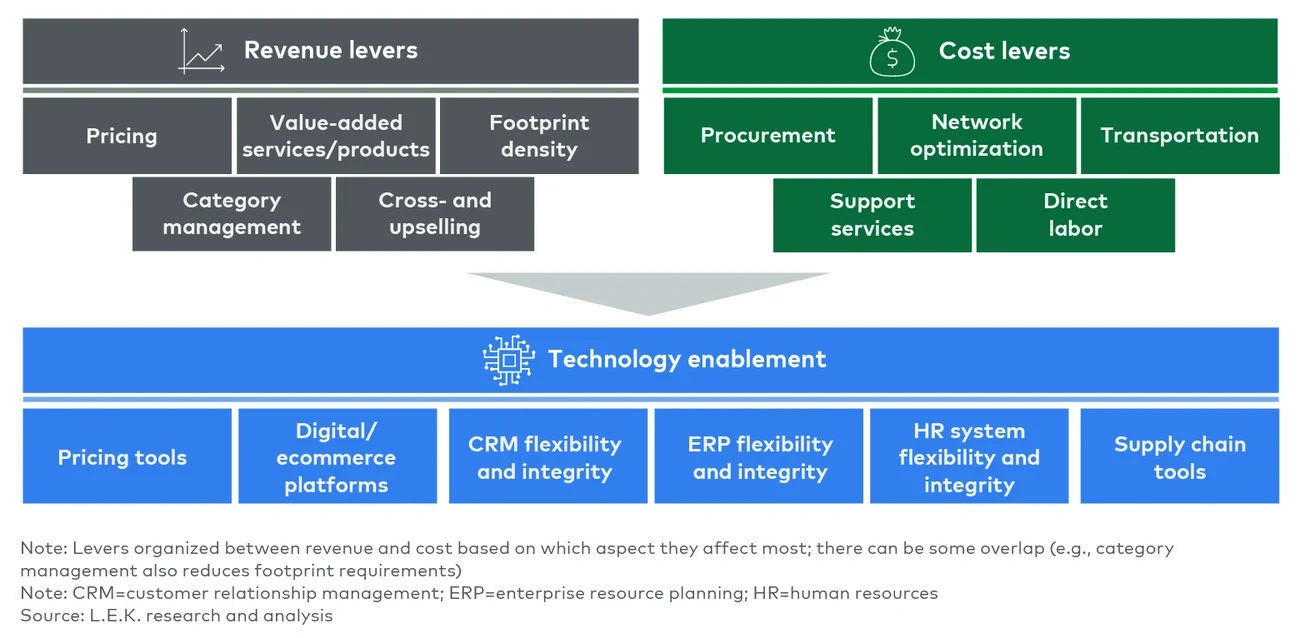

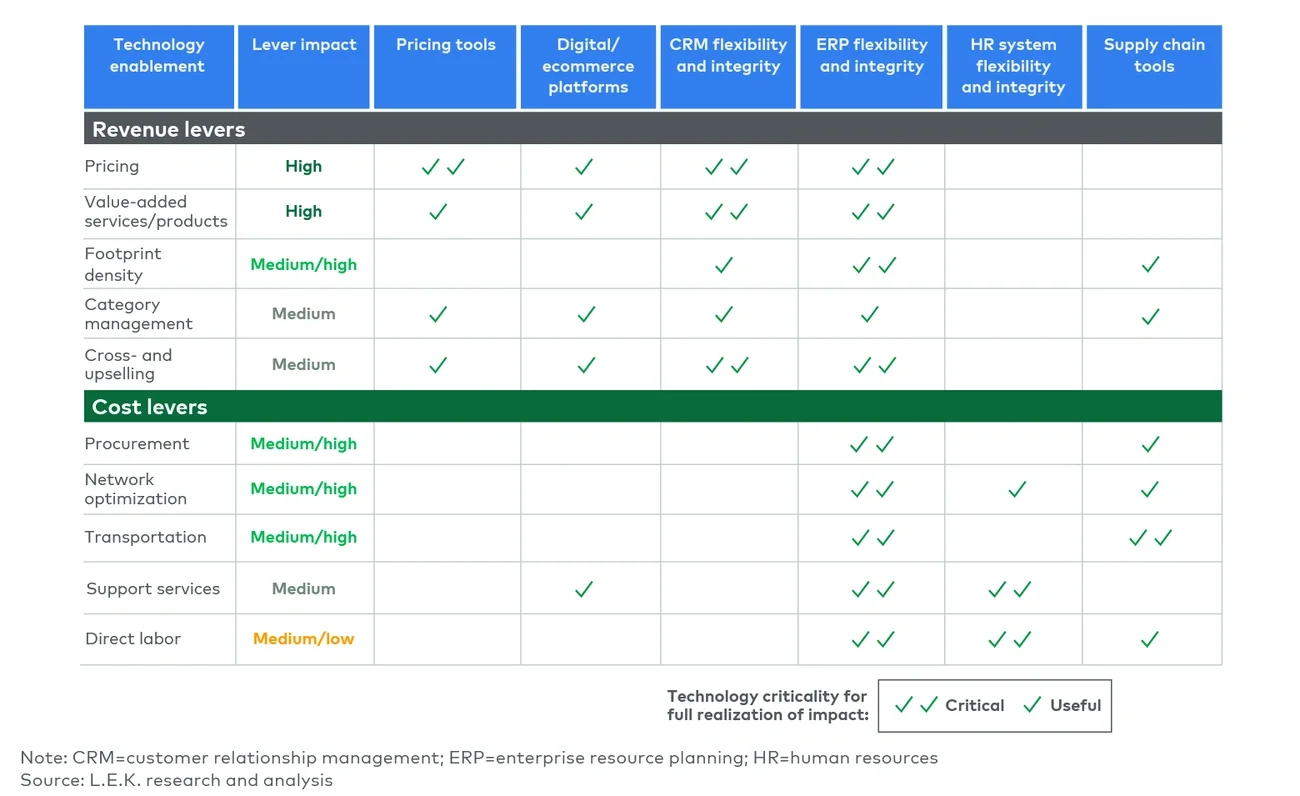

In the building and construction business, many distributors keep their return on capital high by earning healthy margins on high-turn products. This strategy has paid off especially well in recent years, even after accounting for post-COVID-19 pricing concessions. But the trend has continued long enough that industry watchers are left wondering whether it still has room to run.

In this Executive Insights, we’ll look at the conditions that have enabled distributors to expand their EBITDA (earnings before interest, taxes, depreciation and amortization) margins. Then we’ll examine where remaining opportunities for EBITDA margin uplift can be found and what distributors can do to capture them.

A supportive environment for margin growth

Public building products distributors have materially expanded their EBITDA margins over the last 10 years (see Figure 1).