Setting the stage

It’s critical to underscore the point that farmers/growers have already been thinking about small “s” sustainability for decades. As stewards of their land — in many cases, land that has been passed down for generations — they have long sought ways to improve yields sustainably. And from a grower’s point of view, ensuring good soil health is the most important measure of truly sustainable cultivation practices. This will continue to be paramount at the farm level well into the future.

While brands and consumers are pulling growers toward more sustainability initiatives, there is growing pressure from investors, institutions and regulators that are increasingly pushing growers toward such practices. While farmers are interested in doing the right things, they will only make changes that they believe are sensible for their soil health and economically attractive to their business.

With that context, the findings from L.E.K.’s research around the five dimensions outlined above emphasize that many growers are indeed well informed and increasingly interested in further adopting sustainable cultivation practices. Growers’ awareness and usage of sustainable cultivation opportunities vary by technology/practice, with approximately 40% of growers indicating use of regenerative or sustainable cultivation practices and nearly 40% reporting use of crop biologics. Adoption of carbon programs, however, remains low at just over 10%.

Growers are very willing to try new and more sustainable crop inputs, technologies and cultivation practices; however, an attractive return on investment (ROI) is a requirement for growers to implement new sustainable practices/technologies. As an example, growers indicate that their primary reasons for adopting precision agriculture and crop biologics are similar or better yields and lower input costs for crop chemicals and fertilizers.

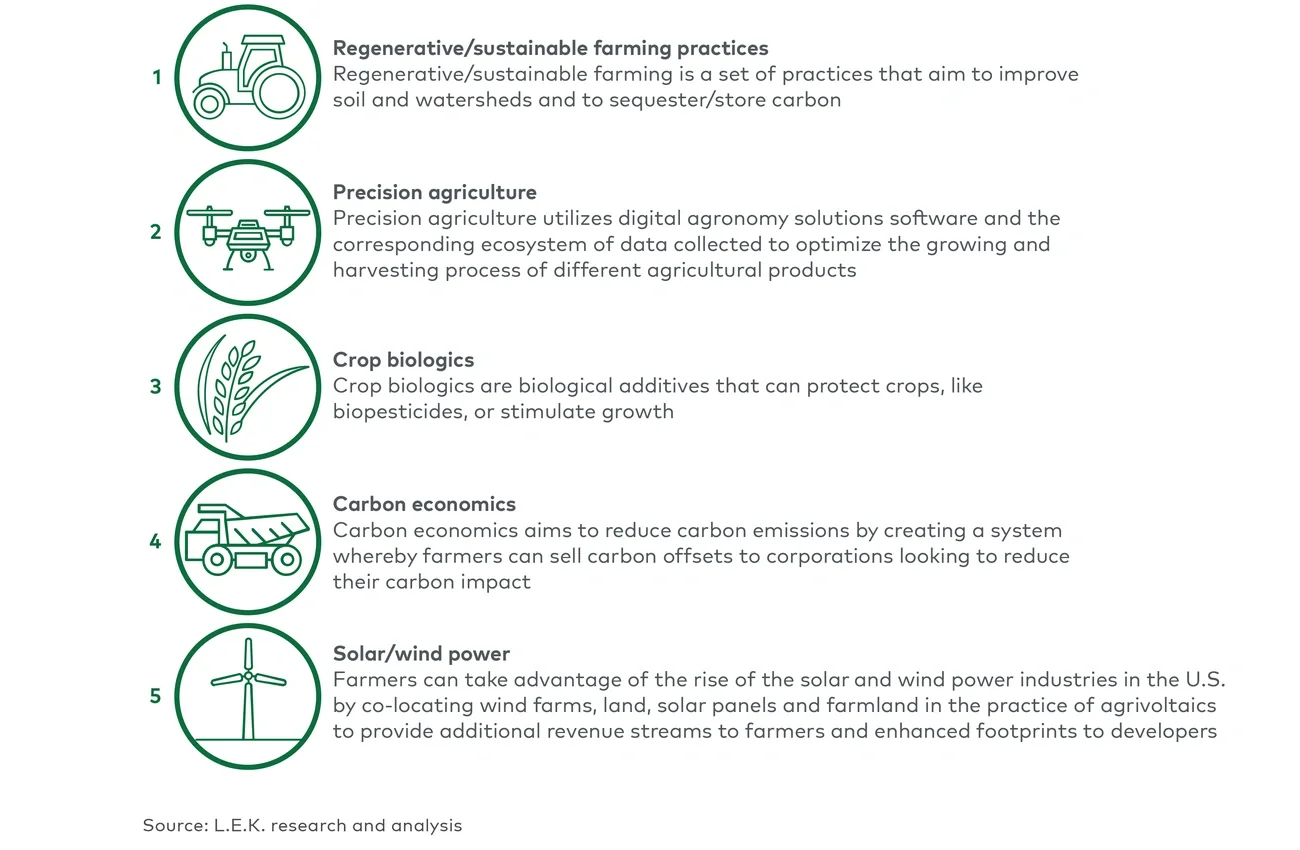

Five key dimensions of sustainable cultivation

Together, the survey and subsequent discussions surfaced the following core findings for each of the five sustainability practices and technologies:

1. Regenerative/sustainable farming practices — The adoption of regenerative/sustainable farming practices — which focus on improving soil health, managing watersheds and storing carbon in soil — is moderately high at approximately 40%. Growers cite improved yields and soil/crop quality as the key reasons they’ve adopted such practices, whereas sustainability, per se, is a secondary consideration. Specific regenerative practices with the highest adoption to date include conservation tillage, more diverse crop rotations and the use of cover crops to improve soil health and nutrition.

While the lack of agreement on industry standard as to what “regenerative agriculture” really means in practice is a key issue, other challenges cited by growers to adopting more regenerative practices include:

- Increased operational complexity

- Inconsistent effectiveness of practices across different crop types and regions

- The long time required (anywhere from three to five years) for such practices to yield tangible results

But despite the challenges associated with the implementation of regenerative farming practices, a combination of grower interest and downstream incentive programs from food brands is expected to help drive increased adoption going forward.

2. Precision agriculture — Awareness of precision agriculture solutions — which are used primarily to enhance crop quality — improve crop yields, avoid overapplication of crop inputs and improve harvesting efficiency, is also high. Notably, the adoption rate is higher among growers of specialty crops than row crops, the latter of which indicated that precision agriculture solutions have yet to deliver on impacting their input usage. By contrast, specialty crop growers were more likely to attribute decreased input usage to precision agriculture.

For growers, ongoing challenges to broader adoption of precision agriculture include the cost of such solutions relative to their impact, difficulty in measuring the results, etc. And from the crop input industry point of view, finding ways to improve grower education and training regarding the compatibility of digital agronomy tools and the capabilities of other advanced technologies will be critical to driving further adoption of precision agriculture solutions among growers in the future.

3. Crop biologics — The use of crop biologics as an important component of sustainable cultivation continues to grow globally. While adoption in the U.S. has been robust, certain overseas markets — Brazil, Spain and others — are seeing even more rapid adoption. And for growers in the EU, regulatory pressures on conventional crop protection chemicals have intensified rapidly, making the EU market ripe for adoption of alternative crop protection mechanisms such as biological controls.

Broadly speaking, biologics can be used to enhance both crop nutrition/fertility and crop protection against fungi and insect pests. Based on the survey findings, the adoption rates of biologics for crop protection and crop nutrition are fairly similar, with approximately18%-20% of growers either using biologics at scale or trialing with the intention to use at scale. However, findings also suggest that many growers have trialed biologics and opted not to roll out at scale, with roughly 30% of growers indicating having abandoned biologics that they’ve tried. And another 30% of growers have yet to trial biologics, suggesting that an untapped market opportunity still exists.

Growers who use crop biologics indicate they are relatively satisfied with what they use and expect to continue to increase their use of such crop biologics over time, especially for nutrition. That said, growers recognize that crop biologics can be costly and that it can be difficult to assess their impact and ROI. Confusing marketing claims and the complicated nature of their use and related storage are also barriers to adoption for some growers. However, the outlook is positive for biologics to become a more important complement to conventional chemistries in the future.

4. Carbon economics — The carbon market in U.S. agriculture remains nascent, with only 13% of all growers reporting having sold carbon credits over the past year. Through sustainable farming practices, including no-till/low-till, use of cover crops, etc., farmers are able to store carbon in soils. And measurement and verification processes have proven that increased soil carbon levels allow growers to sell carbon offsets to intermediaries and corporate counterparties seeking to offset their carbon impact.

Grower awareness and participation in the carbon market is greater among larger farms (20% participation) than for smaller farms (11% participation). While the absence of agreed standards for carbon measurement and verification, as well as the lack of a central marketplace for carbon credit trading, has been a major barrier to growth, farmers have indicated other reasons for not yet engaging in carbon economics. Key challenges cited by growers include:

- Difficulty in meeting market requirements for data tracking and reporting

- Inadequate economic incentive due to the low price of carbon

- Concerns about not getting paid for carbon already stored in soil

Despite those challenges, however, growers who do sell their carbon offsets on the market report relatively high levels of satisfaction with it. Moreover, growers believe the carbon market is becoming increasingly influential in incentivizing sustainable practices. But to drive further adoption, higher carbon prices are likely required.

5. On-farm solar/wind power — Adoption of on-farm renewable power generation is still in its early days but is expected to see steady growth as the cost of energy rises. Based on survey findings, adoption of on-farm renewables is higher for solar than wind, with 11% of respondents indicating use of solar already and another 13% reporting the intent to put solar generation in place within the next two years. By contrast, 5% of growers have already adopted on-farm wind power, with another 7% intending to start using it in the coming 24 months.

The results of this study clearly indicate there is a tremendous amount of interest, activity and investment going into different facets of sustainable agriculture, from both growers and the broader agribusiness industry. However, driving further adoption and impact hinges on solutions that are aligned with the economic incentives of growers.