-

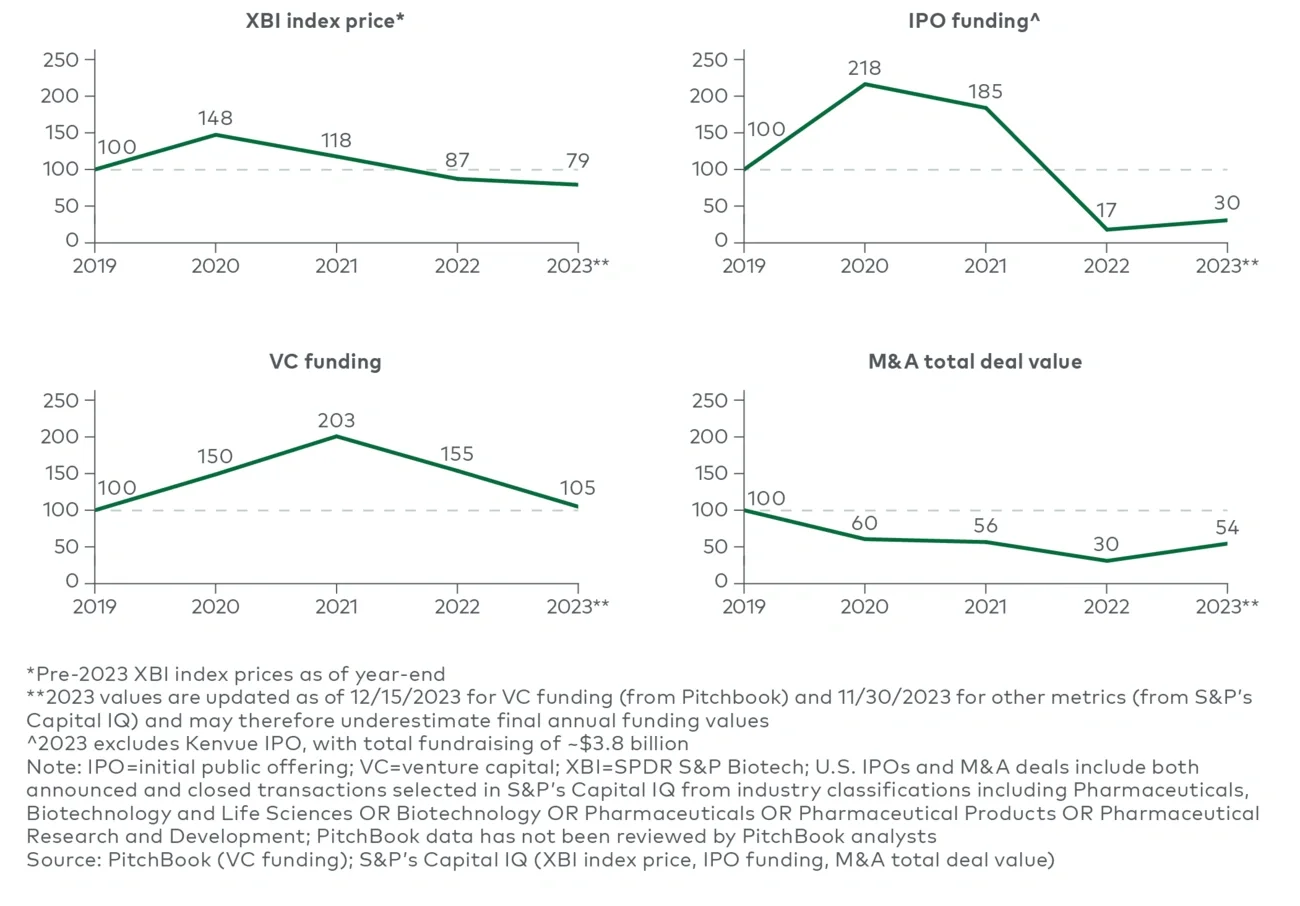

The biotech capital market is starting 2024 in a significant correction period, and it is uncertain how long it will last. Valuations are down significantly: The S&P Biotech index (XBI) is down over 55% since its 2021 peak, while the broader S&P 500 (SPY) gained over 15%.1 History suggests that biopharma can take many years to recover from recession. For example, after a local peak in 2001, the Nasdaq Biotechnology Index fell by approximately 60% over the next four quarters and took nearly 10 years to recover. Biopharma companies should prepare for a sustained recession environment,2 as a near-term recovery is by no means certain.

-

Biotechs with compelling clinical data may still obtain financing, albeit with lower valuations than in 2020-21. Annual venture capital funding has remained strong, and while 2023 is well below pandemic highs, funding has kept above robust pre-pandemic levels.3 Despite this, post-pandemic financing rounds have reportedly4 taken longer to close than in prior years and with greater data expectations.

Private equity firms are also increasingly testing the waters of biotechnology in partnership with venture firms, as recently demonstrated by KKR’s investment in Catalio Capital Management, and represent another source of private funding.5 Volume and value of biotech initial public offerings remained well below pre-pandemic levels throughout 2022 and 2023.6 Investors have higher expectations for clinical data than in prior years, and valuations are still well below pandemic highs.7 Companies unable to access preferred forms of financing may need to find alternative sources (e.g., private investment in public equity financing, debt financing, royalty monetization), although high interest rates make debt financing less attractive. Ultimately, many biotechs may look to the M&A market for their next value inflection point.

-

While conditions are right for smaller-scale biotech acquisitions, fewer viable acquisition targets exist. The top 16 biopharmas had over $500 billion in collective M&A firepower as of November 2023 (based on maintaining a certain net debt-to-EBITDA ratio).8 Many players are keenly interested in dealmaking to offset forthcoming loss of exclusivity and Inflation Reduction Act (IRA) impacts on midterm revenue growth, but there is a limited supply of relevant M&A targets left given the recent wave of acquisitions. Fewer attractive M&A targets exist now than in 2020-21.

-

Biopharma may turn to larger, scale-multiplying M&A to weather the impacts of patent cliffs and the IRA. Many large pharma companies are facing significant revenue gaps in the coming years. The spread in market cap between the largest and smallest top 15 pharma companies is wider than historical norms, making it increasingly difficult for some to compete at scale. These factors could prompt a wave of consolidation in the industry.

Based on these themes, both small and large biopharma companies may need to explore creative financing and M&A strategies this year to unlock the next stage of value creation.

2. Impacts of new drug pricing legislation will continue to unfold

2024 could prove to be another active year for drug pricing legislation as we monitor the impacts of the IRA’s continued rollout, numerous lawsuits from the pharma industry related to the IRA, a presidential election and strong momentum toward pharmacy benefit manager (PBM) reform. Here are the key drug pricing policy and legislation updates to look for in 2024:

-

The publication by Sept. 1st, 2024, of maximum fair prices (MFPs) for the first 10 drugs selected for Medicare drug price negotiations will give the industry more insight into the magnitude of price reductions. While the IRA mandates specific ceilings for MFPs relative to current pricing, no price “floor” is specified, creating potential for even more severe discounting at the discretion of the Centers for Medicare & Medicaid Services (CMS). Stakeholders across the industry will be closely watching for the initial MFP publication in Q3 to understand the degree to which CMS will exercise the option to negotiate greater- than-mandated discounts. Further details on the specific rationale and analyses used by CMS to support MFP price-setting are not slated to be published by CMS until March 2025, but some initial insights on key drivers may be available from the biopharmas themselves before the end of 2024.

-

Ongoing litigation and the presidential election could also shape the future of the IRA’s drug pricing provisions. Several drugmakers and PhRMA have filed lawsuits challenging the constitutionality of the IRA’s Medicare price negotiation provisions. Given the unprecedented nature of the pricing negotiations, there is a significant likelihood that these cases will face multiple levels of judicial review and appeal, including potential review by the Supreme Court. Final judicial resolution before the end of 2024 is unlikely, and near-term injunctions to stop price negotiations are not anticipated since MFP pricing will not take effect until 2026.

Drug pricing and the legislative future of IRA-mandated pricing negotiations are likely to be a significant area of debate during 2024’s presidential election. Legislative amendment to the IRA is unlikely in 2024 while Democrats retain the presidency and the Senate.

Republicans voted unanimously against passage of the IRA in 2022, and if they were to take control of Congress in 2025, they may pursue a repeal of some or all drug price provisions.9 However, Republican presidential nominee front-runner Donald Trump has taken a strong stance on lowering drug prices and supported Medicare price negotiations in his 2016 candidacy, so it remains to be seen whether such a repeal would be passed even with a Republican president.10,11

-

Key PBM legislation in the pipeline pushes for transparency, with bipartisan support. The next major policy priority aimed at reducing drug prices is PBM reform, with strong legislative momentum in 2023 after years of discussion on the topic. The House and Senate have proposed several bills calling for various degrees of transparency around PBM compensation, and restrictions on spread pricing, pass-through rebates and pharmacy clawbacks. The House has already passed their bill, called the “Lower Costs, More Transparency Act,” which may be amended based on the language of the similar bills proposed in the Senate before the Senate votes.

Broadly speaking, we expect the proposed legislation would exert downward pressure on the gross-to-net bubble if spread pricing were to be banned and/or PBM compensation were to be delinked from size of negotiated rebates. Further compensation transparency should also serve to better align PBM incentives with reducing healthcare costs, although transparency terms vary from routine full public disclosure of all drug prices net of rebates and other discounts (in the House’s bill)12 to periodic reporting to plan sponsors and the Department of Health and Human Services only (in the Senate’s Modernizing and Ensuring PBM Accountability Act).13

-

Beyond the U.S., biopharma leaders will need to begin planning for changes on the horizon in the EU as well.14 The EUnetHTA 21 regulation will make EU-wide joint clinical health technology assessments mandatory beginning in 2025 for advanced therapeutics and oncology products and by 2030 for all other drug products. This shift in clinical assessments from national to EU-wide level will present a short-term burden for pharma, requiring additional market access resources. However, the regulation could prove to be a long-term opportunity, as centralization of clinical assessments could mean earlier initiation of pricing and reimbursement negotiation with EU countries.

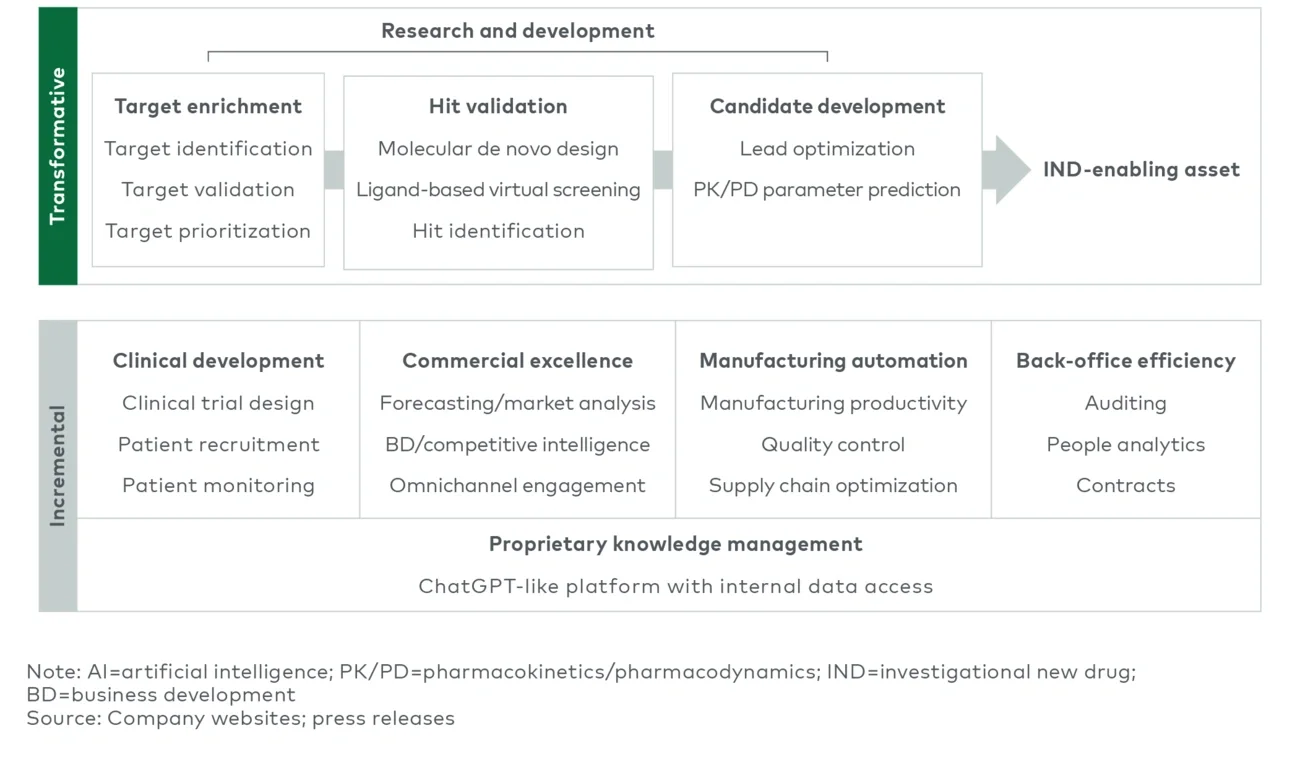

3. Early impact of AI transformation and operational improvements may be realized

2024 should bring both transformational developments and incremental/operational improvements as a result of AI (see Figure 2). Both machine learning (ML)/big data and generative AI, the latest AI computing approach involving the generation of novel content based on training data and context prompting, will be key drivers of efficiency in drug discovery and beyond:

-

The transformative potential of AI-driven drug discovery will be tested in some of the first clinical efficacy readouts. Generative AI and ML will aid in expanding the repertoire of potential drug candidates and accelerate the elimination of less promising ones, hastening progression to clinical trials. In this area specifically, generative AI complements current high- throughput drug discovery’s cycle of deductive and inductive reasoning well and is a natural fit for early adoption. Advances here are particularly important for emerging biotech firms, whose value can hinge on just one or a few early research and development breakthroughs. 2024 will see several clinical readouts from assets whose discovery was heavily influenced by AI, such as InSilico Medicine’s phase 2 data for INS018_055 in idiopathic pulmonary fibrosis15 and Relay Therapeutics’ phase 2 clinical and regulatory update for tumor-agnostic lirafugratinib (RLY-4008).16

-

Beyond drug discovery, biopharmas will be looking for ways to drive incremental improvements through AI, with examples such as improving clinical trial design and participant recruitment, streamlining manufacturing and supply chain processes, simplifying competitive intelligence, and enhancing the development and coordination of sales and marketing materials. Bristol Myers Squibb (BMS) has already applied GPT-4 to clinical trial protocol design, while Takeda has explored applications of AI/ML in patient monitoring.17 Additional operational enhancements and pilot programs in biopharma will likely be announced this year. While evidence of generative AI’s operational impacts in biopharma will be more challenging to discern, efficiency impacts will drive incremental improvements throughout the organization.