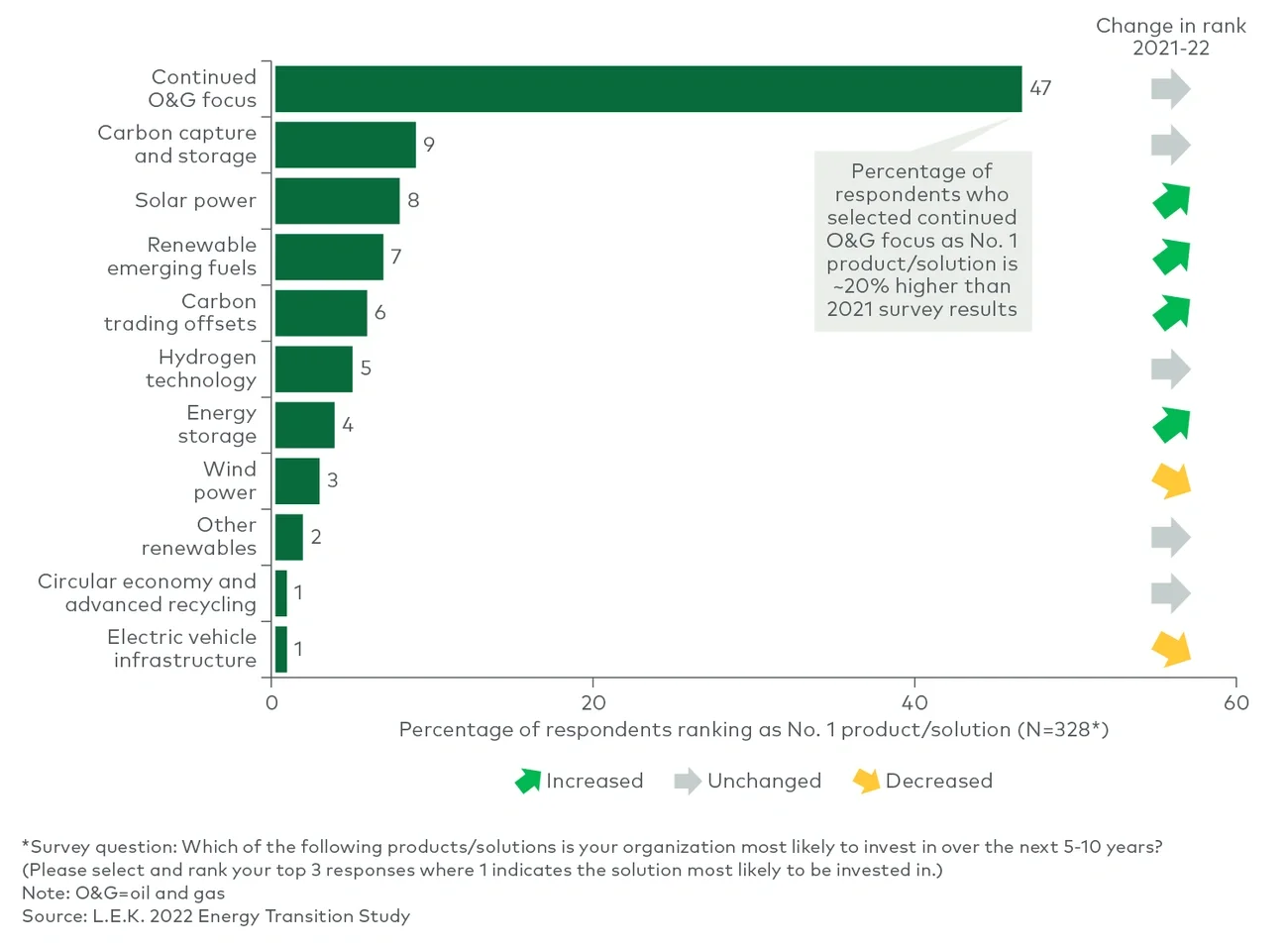

L.E.K. Consulting has identified six focus areas for the U.S. oil and gas industry that will drive the outlook for 2023.

Continued turmoil in the world of energy (in)security

The Russia-Ukraine conflict has placed significant pressure on the already strained global oil and gas supply chain and ensures that energy security will be the primary industry focus this year. The loss of Russian oil supply, coupled with limited OPEC spare capacity and recent production cuts, leads to persistence of global oil supply concerns.

In 2023, commodity prices are expected to recede in the first half of the year because of slowing public demand (though they will still remain relatively high because of limited supply chain), and the second half of the year is expected to bring price growth driven by the easing of COVID-19 restrictions in China, a continued risk premium on Russian oil, and a less aggressive approach on interest rates by central banks, which might have an impact on investments.

As a result of these dynamics in the global market, the U.S. is strongly positioned to fill the unmet global demand for oil and gas; dedicated, disciplined investments are being made toward that goal, mainly by companies with sufficiently healthy balance sheets and less dependency on external capital. Within the U.S., the Permian Basin in West Texas is expected to continue supporting this growth.

More gas on the energy horizon

The transition to renewable energy in the EU is expected to continue at a rapid pace, though natural gas demand will remain high as full fossil-fuel replacement will take several years. As the global market seeks alternative sources to Russian gas, the U.S. is poised to become the emerging reliable supplier of liquified natural gas (LNG). Bolstering supply chain replacement needs is the continued increase in global investments in new LNG infrastructure, which is expected to raise the global total LNG supply from approximately 380 million tons per year in 2021 to approximately 545 million tons in 2023 and approximately 570 million tons in 2024.

Bits to bytes: The AI era begins

Emerging technologies in the industrial Internet of Things (IoT), including digital twins, artificial intelligence (AI) and blockchain, will present innovative solutions to optimize operations, minimize risk and reduce greenhouse gas emissions in 2023. These solutions come at a time when the industry is facing challenges in the form of a critical skills shortage and tight labor supply, aging infrastructure that is increasingly vulnerable to forced outages, and heightened pressure from investors and regulators to prioritize sustainability. Key players in the digitization trend include:

-

Digital twins – Mimic and monitor assets to enhance reliability, logistics, and performance, with increasing adoption across the oil and gas value chain, as indicated by industry leaders in our most recent L.E.K. Industrials Digital Survey

-

Manufacturing execution system (MES) – Enables refineries to optimize production by integrating equipment performance metrics

-

Digital asset management – Leverages data-driven solutions to automate processes like testing, inspection, and certification and decreases costs associated with monitoring equipment

-

AI-based technologies – Bolster equipment monitoring and inspection capabilities with tools like drones or miniature fiber-optic sensors

-

Blockchain – Provides transparency and traceability by simplifying oil and gas trading, shipment tracking, documentation, and payments

Decarbonization as a service: The new frontier

The push for carbon capture, utilization and storage (CCUS) should continue robustly in 2023, as the market trends toward sustainability and favorable policies supporting decarbonization further develop the practice as a service business. In addition to increased awareness and market pressure to implement more sustainable practices, recent public policies are pushing CCUS through tax credits, rebates and other incentives to reduce emissions.

The $370 billion 2022 Inflation Reduction Act is the largest climate-change-dedicated spending package in history, with $35 billion to $40 billion allocated to carbon initiatives. Combined with $8 billion to $10 billion from the 2021 Infrastructure Investment and Jobs Act, a total of $45 billion to $50 billion of federal funding will go directly to CCUS projects.

Oil and gas operators, both upstream and downstream players, are well positioned to develop “decarbonization as a service” (DaaS) given their sub-utilized infrastructure and experience dealing with the transportation, storage, and trade of similar molecules. On the whole, businesses that provide DaaS are increasing in number in sectors like transportation, storage and sequestration; private equity and venture capital investments in carbon accounting and offset companies nearly tripled in recent years and are expected to continue increasing rapidly. This growth is fueling the monetization of DaaS in areas like selling carbon credits, transporting and disposing of captured CO2 molecules, and performing CCUS for carbon offsetting purposes.

Fueling a greener future

There is an increasing transformation of energy systems away from fossil fuels to renewable and clean energy, with growth primarily seen in sources like:

-

Renewable green diesel (RGD) – Production is expected to continue to grow in 2023 after a 90% surge in 2022

-

Sustainable aviation fuel (SAF) – Increasing investments are being made by traditional refiners such as Valero, Phillips66 and Marathon for production of SAF, while airline companies such as United Airlines, Iberia Airlines and British Airways continue to make commitments on adopting an increased share of SAF in their respective fleets

-

Renewable natural gas (RNG) – More gas utility operators are taking steps to incorporate RNG into their distribution systems and enter into joint ventures focused on the expansion of RNG production capacity with multiple players

Government incentives for cleaner fuels like the Environmental Protection Agency’s renewable fuel standard and California’s low-carbon fuel standard are driving the conversion, along with corporate sustainability goals set by companies attuned to customer awareness. Investments in refinery capacity for renewable fuels are growing, reaching approximately $12 billion in 2022, up from approximately $1 billion in 2019. Also seeing rapid growth is renewable diesel production, having surged 90% in 2022 with expectations that it will continue to increase throughout 2023.

Rethinking portfolios with decarbonizing investments

As the oil and gas industry matures and increases in complexity, it has become more important than ever that legacy oil and gas companies prioritize the efficient deployment of capital to remain competitive as the market shifts away from hydrocarbon energy over the long-term. High current oil prices have created financial opportunity for portfolio optimization, and the drive toward green energy and sustainability initiatives correlates with the plateauing of oil demand by 2030, creating an attractive financial window.

Key enterprise strategies for portfolio optimization include:

-

Capital allocation efficiency – 2023 will continue to see the focus of most exploration, development and production operators on maintaining capital discipline and seeking maximum financial performance of their respective operations; some public companies have announced that dividend payments and payment of financial obligations will remain a top priority, while still keeping a cautious approach to business expansion

-

Investment in green tech – Seeking investments in CCUS, green hydrogen, and renewable fuels diversifies portfolio risk and establishes participation in high-potential markets, as it helps in achieving oil and gas companies’ own decarbonization goals

-

M&A/A&D strategy – With a favorable environment for consolidation, M&A/A&D activity is expected to rise as value expectations on buyers’ and seller’s sides align; considerations around financial and operation performance will prevail, while the movement toward low carbon intensity footprints continues to increase in relevance in overall investment screening criteria

By providing reliable hydrocarbons in a time of energy insecurity while also looking ahead to alternative and renewable fuel sources, oil and gas companies will see a time of opportunity in 2023 for exploration and expansion in preparation for continued shifts in the industry.

To learn more about market factors and key themes driving oil and gas in 2023, please contact Franco Ciulla or Nilesh Dayal at energy@lek.com.