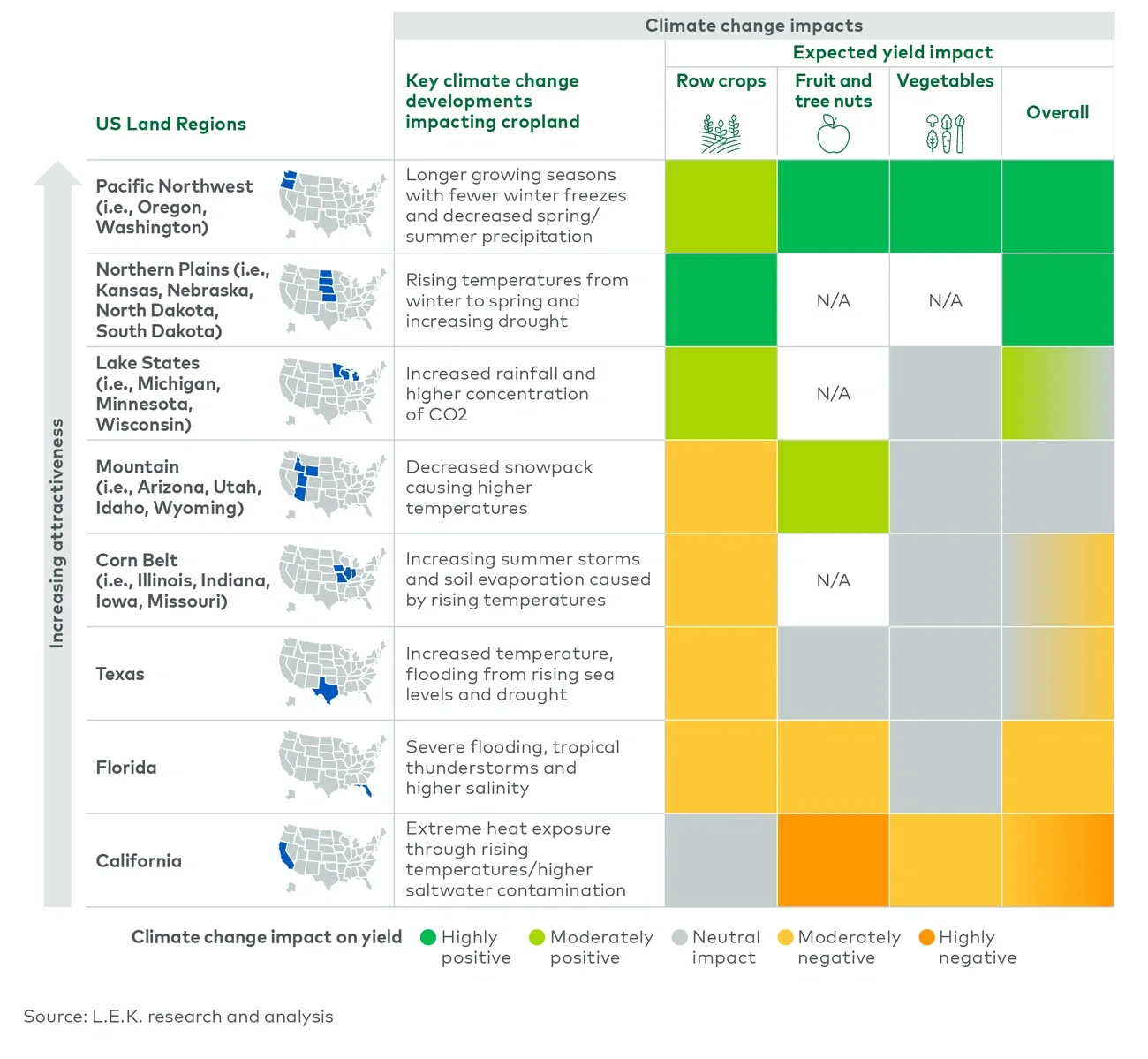

The impact of increasingly frequent and intense extreme weather events often captures media attention; however, what’s less reported is how climate shifts are impacting agricultural productivity in the U.S. and are likely to change the productivity of growing regions for key crops in the future. Indeed, climate shifts have already started to affect the cultivation map of numerous crops, and they are expected to continue to slowly alter underlying crop yields achievable in any given location. Some areas likely will see yields gradually trend downward, while other regions will see their productivity improve from shifts in climate.

While these changes will have clear implications for the future value of cropland, there are also implications for the agribusiness and food industries more broadly. For example, today’s networks of grain elevators and milling facilities, which are optimally located proximate to key crop growing regions, may need to shift in order to adapt to changes in crop production over the next several decades. And food companies may need to rethink where and how they will be able to source the ingredients they need as climate shifts impact which crops are best grown where. Some forward-looking companies are already beginning to develop long-term climate-related risk assessments. L.E.K. Consulting expects this to become an increasingly important strategic issue for companies and investors in the agribusiness and food sectors.

What climate shifts are expected in the U.S.?

The U.S. is getting warmer; since the late 1970s, the National Oceanic and Atmospheric Administration has observed that the average surface temperature across the contiguous 48 U.S. states has increased at an average rate of 0.32-0.55 F per decade. In fact, nine of the top 10 warmest years on record in the U.S. have occurred since 1998. In addition to the temperature rise, climate shifts have driven and are expected to drive more frequent and extreme weather events.

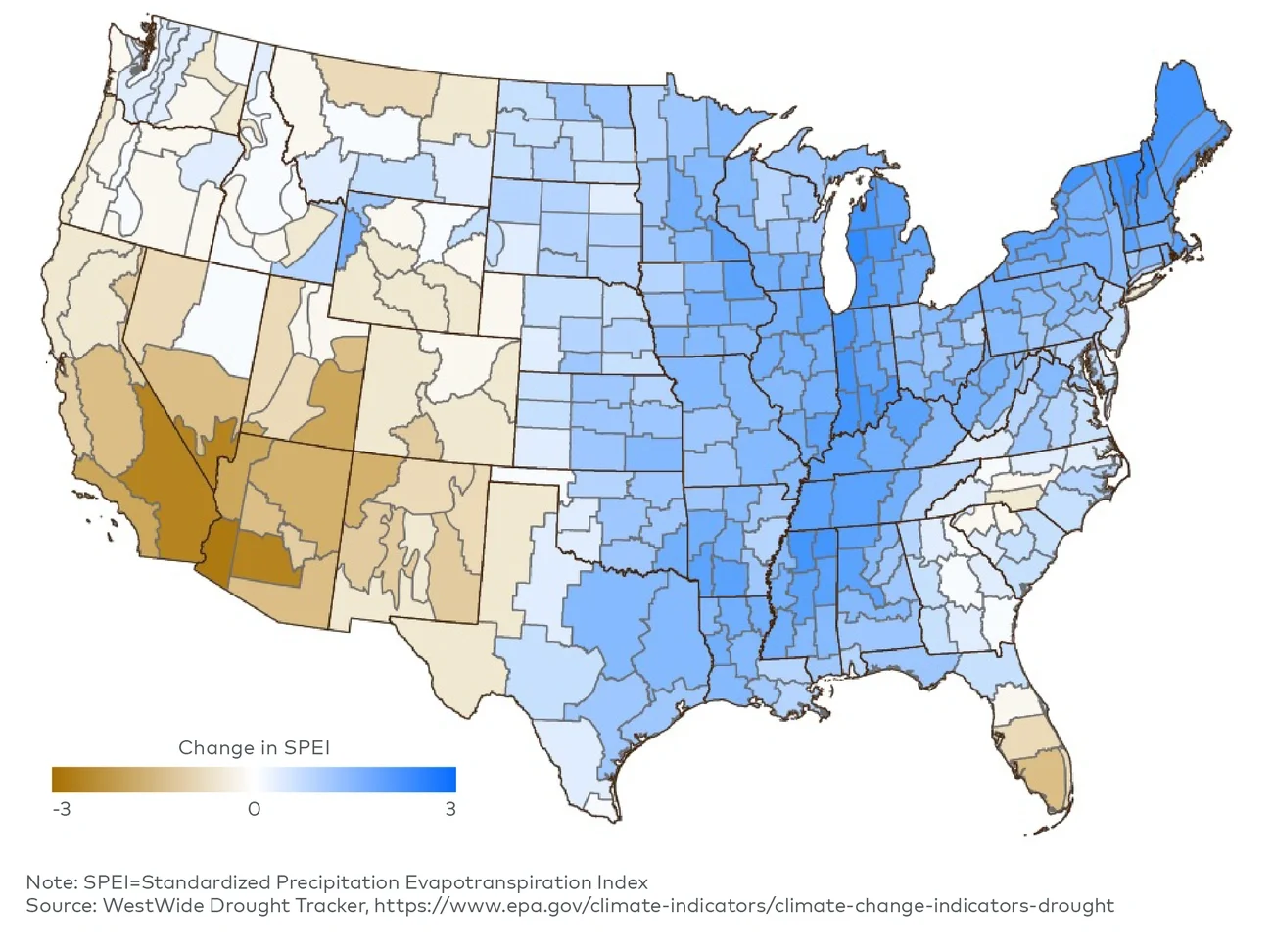

Firstly, certain regions, in particular Southwestern states, have seen less precipitation over the last century, causing and prolonging drought conditions. At the end of 2022, around 85% of the land in California was under severe drought, marking a long-term trend in decreased moisture (see Figure 1).