Enacted in 2021, the Infrastructure Investment and Jobs Act (IIJA) provides $1.2 trillion in funding for highways, transit systems, railways, the electric grid and broadband networks, as well as $65 billion in federal funding for water utilities, water infrastructure and environmental programs over the next 10 years (see Figure 1).

Executive Insights

A Drop in the Bucket: IIJA’s Limited Impact on the Water and Wastewater Industry

A Drop in the Bucket: IIJA’s Limited Impact on the Water and Wastewater Industry

April 5, 2024

Key takeaways

Over the next five years, funds from the IIJA will increase the annualized growth rate of the municipal water and wastewater industry from about 3% annually to roughly 4% annually, an incrementally positive but not transformative impact.

Administrative delays and lengthy project timelines will spread out the deployment of IIJA’s $65B for water infrastructure investments over a ten-year period, with annual spending reaching a peak in 2026-27, at about $10B each year (approximately $4B in 2023).

The IIJA will only increase the federal government’s share of water infrastructure funding from around 4% (average from 2018 to 2023) to roughly 7% (average from 2023 to 2028) – the key source of water infrastructure funding will continue to be utility ratepayers and local and state governments.

IIJA provides some funding that will accelerate investments into emerging contaminants, opening up new, niche opportunities in the industry.

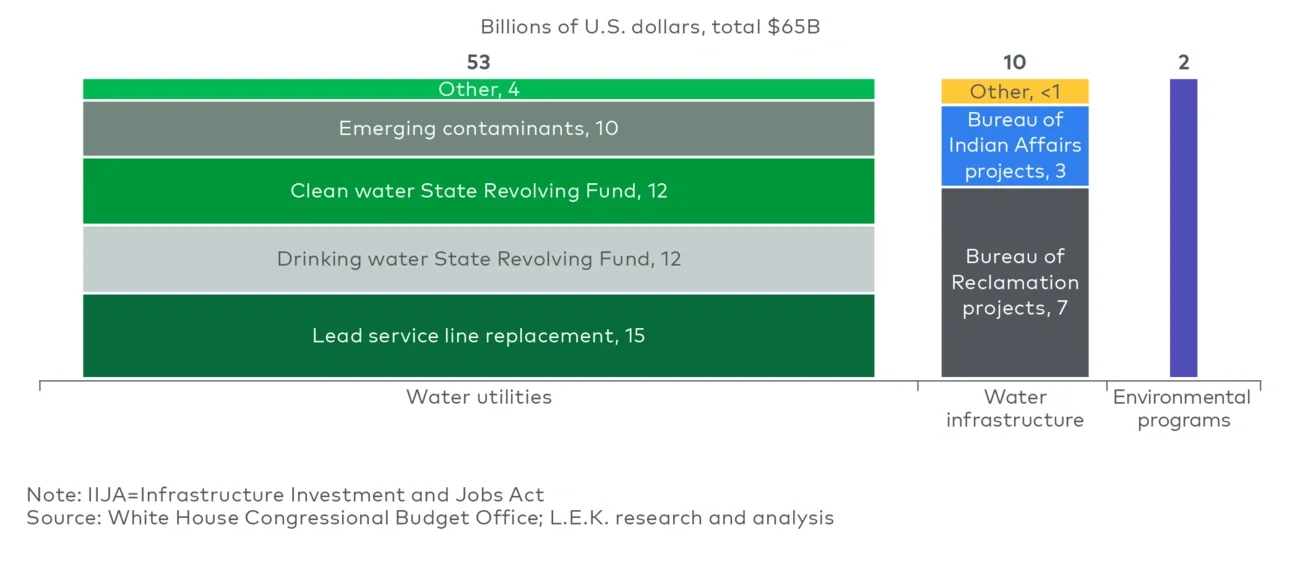

Figure 1

IIJA water funding by application

Image

Looking at the allocation areas of this funding, the industry’s forecast growth rate, the strength of state and local funding environments, and the timeline of funding deployment, L.E.K. Consulting finds that we can expect to see the effect of the IIJA on the municipal water and wastewater treatment sector to be positive, but limited in scope.

Funding water utilities through the IIJA

Water and wastewater utilities are the primary recipients of IIJA funding, receiving about $53 billion to cover three broad categories of projects:

- Drinking water and clean water ($24 billion) — Upgrading water and wastewater treatment plants, water lines and sewer systems

- Lead service line replacement ($15 billion) — Replacing old municipal-owned lead service lines with pipes made of nontoxic materials

- Emerging contaminants remediation ($10 billion) — Developing water treatment solutions for contaminants that are not yet regulated, most importantly per- and polyfluoroalkyl substances (PFAS), a category of “forever chemicals” ubiquitous in the U.S. water supply that have been shown to be linked to a variety of negative health effects

The IIJA also allocates about $10 billion of funding to building, repairing and maintaining water infrastructure in the western United States, including the construction and operation of dams, hydroelectric power, canals, water storage, flood control and water delivery systems.

Lastly, the package provides about $2 billion to a range of environmental management programs, such as the Great Lakes Restoration Initiative and the Chesapeake Bay Program, which monitor, protect and manage water quality within critical U.S. estuaries.

Breaking down the IIJA timeline

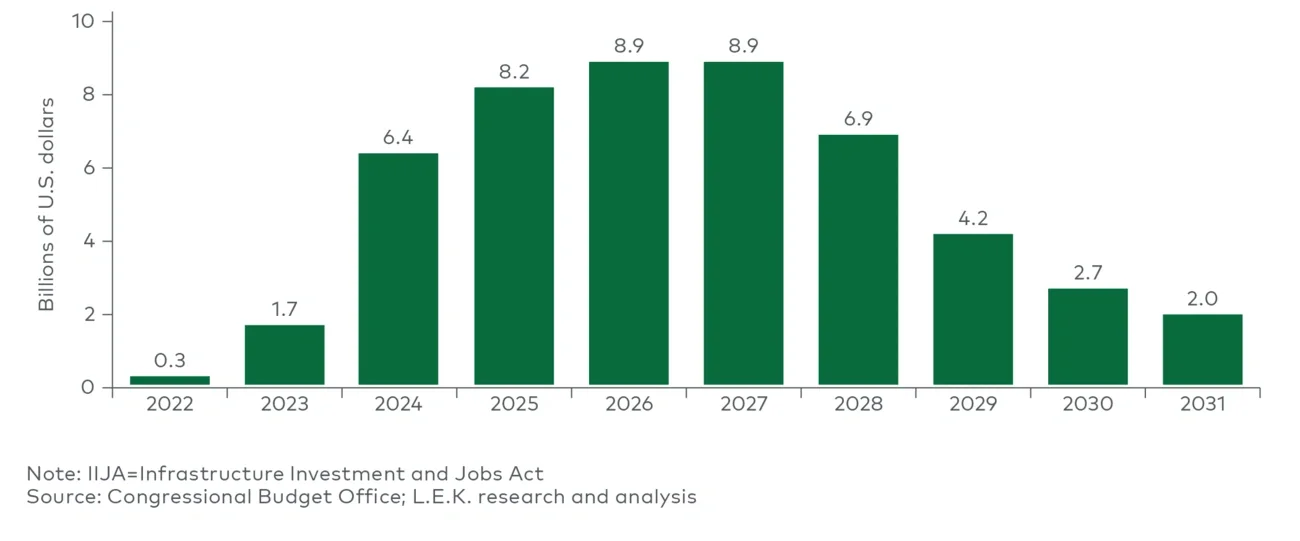

The IIJA’s $65 billion of water infrastructure funding will take longer to be fully disbursed than may be expected — about 10 years — as funds must go through multiple layers of government administration for approval, and long construction timelines can further delay rollouts. As a result, the IIJA’s contribution to water investments started small at approximately $1 billion per year in 2022; we can expect to see a peak in spending at about $11 billion per year in 2027 and then a tapering off through 2031 (see Figure 2).

Figure 2

IIJA-related water outlays (2022-2031)

Image

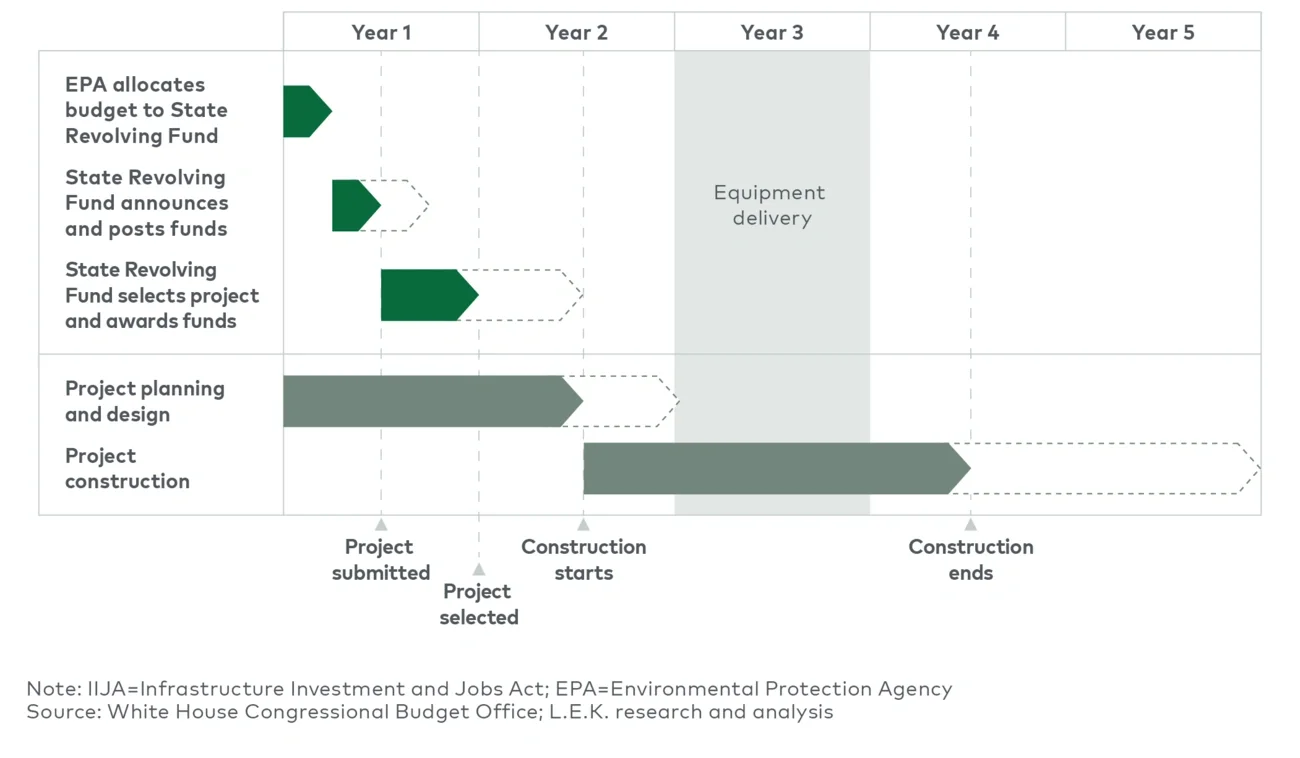

To understand why the IIJA funds will take about 10 years to be fully disbursed, it helps to understand the mechanics of the State Revolving Fund, the Environmental Protection Agency’s (EPA) primary tool for funding water projects. Once the EPA receives funding from the federal government, it takes one year, on average, before the funding is allocated to a specific project at the state level. It then takes another two to three years, on average, before construction is complete, equipment is delivered and the EPA fully pays all project stakeholders (see Figure 3).

Figure 3

IIJA funding allocation and project timeline

Image

The IIJA’s impact on market growth

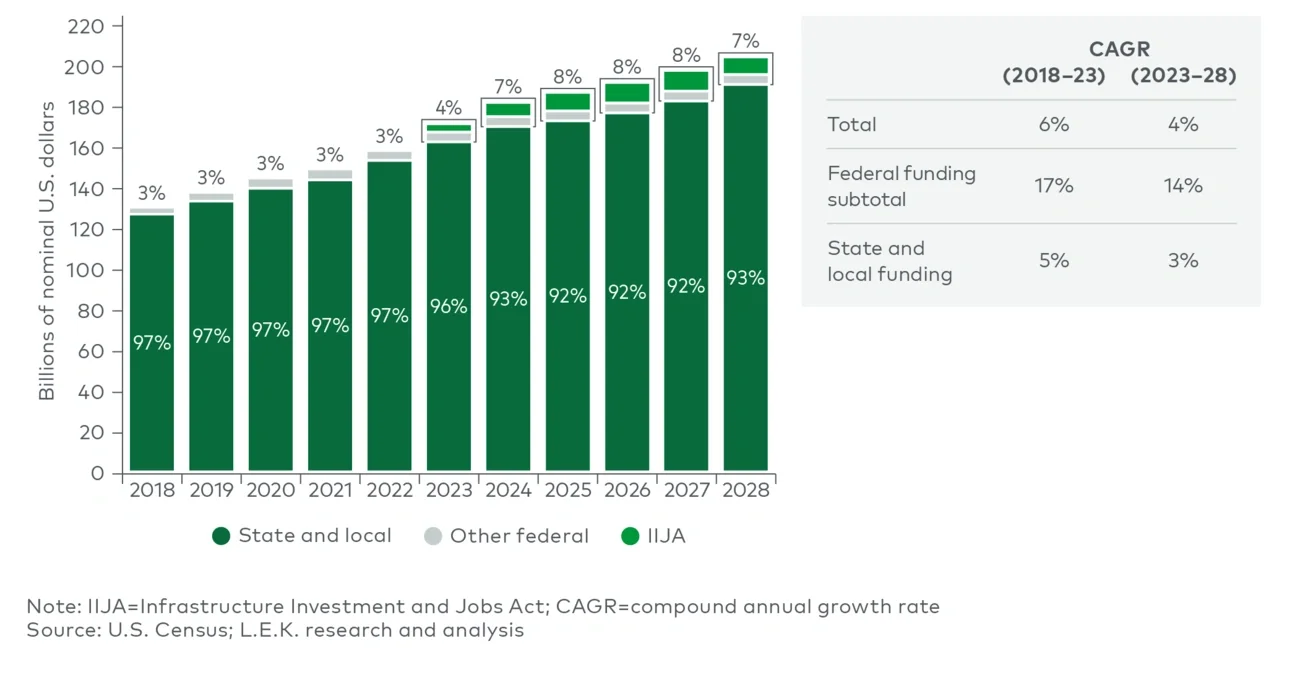

While $65 billion is a sizable contribution to the water sector, the IIJA’s lengthy timeline will dilute its annual impact on the municipal water and wastewater market’s annual spend of $170 billion.

Over the past five years, the federal government financed about 4% of all water infrastructure investments; with the IIJA, this share will increase to about 8% over the next five years. Consequently, we can expect to see the water industry’s growth rate rise by about 1% annually due to the IIJA, as the total market is expected to grow at about 4% annually through 2028 (see Figure 4).

Figure 4

Government funding for water and wastewater utilities (2018-2028)

Image

Water will continue to be funded locally

Though the IIJA will increase the federal government’s role in funding water infrastructure, state and local governments will remain the most important sources of funding in the water market. These entities collectively fund about 93% of water infrastructure, primarily from utility rates and fees as well as municipal bonds.

Funding from state and local governments is projected to grow 3% annually over the next five years as high-profile water incidents and infrastructure investment remain prominent issues for municipal rate setters.

Public awareness of newsworthy water incidents in Flint, Michigan, and Jackson, Mississippi, has raised the salience of underinvestment in water infrastructure. Local government officials, increasingly aware that underinvestment in water infrastructure puts them at risk for high-profile public relations disasters, are therefore more willing to approve rate increases to fund upgrades.

At the same time, state and local governments are also in a significantly better financial position than they were at the height of the COVID-19 crisis due to continued economic recovery, federal transfers and budget surpluses. In 2007, only 22% of states had a AAA credit rating, whereas 38% do today. With stronger balance sheets and a growing tax base, state and local governments are increasingly willing to use bond financing to fund water projects, which will ensure the continued steady growth of the market base due to local spending.

Strategic implications for investors

The water and wastewater treatment industry remains well positioned for growth due to strong fundamentals and a modest but positive impact from the IIJA.

For manufacturers and investors alike, this period of growth creates a new set of opportunities and challenges. To best manage the challenges, stakeholders should consider the following:

- Protect margins — The commercial and competitive environment remains largely unchanged in the wake of the IIJA — manufacturers still win through quality, expertise, availability and price. However, price has become more of an issue in this inflationary environment, and protecting margin gains through operational excellence will become critical to maintaining current levels of profitability.

- Identify high-growth niches — The IIJA will disproportionately allocate funds to the emerging need to remediate contaminants and replace lead service lines. Technologies such as filtration systems and trenchless rehabilitation will see an outsized benefit from IIJA funding, creating attractive investment opportunities for strategic and financial buyers.

- Hold through 2027 — Investors need not be concerned that the end of the IIJA will lead to a rapid slowdown in water market growth. Because the IIJA impact is spread out over 10 years, with spending peaking in 2027, investors can expect years of stable growth before a slight cooling off in the early 2030s.

Ultimately, water and wastewater remains an attractive market with ample opportunity for growth, both currently and as we look toward the later 2020s, when IIJA funds begin to taper off. Revitalizing existing infrastructure and making key investments to ensure the safe delivery of drinking water and treatment of wastewater will ensure activity remains consistent in the coming decades.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Questions about our latest thinking?

Questions about our latest thinking?

Related insights

You might also be interested in these insights.

English