In January 2020, the Department of Health and Human Services (HHS) issued a public health emergency (PHE) soon after the first cases of COVID-19 were detected in the U.S. In March 2020, Congress passed the Families First Coronavirus Response Act (FFCRA), which, among other provisions, put in place controls to ensure those in need had access to care during the pandemic. These provisions included:i

-

A temporary increase of 6.2 percentage points in the Federal Medical Assistance Percentage (FMAP) — the federal government’s share of Medicaid costs — to qualifying states

-

A maintenance of effort (MOE) protection, also known as “continuous coverage,” which prevents states that receive the increased FMAP from terminating people’s Medicaid coverage during the PHE

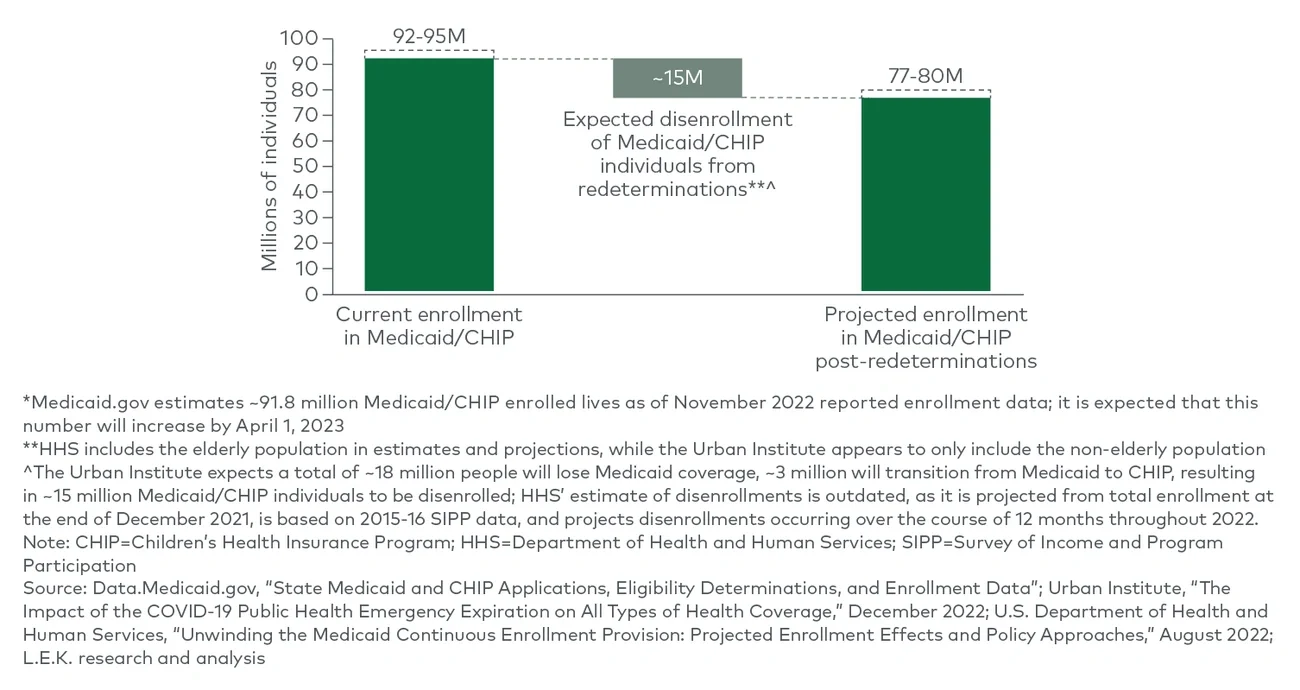

The PHE was renewed 12 times in 90-day increments, keeping in place the increased FMAP and MOE protections for Medicaid, before President Joe Biden announced its end date of May 11, 2023. During this same time, estimated enrollment in Medicaid and the Children’s Health Insurance Program (CHIP) approached 92 million as of November 2022, an increase of over 21 million since February 2020;ii however, on Dec. 29, 2022, President Biden signed the Consolidated Appropriations Act of 2023. This Act allows eligibility terminations to begin on April 1, 2023, permitting states to begin initiating renewals that may result in eligibility terminations as early as Feb. 1, 2023, or at the latest by April 2023, giving each state 12 months from its starting point to initiate all renewals, and 14 months from its start to complete all renewals.iii

Additionally, the act granted a gradual phaseout of the 6.2 percentage point FMAP enhancement beginning in April 2023 and ending on Dec. 31, 2023.iv Now the healthcare system is preparing for the far-reaching ramifications that redeterminations will bring. In this Executive Insights, L.E.K. Consulting discusses the implications of upcoming Medicaid redeterminations and considerations for payers, providers and patients.

By the numbers: What could Medicaid redeterminations look like?

There are three main variables defining what the impact of Medicaid redeterminations will be:

-

How many people will lose Medicaid coverage?

-

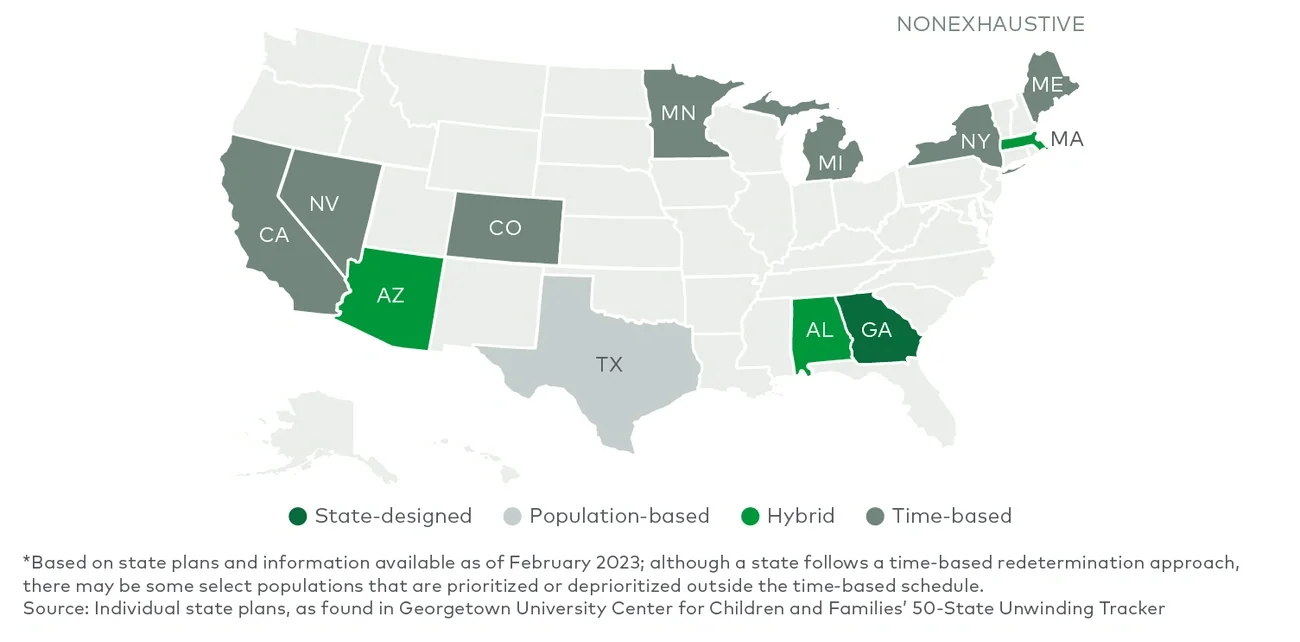

How will the disenrollments be distributed over time?

-

What type of insurance will those who lose their Medicaid coverage receive?

These variables are very difficult to predict, but key indicators such as employment rates, pre-pandemic insurance coverage trends, Affordable Care Act (ACA) policies and state-published plans help shed light on a possible range of outcomes.

The number of people who will lose Medicaid coverage

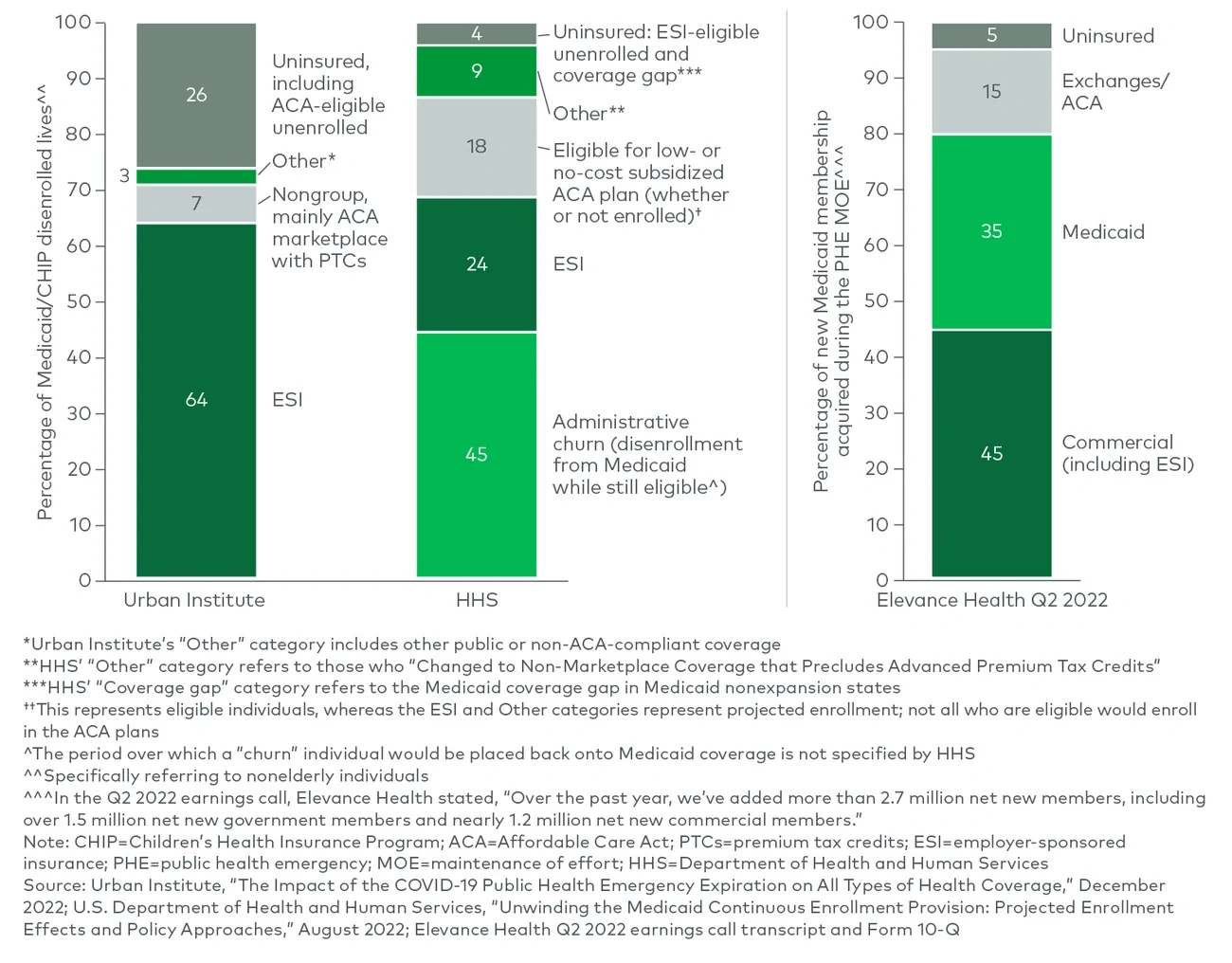

Following the pandemic, unemployment rates have largely stabilized, indicating a return to long-term pre-pandemic trends, and Medicaid enrollment levels are expected to follow suit. A range of key reports, namely from the Urban Institute and HHS, suggest a consensus of around 15 million total Medicaid/CHIP disenrollments due to Medicaid redeterminations, with some caveats (see Figure 1).v vi