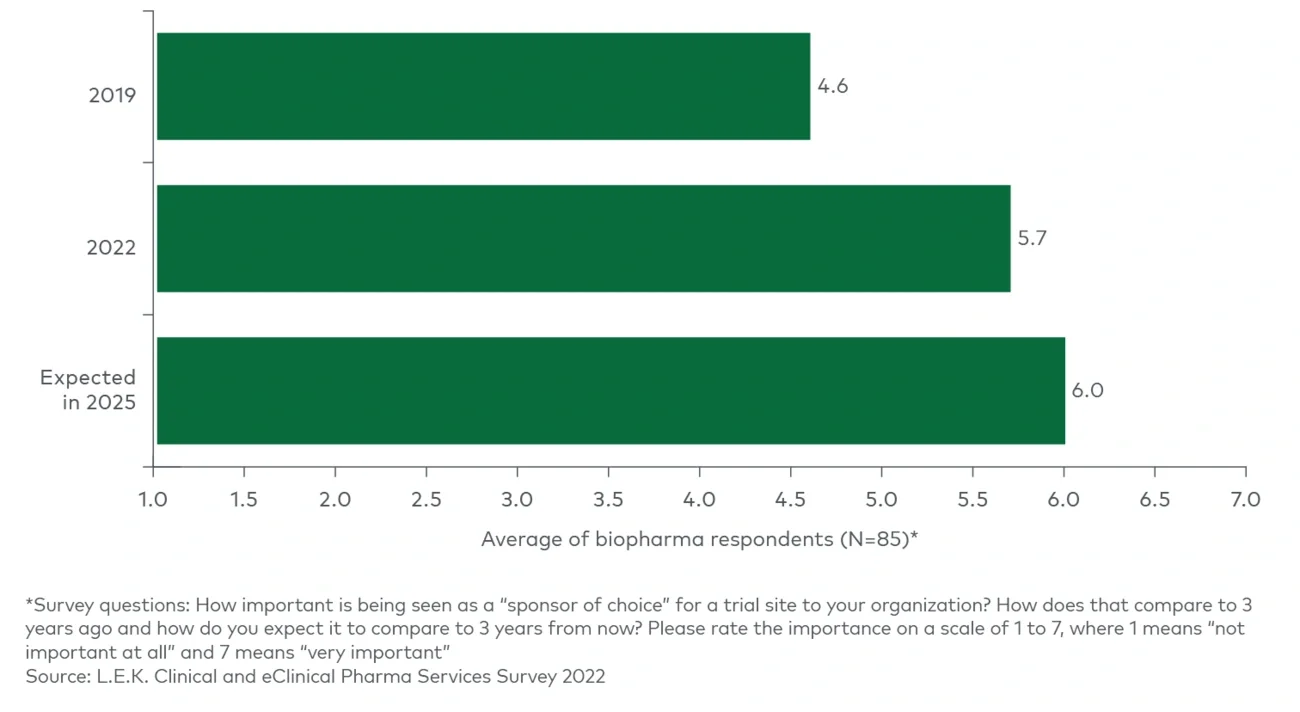

These value propositions are on trend for three key developments we have seen in the clinical trials space.

Increasing complexity of clinical trials

As more advanced-modality assets, such as cell and gene therapies, have entered the clinic and disease focus has shifted to rare disease and oncology indications, trial designs have become increasingly complex. The growing use of biomarkers for patient stratification and eligibility as well as safety and efficacy endpoints, in addition to more complex operational and technical requirements for therapy administration, has created additional hurdles to efficient trial execution.

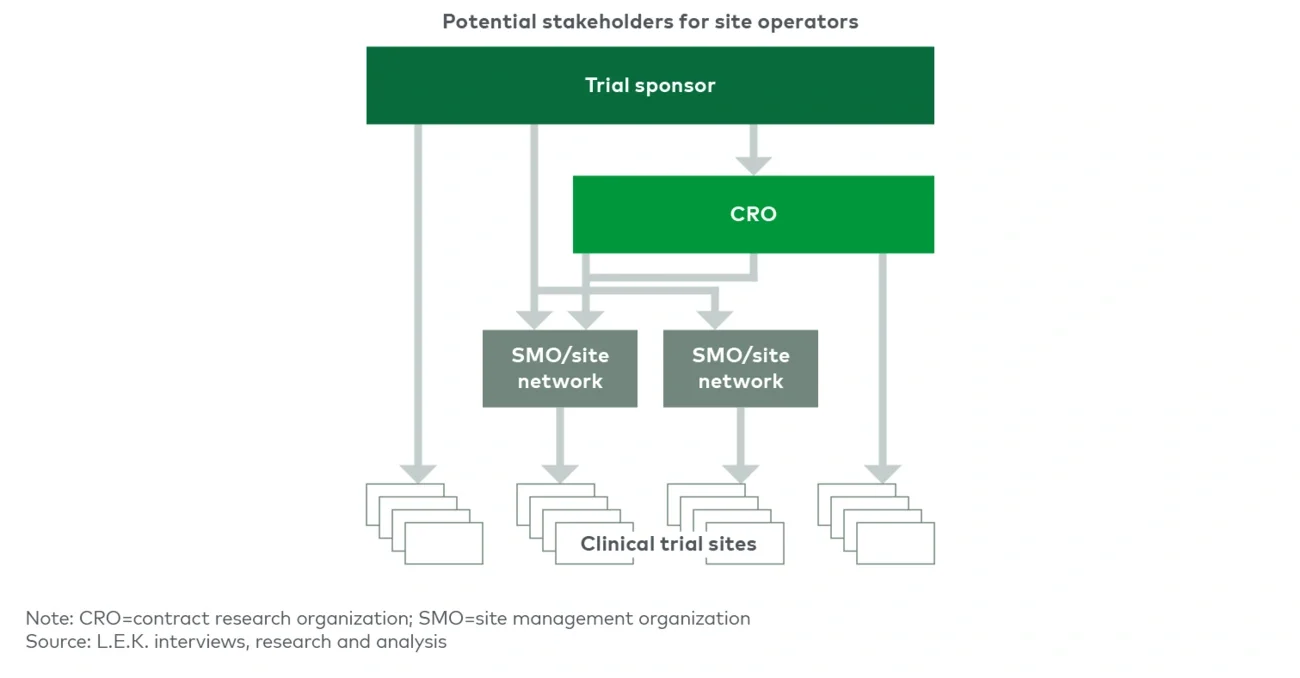

SMO sites are typically fully dedicated to running trials, unlike academic medical centers (AMCs), community hospitals or physician offices that have other patient care priorities. This enables SMOs to dedicate more focused resources and attention to execution of complex trial designs. Furthermore, many SMOs have specific therapeutic area expertise and employ principal investigators who have a track record of executing trials in emerging-modality therapeutics and experience with biomarker data collection and reporting. This focus and expertise, in addition to sponsors’ ability to negotiate a single contract and have a single point of contact across an SMO’s network, reduce the burden of trial complexity on CRO and biopharma clients.

Increasing difficulty with patient recruitment and retention

The rise of personalized medicine has led to a reduction in eligible patients for trials. The shift in pipeline focus toward orphan diseases as well as assets that have additional gating criteria to patient eligibility (e.g., specific tumor markers for targeted therapies in oncology) has created hurdles for patient recruitment, emphasizing the need for recruiting niche populations and including genetically diverse patients.

SMOs have broader recruitment reach than independent sites and can develop best-in-class recruiting capabilities, enabling them to mitigate patient recruitment and retention hurdles. SMOs are also able to build out more robust decentralized trial functions through partnerships and “hub and spoke” models to reduce geographic barriers to patient access.

Increasing cost of clinical trials

In recent years, recruitment delays, bureaucracy at AMCs and trial miscues, in addition to greater complexity of trial design, have resulted in sustained increases in clinical trial costs.2

The SMO model enables economies of scale by distributing back-office costs across multiple trial sites. Furthermore, SMOs tend to invest in capabilities to ensure operational efficiency throughout their network of sites that streamline site management in comparison to sponsor-driven cross-site coordination.

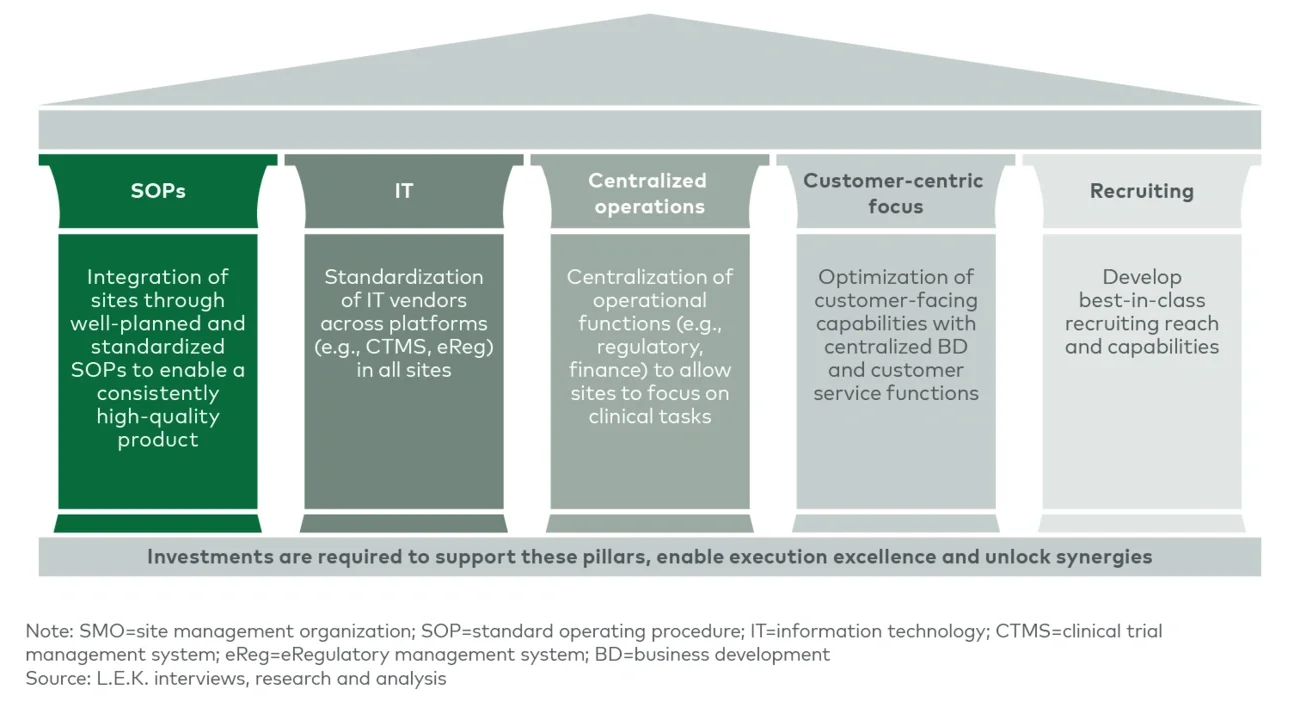

Implications for investors and operators in the SMO space

The trends mentioned in the previous section are expected to continue in the coming years, potentially driving further consolidation of clinical trial sites under SMO umbrellas. However, the rise of SMOs will not be homogenous, and increasing investment in the clinical trial space will result in increased competition among SMOs and their private equity backers. Industry experts indicate that EBITDA multiples for clinical trial sites have risen in recent years,3 and some SMOs have seen mixed results with expansion, sometimes closing sites shortly after startup or acquisition, as Headlands Research did in Houston and in Lake Charles, Louisiana.4 Winning in this competitive environment requires investors and operators to focus on high-value aspects of strategic execution.

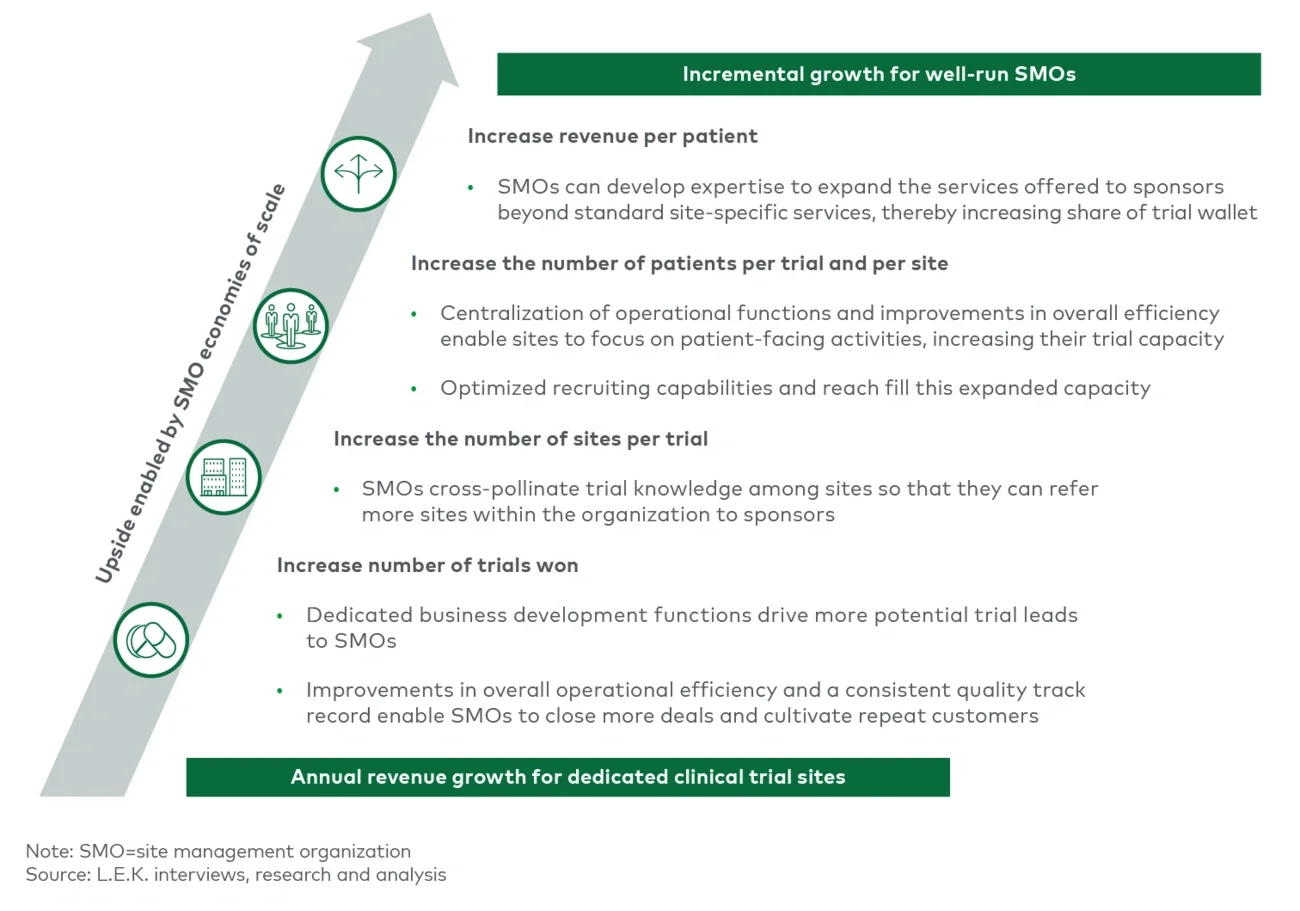

The key to successfully capitalizing on the core SMO value proposition lies in economies of scale. As an SMO expands to acquire or open additional sites and enter into partnerships with AMCs and hospitals, careful consideration must be given to the synergies and capabilities that a new site can bring to the table. Trade-offs exist between adding a novel capability or specialty and adding a site that has similarities to existing sites in order to expand patient access and expertise in a given therapeutic area. The strategy for adding new sites must seek to maximize value along key growth vectors; these include increasing the number of trials won, increasing the number of sites serving a trial, increasing the number of patients per site and growing revenue per patient by capturing additional share of the trial wallet (see Figure 4).