exacerbates the problem.

-

When arriving at a final valuation, corporates can tend towards extreme conservativism. This can manifest itself both in terms of the standalone impact of an acquisition and the synergy potential. Financial investors are often willing to be more aggressive, and as a result, there is risk that corporates will submit uncompetitive offers; this is surprising given that they more often have synergy benefits that can be realised. However, management teams ‘live’ more closely with the consequences of their decisions. This means they have a vested interest in being cautious, as they can visualise all the challenges and know they will need to own/deliver in line with the valuation. In contrast, financial investors have a more aggressive approach to developing a valuation, as they tend to focus on how to deliver the required value only once they own the target and can be bolder in their outlook and more willing to believe in the target’s business plan.

-

Even after navigating these issues, once a corporate arrives at a valuation, it may lack the agility to move swiftly to an offer. This is often due to the structure of its M&A governance and corporate ownership. Most corporates suffer from having longer lines of communication than financial investors, and this makes it harder to be agile. In addition, some corporates are less willing to accept some risk in a deal and look to address all questions before moving forwards. Meanwhile, financial investors have a lower burden of proof and less complexity in terms of constructing deal/offer terms.

Winning approaches

Due to their governance, ownership and financial setup, corporates will always tend to face more approval steps and hurdles in their approach to M&A than most financial investors. This is especially true for public companies. We have observed that corporates who are more successful in their M&A approach usually deploy specific solutions or instil particular behaviours. Learning from these successes and adopting their strategies is a positive way to improve your success rate in the acquisition process. Our five steps to a winning approach help formalise this as follows:

-

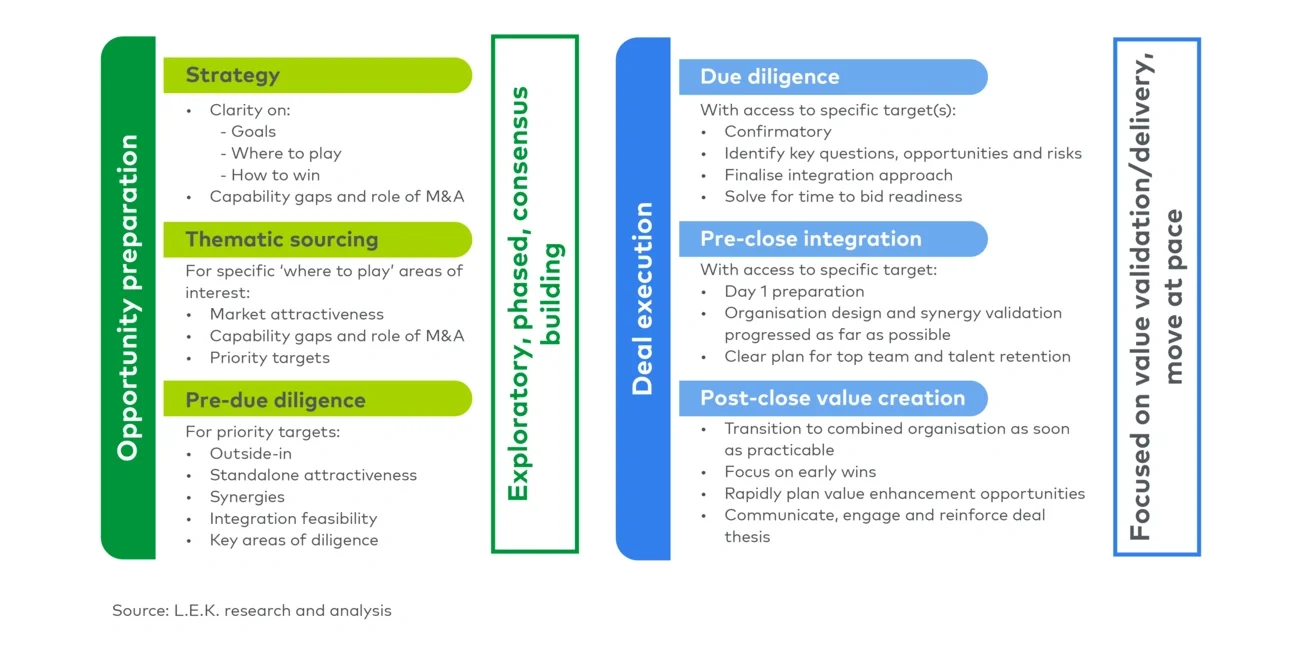

Aim to start from a detailed strategic roadmap as early as possible, with clarity on the role of M&A to deliver growth priorities, allowances for more proactivity in seeking out new opportunities and time created to manage hurdles (see Figure 3). To be more proactive, corporates should create a longer-term strategic roadmap, assess their capability gaps and be clear about the role M&A will have in delivering the roadmap. With a clear M&A strategy then in place, corporates can define the internal deal process, get the right team together, develop a playbook and carry out thematic sourcing of potential targets (e.g. active engagement with investment banks). For prioritised targets, investing early in a robust outside-in due diligence process can provide early insights into organisation, footprint and P&L structure, and allow for an initial view of value creation opportunities.

Figure 3

Best practice for early preparation to ensure M&A success

Image

-

Introduce a governance structure that supports rapid decision making and allows time for early alignment with the board. In addition to investing time to create a clear strategy roadmap early in the M&A process, it is important to ensure that senior management and the board are aligned on the strategic vision for the company. To reduce the need for education/alignment during a live process, it is critical that the board is aligned with not just the strategic vision for the company but also the role that M&A will need to play in delivering that vision. As part of this early education, it is important for the board to recognise there will be no ‘one perfect deal’ and that they must be prepared ahead of a specific opportunity for the possibility that compromises will need to be made. Management then needs to ensure that the board is briefed as early as possible on a potential opportunity to make governance hurdles more manageable and allow the board to pre-define the key diligence issues. To minimise board approval hurdles, corporates should consider the introduction of similar M&A governance structures as financial investors do (e.g. forming a subcommittee of the board that meets regularly during an M&A process similar to private equity investment committees).

-

When conducting due diligence, focus on the most critical issues only. It is important not to try to solve all questions in initial diligence; instead ensure there is focus on the big questions and achieve an early understanding on what matters the most in order to proceed. Three critical areas should be focused on: (i) validating the attractiveness of the target, (ii) confirming how value will be delivered through the transaction and (iii) identifying and addressing any ‘deal breaker’ risks. Management teams need to be comfortable that some topics will only be examined during confirmatory diligence and should not delay arriving at a valuation. It is important not to try to solve all the integration questions during initial diligence, as these can be addressed pre-close. This means that it is not necessary to include all business functions in the early stages of the process, and a targeted approach should be taken, including only those functions which will drive value.

-

Be willing to make the required upfront investments to ensure success. Once firms have defined their longer-term vision and the role that M&A will play, this provides clarity on likely levels of M&A activity. This can then be used to determine the investment needed to right-size the team. If M&A is only seen as likely to occur occasionally, then corporates need to be willing to outsource everything from defining M&A strategy and sourcing potential targets to carrying out due diligence and executing integration. Corporates must be honest about their own level of capabilities and recognise when external support is required. The involvement of external support can also provide independent validation to investment rationale and assumptions and can help management teams prepare for dealing with both internal and external hurdles (e.g. board meetings, antitrust submissions). In addition to recognising investment in talent and capabilities for both deal execution and post-deal integration, corporates also need to be comfortable with the idea that there are times when a particular deal may not always be successful, and that such a situation is okay because there will always be lessons learned from the experience. This spend is not wasted, and corporates must be willing to budget for failure.

-

Finally, to win deals, be ambitious in valuation. When defining the synergy opportunities for valuation, corporates should take an ambitious, top-down view of the potential. The detailed bottom-up approach should only be done during confirmatory diligence by the functional leads. They must maintain the original ambition where possible but use granularity to drive buy-in by the functional teams. Setting the top-down synergy opportunity should be done in conjunction with defining both the combined operating model and the integration strategy to ensure a realistic ambition.

How L.E.K. can help

For those corporates who are today finding themselves losing out on M&A opportunities, following our recommendations should result in improvements in their acquisition growth strategy. The benefits should include a more structured approach in moving from a defined strategic growth plan to a clearer M&A strategy to deliver those goals. This should result in better identification of opportunities, more flexibility and agility in delivering the plan, and less reliance on just one deal. We believe our strategy helps corporates gain more conviction around the valuation of the target and its ability to deliver value from the acquisition. Developing a better understanding of the strategic value of the target will ensure it is being best placed within portfolio and given the right level of investment in the future to deliver this value. Developing a better valuation of synergies will ensure the teams are being correctly measured against the right targets.

To find out more about our work in M&A, please contact us at strategy@lek.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2023 L.E.K. Consulting

Questions about our latest thinking?

Questions about our latest thinking?

Related insights

You might also be interested in these insights.

English