Key takeaways

-

Although COVID-19 is having a significant impact on the fitness industry, it has a strong track record of growth and has proved resilient to economic downturns.

-

As clubs reopen, many intend to implement policies to protect workers and members that will affect both revenues and costs.

-

As fitness clubs critically evaluate their business models in a post-COVID-19 world, we offer strategies that focus on retaining and re-engaging members for the long term; growing revenue per member; and optimizing studio footprint.

-

Gyms and boutique studios that proactively adopt new ways to retain customers and increase revenue per customer are best placed to succeed when the virus’s impact on the economy subsides.

As COVID-19 gripped much of the world, fitness club and boutique studio locations went into complete shutdown. It is widely expected that some gyms will not survive. Independent clubs and smaller chains will be hit the hardest, and some large chains may also shutter locations. Gold’s Gym recently filed for bankruptcy and reports have emerged that 24 Hour Fitness and Town Sports are contemplating bankruptcy. Others have taken swift action to close locations ― for example, YogaWorks is closing all of its New York studios.

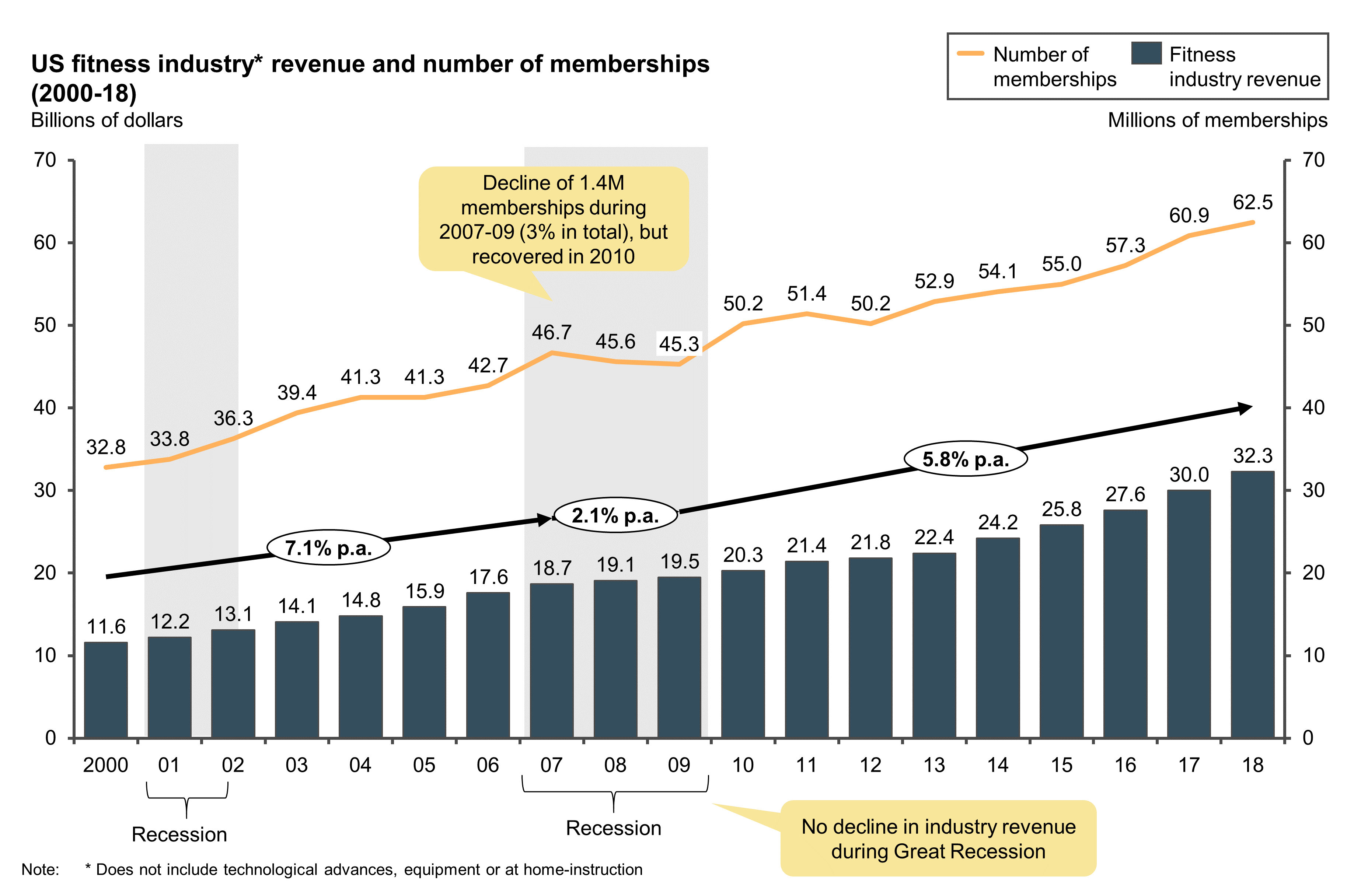

Despite the initial severe effects of the pandemic, the fitness industry has a strong track record of growth and has proved resilient to economic downturns. In fact, the sector’s revenue grew through both of the past two recessions (see Figure 1).

While cutting costs where they can, studios and gyms are also focusing on near-term tactics to retain memberships. Many locations have frozen payments during closures to appease customers, and boutiques especially have launched digital streaming versions of their popular classes (e.g., Orangetheory At-Home).

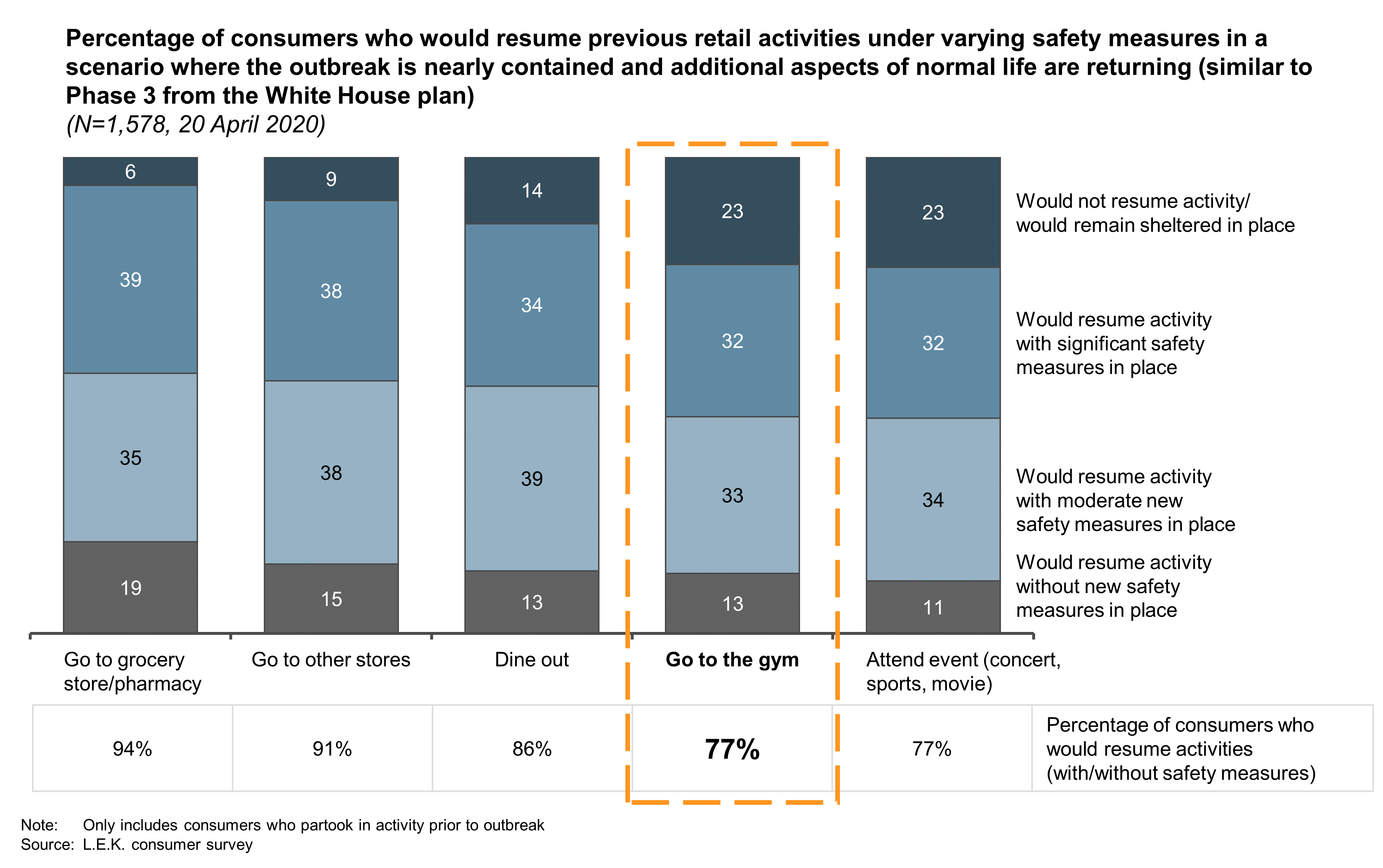

Government guidelines are dictating the speed of re-opening, but safety measures such as strict capacity limits and consumers’ hesitancy to resume pre-COVID-19 fitness club activity (see Figure 2) mean the sector’s revenue and profits are likely to remain depressed for some time.

As clubs reopen, they will look and feel quite different than they did in early March. Many gyms (e.g., Crunch, Equinox, Gold’s Gym, LA Fitness) intend to implement a number of restrictive policies to protect workers and members. These measures will change the unit economics of clubs as long as they are in place, as they impact both revenues (e.g., limiting number of guests in the gym at one time) and costs (e.g., adding staff, products and services to keep facilities and equipment safe).

L.E.K. Consulting’s research and analysis have determined that, as fitness clubs critically evaluate their business models in a post-COVID-19 world, seeking ways to rebuild and configure the top line will be critical. We’re not suggesting they fundamentally change what they stand for or undermine their core value proposition (that could be disastrous), but implementing the right changes could deliver meaningful value. To this effect, we offer various strategies around three key levers:

- Retaining and re-engaging members for the long term

- Growing revenue per member

- Optimizing studio footprint

Retaining and re-engaging members for the long-term

Gyms and boutique studios are already leveraging near-term strategies to minimize membership loss. They will also need to attract members back into the studio after re-opening, and to re-engage participants with non-membership concepts (i.e., classes/other packages). They can use several avenues to facilitate this in a post-COVID-19 environment such as digital fitness and tiered membership models.

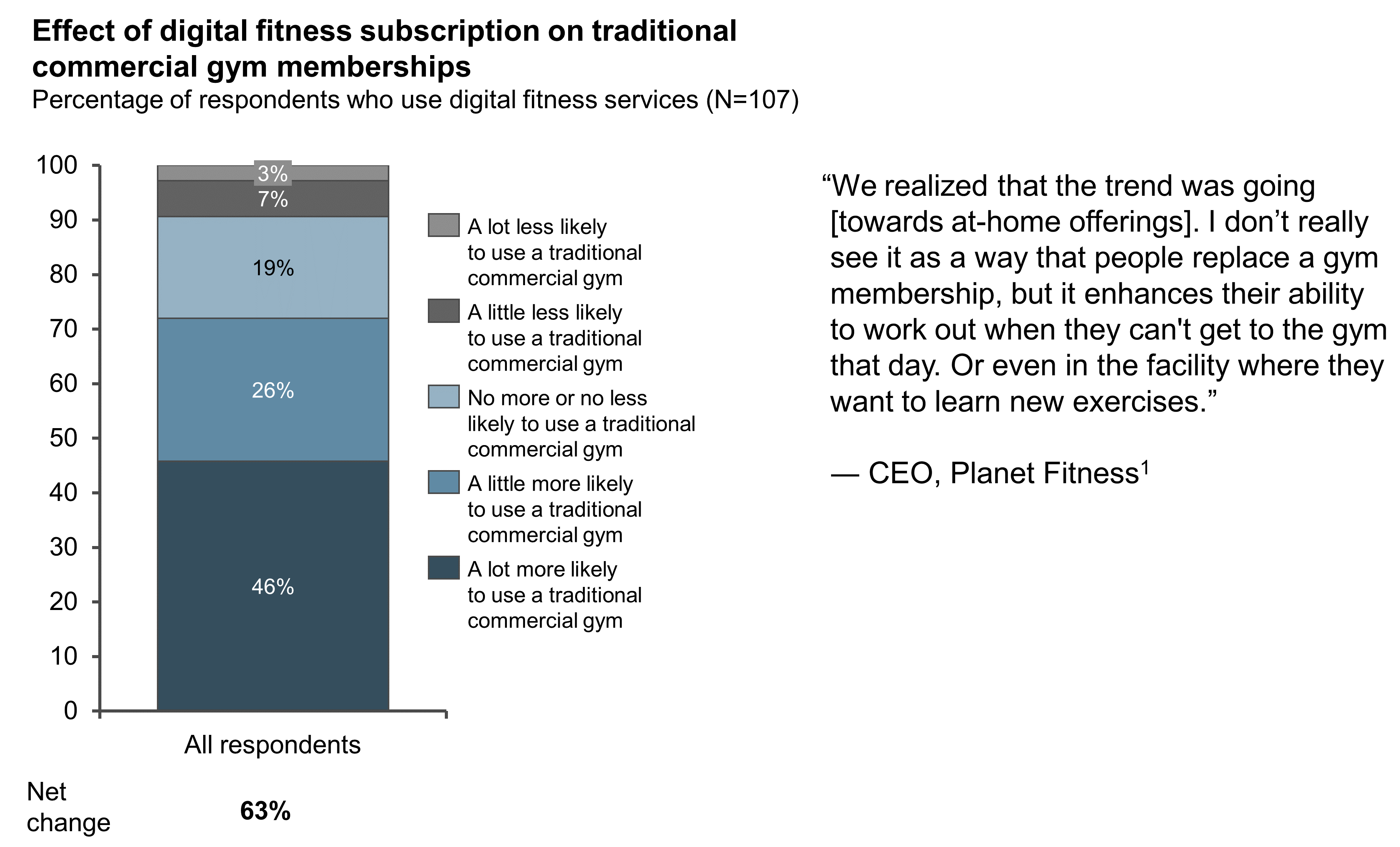

Digital fitness. While consumers have readily embraced innovative digital, at-home fitness offerings (e.g. Peloton, Mirror, Tonal), studios and gyms have engaged with this trend slowly, due to the fear that digital services would de-value the in-studio experience or add too much complexity. However, our research has consistently shown that digital fitness complements rather than replaces the physical experience: the L.E.K. Digital Fitness Survey shows that approximately 90% of digital fitness subscribers state their likelihood to use a traditional gym is either the same or greater than before their digital fitness usage (see Figure 3).

As the COVID-19 pandemic has accelerated consumer demand for digital at-home fitness, location-based clubs must now seriously consider how they might adapt their business model. The key is establishing at-home programming not as a replacement for the in-studio experience, but as a complement to it ― for example, by providing options that improve convenience and increase participation, delivering incremental and more tailored classes not offered in the studio, and by enabling enhanced community engagement.

A digital offering can clearly be a bridge spanning the period of social distancing ― one that sustains member engagement and serves as a revenue source. During and after reopening, though, we expect complementary digital experiences to continue playing an important role as some customers will feel safer staying at home – and, some will simply have realized they value an at-home model, at least some of the time. Studios and gyms can incorporate digital fitness into their business models in various ways, including the following:

- Offering digital classes or training: offering remote coaching from the gym, workout guides, cardio programs, or at-home classes or training with or without equipment (e.g., Barry’s At Home offers classes that don’t require equipment, as well as others that do)

- Hosting challenges and events: fostering healthy competition and a sense of community among members (e.g., Peloton’s Annual Challenge)

- Enabling management and monitoring: Tracking workouts, monitoring progress and providing leaderboards to share and compare with others (e.g., Orangetheory’s app that integrates with wearable fitness tech, providing these and other features)

- Creating digital community groups: Offering members a forum to connect with others and foster a sense of community (e.g., the Strava app, which refers to itself as the “social network for athletes”)

Tiered membership models. For gyms with membership programs, introducing or expanding a tiered membership approach could enhance member retention and growth. Tiered options give consumers more choices to find the cost/benefit model that meets their needs and budget, versus a one-size-fits-all approach that might not work for them. This will be especially important in seeking to re-activate customers post COVID-19, when many are likely to be reining in their expenditures and shying away from financial commitments that don’t offer them great value.

Think of gym memberships as airline tickets: people who want the cheapest route from point A to B will buy basic economy, while those who want greater service can add on perks such as preferred seating, extra baggage and expedited boarding. Some gyms have already offered limited tiered membership options, offering features such as multi-club access, training, and classes. This is a time to expand or reconfigure those tiers to maximize membership retention.

Tiered memberships are also a good way to monetize digital, at-home services. For example, gyms might consider:

- A free, basic digital membership with access to an app with pre-recorded classes

- A moderately-priced premium economy digital membership with access to special offerings (e.g., personal training, live-streamed classes)

- A full-priced premium omni-channel membership that combines digital specialty and in-studio access

In the immediate term, many gyms and studios will need to embrace promotional pricing when they reopen in order to quickly attract customers lost during the downturn. Offering the right incentives without alienating existing customers and permanently resetting to a lower pricing structure will be important in configuring customer acquisition strategies.

Growing revenue per member

With the pandemic placing constraints on membership bases, growing revenue per member via value-added ancillary services will be critical to driving the top line. This shouldn’t be done by adding a haphazard “kitchen sink” array of services, but rather by making additions that are strategically relevant and have integrity with respect to the brand’s core value proposition. Done right, new revenue streams should feel natural and highly brand consistent to the consumer, and ultimately should add value to the business concept.

Potential areas in which to explore ancillary revenue opportunities are described below. These extend beyond the digital, at-home fitness strategies we highlighted earlier but share their ability to generate incremental revenue.

Nutrition and weight management. Gyms and boutiques have been attempting to move into the sports nutrition and weight management spaces for some time with mixed success. The accelerated decline of specialty retail during the COVID-19 pandemic will create a unique market gap that gyms and studios could take advantage of ― making a reassessment of entry into the sports nutrition/weight management space worthwhile.

Historically, the specialty retail channel occupied by GNC, Vitamin Shoppe, and independent health and wellness shops has met consumers’ needs for these products and provided guidance in navigating a crowded and complex array of product choices. GNC and Vitamin Shoppe together account for an estimated $3 billion of retail sales in the U.S. However, today this channel is under threat. For example, GNC, the largest vitamins, minerals and supplements (VMS) specialty chain, received a delisting warning from the NYSE in April 2020.

In the place of such retailers, fitness concepts that have built trust with their members and have a distinct culture or health perspective could offer sports nutrition solutions that are highly consistent and tailored to their fitness proposition. These could include custom products under the concept’s brand name, or a tailored selection of complementary third party brands (e.g., a partnership with a virtual weight management program such as Noom). Combined with convenient locations for pick-up, auto-replenishment, and consultation from trusted trainers, the proposition could be compelling to a meaningful segment of members.

Structured weight management. During COVID-19, consumers are seeking ways to eat well within the confines of social distancing. Health-positioned meal kit companies such as Blue Apron and Sun Basket that had seen their popularity wane recently have reported significant sales growth after stay-at-home orders went into place (Blue Apron’s Q1 earnings call mentioned a positive year-over-year growth outlook after two years of declines).

The renewed demand for pre-packaged healthy meals is introducing new consumers to the concept, and many of these consumers have not yet settled on a brand. This could present a long-term opportunity for gyms and studios to partner with structured weight management providers to provide nutrition services and packaged meals to clients. Some businesses have already started down this path. Specialty gyms have offered meals through partnerships for years ― many CrossFit gyms around the country have partnered with MegaFit Meals to supply pre-packaged meals and supplements to complement their strenuous workout regime.

Fitness tech and equipment. The growth of at-home fitness creates opportunities for equipment-centric fitness concepts to sell equipment that enables their members to participate at home. For example, SoulCycle’s new “At-home bike” includes pre-recorded and live versions of Soulcycle’s trademark in-studio classes in an attempt to recreate the community experience in the home. “Barry’s At Home” classes offer specific classes that utilize their branded resistance bands (available for purchase on their website).

For gyms and studios that have not yet done so, this is an important time to consider integrating their classes into fitness tech wearables. Fitness tech was already a growing trend in the market pre-COVID, and its traction is accelerating as consumers seek to track their fitness progress outside the club.

Optimizing studio footprint

COVID-19 has fundamentally changed the way studios need to think about real estate strategy. Social distancing requirements will reset attendance levels, thus changing the unit economics of each studio. Owners should recalculate the optimal size for each location and think strategically about relocating or closing existing studios.

Re-assessment of existing footprint. Fist, operators need to reassess their existing portfolio. This doesn’t necessarily mean rationalizing the number of locations. Studios and gyms should reconsider key economic assumptions around each of their locations ― for example:

- Foot traffic: Studios near shopping centers, grocery stores, or office parks—popular locations ― may see significant foot traffic decline. Grocery store chains such as Kroger have reduced capacity by 50%, while Walmart and Target have gone further, reducing capacity by 80%. Conversely, studios located in or near residential areas may see increased foot traffic as work from home normalizes, even post COVID-19.

- Capacity constraints: Operators should run their unit economics with new scenarios reflecting reduced intra-studio capacity for the short and medium terms. For example, many re-opened gyms are operating with a rule of one person per every 200 square feet (versus a pre-COVID-19 ratio of one per 60) and allowing only every other or even every third machine to be occupied at a time.

New opportunities. While they face challenges, fitness operations also have significant opportunities to repurpose existing spaces and expand into new areas.

- Re-visiting previously costly locations: Commercial real estate has doubled in price over the past decade, putting some areas out of reach for new studio locations. The coronavirus is widely expected to tamper this growth, if not reverse it in many areas. This might enable operators to upgrade facilities to find better locations and/or to increase space to handle new social distancing requirements while not increasing overall real estate costs.

- Re-purposing existing facilities: While some studios might have to use bigger spaces to meet capacity constraints, others might find cost-effective ways to use smaller studios in favorable locations, by re-orienting interior spaces. Studios with significant vertical space might consider adding a second level of machines. Others might consider decreasing large lobbies or locker rooms to make more room in the workout space.

Conclusion

COVID-19 is having a significant impact on the fitness industry, but the industry is resilient, and gyms and boutique studios that proactively adopt new ways to retain customers and increase revenue per customer are best placed to succeed when the virus’s impact on the economy subsides.

10292020091002