Research and development (R&D) costs incurred by biopharmaceutical companies to bring new therapies to market are extraordinarily high. The median pivotal trial cost per new molecular entity (NME) approved by the U.S. Food and Drug Administration (FDA) between 2015 and 2017 has been estimated at $48 million, and the median cost per patient per pivotal trial for those NMEs has been estimated at over $40,000, according to a recent analysis.1 In the midst of this, patients and the sites that recruit and enroll these patients are changing how trials are executed.

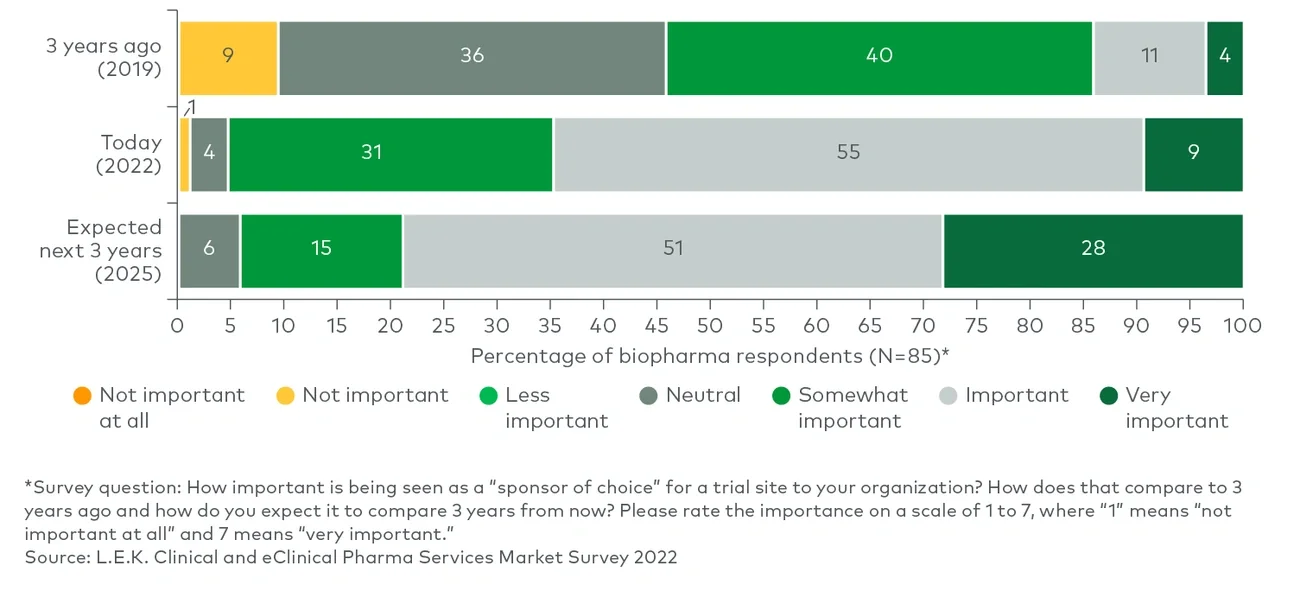

Clinical trial sponsors, as noted in L.E.K. Consulting’s Executive Insights “Looking Ahead in Pharma Services: Key Trends Impacting the Industry,” often fail to reach their recruitment targets. There is also a lack of appropriate racial representation among study participants. On the other hand, while trial sites still play a critical role in the determination of trial outcomes, more activities today are taking place in distributed locations than they did before the onset of the COVID-19 pandemic. Together, these dynamics have led to a greater reliance on clinical trial partnerships for execution.

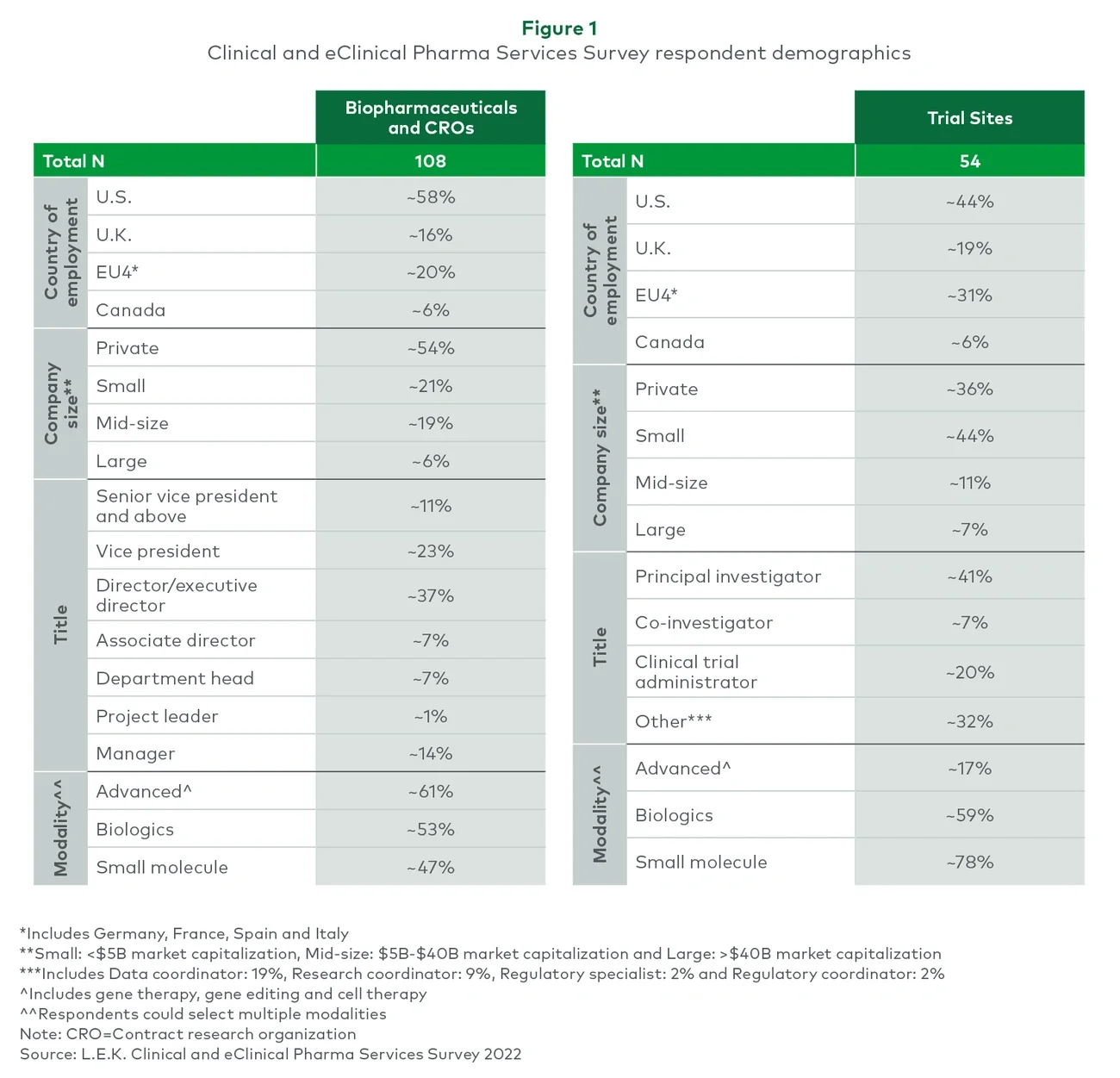

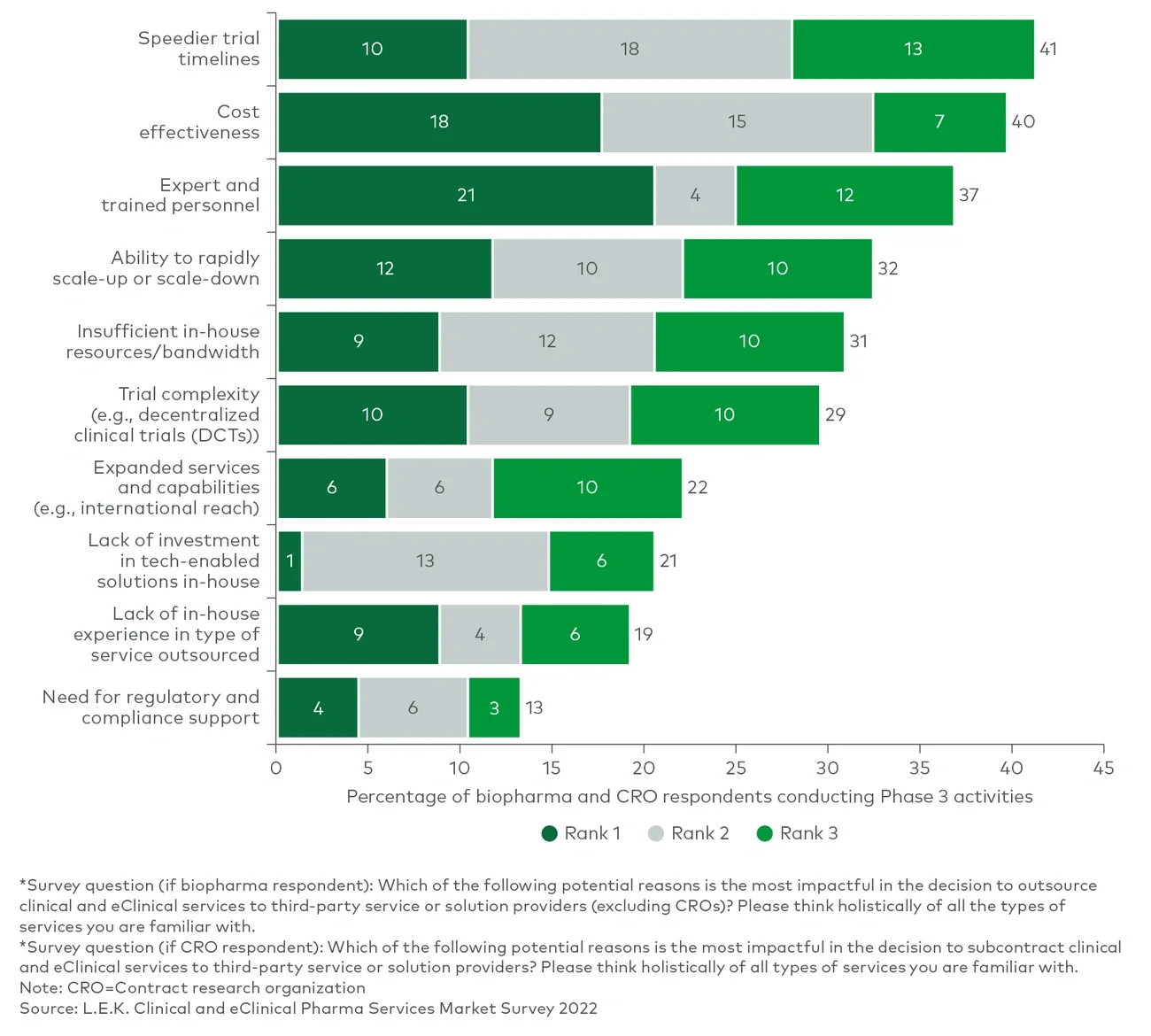

In its inaugural Clinical and eClinical Pharma Services Survey (see Figure 1), L.E.K. asked biopharmaceutical, contract research organization (CRO) and trial site experts about these and other key emerging trends in clinical trials and how they are impacting the outsourced, clinical and eClinical pharmaceutical services market. This report also makes clear how sites and patients are changing the way trials are executed and how those changes are driving growth in the market.