The barriers to success in the vaccine space, particularly within infectious diseases, stem from the challenges of vaccinating a large, healthy and global population. Regulators such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) are reluctant to approve a vaccine in the absence of a clear and convincing risk-benefit ratio. Obtaining this data is difficult, as rare side effects may only be observed after inoculating many patients.

Vaccine developers need to design trials with large, diverse sample sizes to ensure all possible rare adverse events and comorbidities are captured. These trials can be lengthy and costly, impacting both development timelines and return on investment. In addition, in the case of seasonal vaccines, there are often annual regulatory requirements that create additional development and regulatory costs as well as operational burdens for vaccine companies.

Policymakers such as the Centers for Disease Control and Prevention’s (CDC) Advisory Committee on Immunization Practices (ACIP) in the U.S., the National Advisory Committee on Immunization (NACI) in Canada, the Joint Committee on Vaccination and Immunisation (JCVI) in the U.K., the Technical Committee on Vaccinations (CTV) in France, and other advisory boards assess not only safety and efficacy in making their recommendations but also cost-effectiveness. A positive recommendation from these organizations is a prerequisite for high uptake.

Other market stakeholders that influence uptake include governments, physicians, pharmacies, distributors and patients. The level of influence of these diverse market stakeholders on vaccine uptake, pricing and access may differ by market or geography. In many high-income countries, retail pharmacies have gained increasing influence, creating additional pricing pressure and another layer of stakeholders for vaccine manufacturers to navigate.

The high-volume development, global commercialization, and associated tight and unpredictable operational timelines (e.g., seasonality, guidance windows, regional complexities) illustrate that developers must have access to both flexible manufacturing at scale and regional distribution networks.

Regulator preferences on strain selection and number of strains (e.g., monovalent vs. bivalent) included in a vaccine also can stress various parts of a biopharma company. R&D and commercial teams must be able to predict and develop updated versions of vaccines on a regular basis, while manufacturing capacity may need to be left idle when off peak. A diversified manufacturing and supply network, while not easy to come by, provides the flexibility needed to update, scale and distribute to the different stakeholders across markets in a timely manner.

In a competitive marketplace, new entrants may have a harder time creating necessary manufacturing and supply networks, resulting in likely tech transfer challenges as well as development and distribution delays. Additionally, keen oversight of the supply and manufacturing network, no matter how large or small it may be, is paramount. As was clearly illustrated during the COVID-19 pandemic, millions of vaccine doses had to be discarded due to a manufacturing error that led to the contamination of two vaccines being made in the same contract development and manufacturing plant.

Governments and other payers may be unwilling to pay high prices for a widely distributed vaccine even if it is cost-effective. For example, in the U.S., the average noninfluenza vaccine costs approximately $110 per dose in the private sector. Most influenza vaccines are priced quite a bit lower, in the $20-$60 range. Even the most expensive vaccines, such as Gardasil, Prevnar and Bexsero, are priced at a few hundred dollars per dose. These prices are far lower than the cost of most novel branded prescription therapeutics.

Additionally, unlike with treatments for chronic diseases, patients may only receive a vaccine course once (e.g., a pediatric hep B vaccination requires three doses over six to 18 months), seasonally (e.g., for influenza) or even less frequently (e.g., a Td or Tdap vaccination every 10 years), which can further limit recurring revenue. To that end, many COVID-19 vaccine manufacturers have signaled that they will increase prices from about $20 per dose to $110-$130 per dose as they transition to the commercial market.

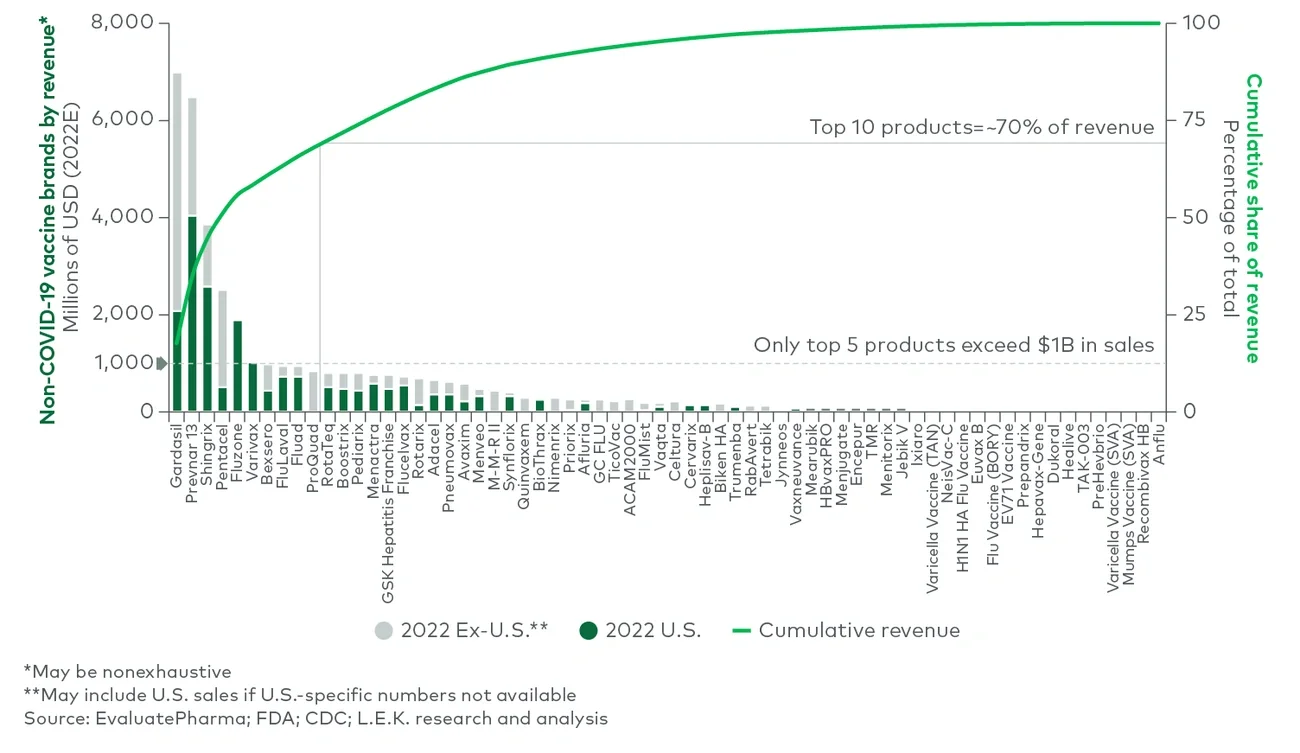

These pricing pressures are a major reason why only five non-COVID-19 vaccine brands exceeded $1 billion in estimated worldwide sales in 2022, accounting for approximately 55% of the market (see Figure 3). Parallel to lower revenues, lower pricing also reduces profit margins. This is especially critical for small and emerging biotechnology companies that may not be able to benefit from economies of scale.