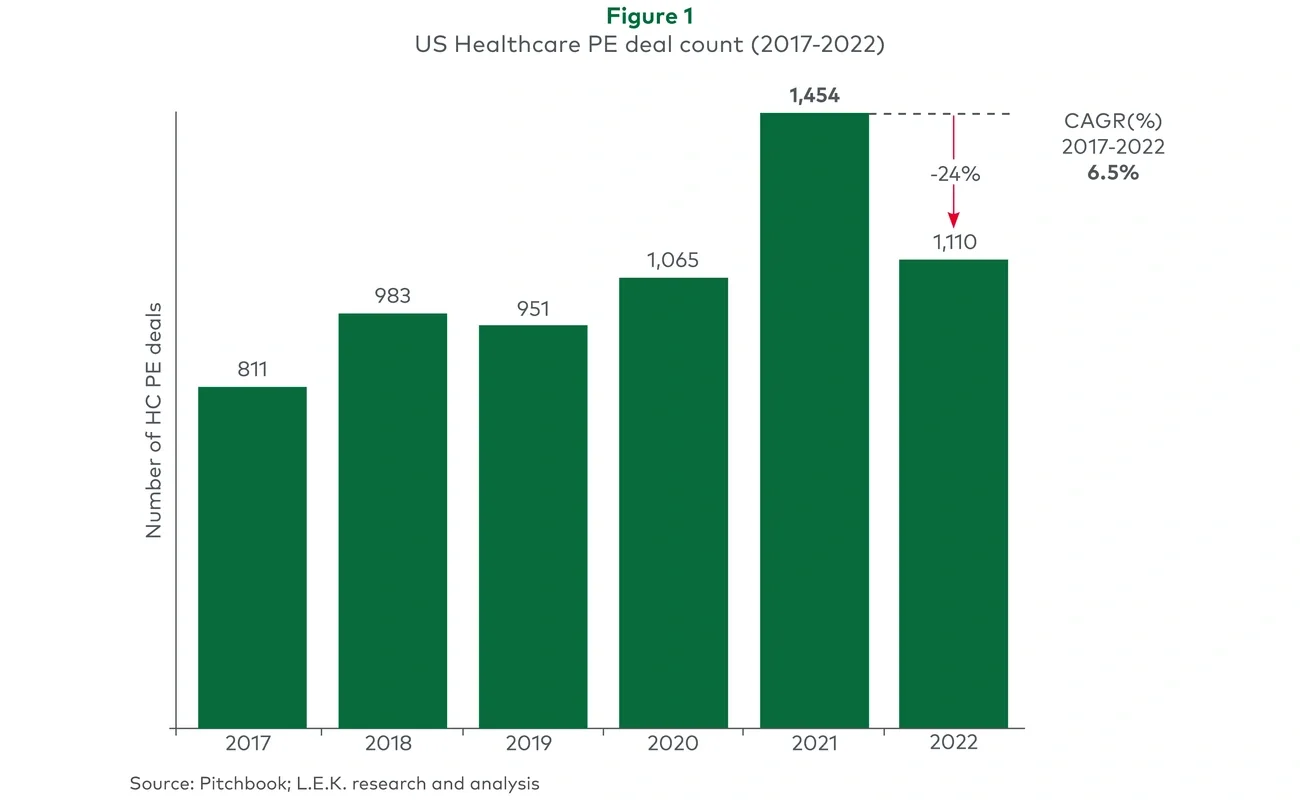

Despite an overall market decline, L.E.K.’s North American Healthcare PE activity increased approximately 20% year over year off our best year ever in 2021 as our larger, more tenured team dug in for PE clients across the healthcare value chain.

Healthcare providers

Med spas

The number of med spas in the U.S. has doubled from roughly 4,200 in 2017 to approximately 8,900 locations in 2023 and now represent approximately $16 billion of annual spend. While only a handful of scaled platforms exist to date, private equity firms recognize market growth as well as potential for professionalized branding, membership sales, de novo site launches, and tuck-in M&A. There are robust underlying growth drivers and strong long-term prospects in this area, including affluent clientele, the recurring nature of treatment, and customer feedback regarding the importance of treatment. This applies even if a recession creates temporary setbacks.

Orthopedics/Musculoskeletal (MSK) care

The U.S. orthopedic/MSK market, which includes professional fees and outpatient facility fees, represents approximately $75 billion in spend and is expected to grow at 6.8% annually to reach approximately $110 billion in 2027. Orthopedists are increasingly dissatisfied with hospital employment and interested in joining scaled independent practices. These groups often allow orthopedists to retain clinical autonomy while providing scale, strong leadership and strategic direction, and superior compensation and equity.

Dental services

While private equity firms have been investing in dental service organizations (DSOs) for some time, standard DSOs, specialty DSOs (e.g., oral surgery, orthodontia), and dental labs remain fragmented and present significant runway for both de novo growth and M&A. Today, approximately 23% of all U.S. dental offices are DSO-affiliated. As DSOs continue to outgrow their competition on a same-store sales basis and also through M&A, they are expected to exceed 15% yearly growth through 2026. Specialty-DSOs are expected to grow even faster.

Rural health/urgent care

Rural-focused providers of urgent care, primary care, and other specialties (e.g., behavioral health, orthopedics) are an often overlooked but critical and growing front door for healthcare for many Americans. While healthcare provider capacity is limited throughout the U.S., it is more than 50% lower in rural markets than in urban areas, resulting in an “If you build it, they will come” supply/demand dynamic. Millions of Americans sought diagnosis and/or treatment for COVID-19 in a rural health location and respond that they are very likely to go to that location for future medical care including downstream care (if possible), which is likely to equate to well above-national-average growth rates for providers who can attract and retain talent.

HCIT

Practice management/EMR solutions

Private equity firms continue to invest in practice management software solutions, which support appointment scheduling and tracking, compliance reporting, visit documentation (e.g., electronic health records), insurance claim reporting (e.g., revenue cycle management) and database management, as well as more recently emerging functions (e.g., patient intake, e-prescribing, and marketing) across a variety of specialties. Practice management software is anticipated to remain an active area of investment for private equity firms given solution stickiness, the emerging focus on specialty-specific offerings, horizontal and vertical provider consolidation, growing market complexity and costs, and increased regulatory pressure that all lend themselves to greater solution adoption and willingness to adopt add-on modules and services.

Human capital management software (HCM)

Human capital management software solutions continue to be active areas of investment for private equity firms as healthcare providers look for ways to automate workflows (including support for HR, staff deployment and regulatory compliance). Private equity interest in this space is expected to continue due to the increasing use of cloud-based solutions and an increasing need for integrated HR suites, as well as the emerging adoption of workforce analytics solutions and digital technologies.

Tech-enabled services

Value-based care (VBC) enablers

Value-based care is gaining traction as capitated platforms in primary care expand rapidly and new specialties follow suit (e.g., kidney-care, MSK). Provider groups that have historically operated under fee-for-service (FFS) are increasingly making the transition to VBC and seeking vended support to fill gaps in population health management (PHM)/care management (CM) experience, capabilities and tools. While the market is relatively nascent and there is room for many winners across different models, the vendors most likely to succeed will bring a proven track record of cost savings and improved clinical outcomes, a broad suite of PHM and CM offerings, robust data & analytics capabilities, strong integration capabilities, and VBC contracting expertise.

Specialized revenue cycle management (RCM) solutions

As in practice management/EMR solutions, specialist providers and investors are realizing the need for specialized RCM solutions. Increasing healthcare spend, provider cost pressures, the transition to VBC (in some specialties) and increasing complexity in claims/billing are driving increased adoption of best-in-breed RCM solutions. Investors are especially interested in providers with deep expertise in highly complex claim specialties such as anesthesiology, orthopedic, or third-party claims.

Healthcare staffing

Private equity firms continue to invest in healthcare staffing providers which include travel nurses, per diem nurses, locum tenens, and allied healthcare staff serving a variety of healthcare providers (e.g., hospitals, ambulatory surgical centers, specialty physician practices, clinics, home health agencies, veterinary clinics). Investment activity in this space is anticipated to grow as an increasing geriatric population requires significant medical care, technological advances require skilled labor, and healthcare staff suffer from the lingering impact of COVID-19 burnout — all of which drive up bill rates and indicate a continued supply and demand imbalance for years to come.

Home-based care

The U.S. home healthcare market size was valued at approximately $140 billion in 2022 and is expected to grow approximately 7.5% annually through 2030 driven by a growing geriatric population, the rising desire to age in the home and increasing prevalence of chronic diseases. Recent advancements in technology and cost effectiveness of home healthcare services are driving healthcare providers to implement hospital-at-home and skilled-nursing-facility (SNF)-at-home programs, as well as to explore a variety of solutions (e.g., remote patient monitoring, electronic caregiver visit verification, care coordination) that push the boundaries of care that can be cost-effectively provided where patients want it most — in the home.

Employer cost-containment solutions

Self-insured employers and third-party administrators (TPAs) are increasingly deploying cost containment solutions to combat rising claims costs, fraud, complex coding requirements, and prompt-to-pay laws. Payers have many solutions at their disposal to help contain costs, ranging from payment integrity solutions to network access, care management and reinsurance/stop-loss solutions. Outsourced out-of-network (OON) repricing solutions are one subsegment that is expected to grow 11%-13% each year to reach $1.3-$1.4 billion of spend through 2024.

For more information, please contact healthcare@lekinsights.com.