In vitro fertilization (IVF) in Asia-Pacific (APAC) and the Middle East is on a high-growth trajectory driven by rising demand and supply innovations. This Executive Insight, co- authored by L.E.K. Consulting and Lincoln International, discusses five reasons why the APAC and Middle East regions present a compelling investment opportunity for various investors interested in the IVF sector:

-

Growing IVF cycle volume: IVF cycle volume in APAC and the Middle East reached 1.5 million in 2021 at a five-year CAGR of 8%. Countries such as India, Thailand, and China demonstrate potential for high growth while moving up to developed market penetration levels.

-

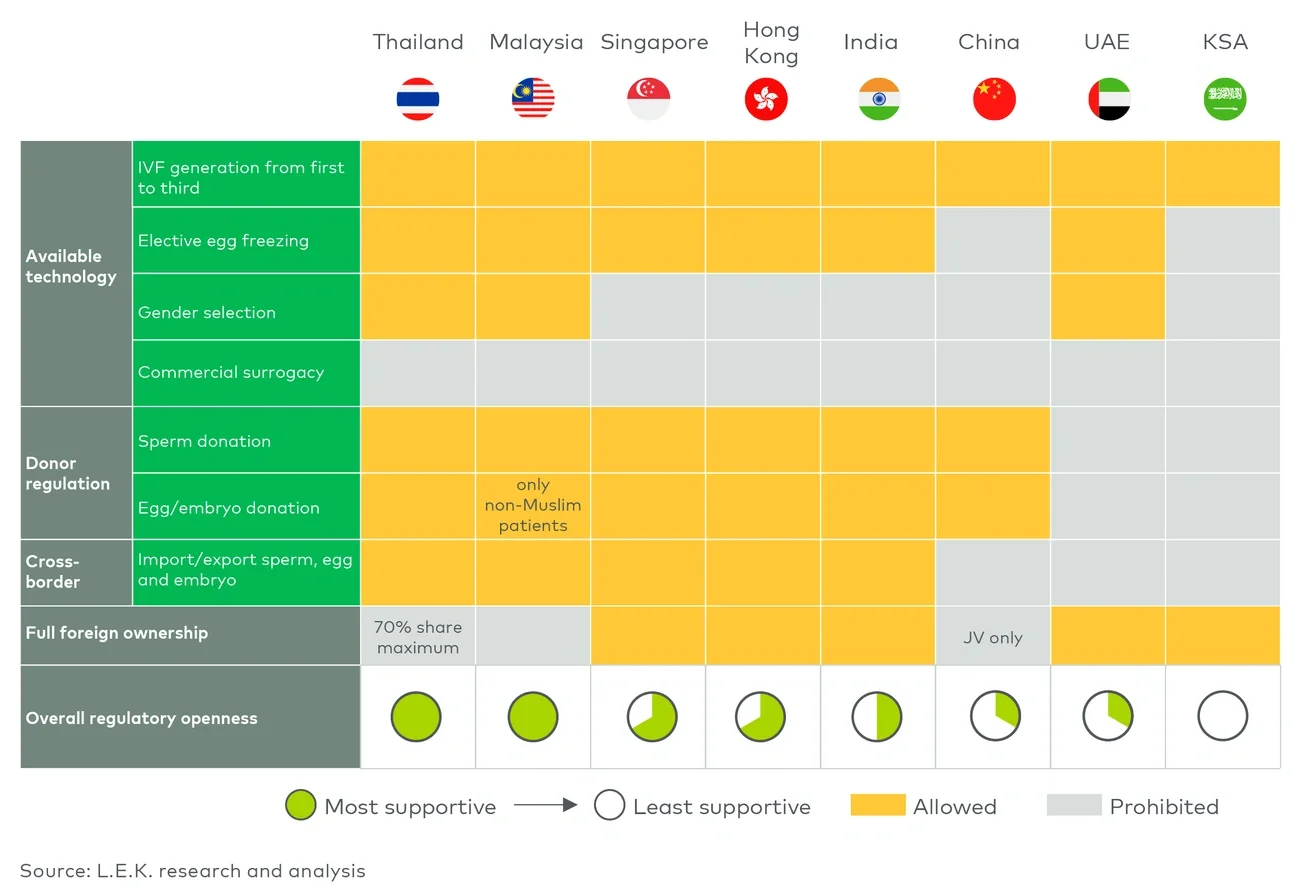

Enhanced regulatory frameworks: Clearly defined regulations are foundational for establishing a scaled and corporatized IVF market. While Thailand and Malaysia have the most flexible regulatory environments, recently introduced regulations may impose some restrictions in key countries such as India. However, the formalization of regulations will be a positive influence for the sector in the long run, as it will drive quality and compliance.

-

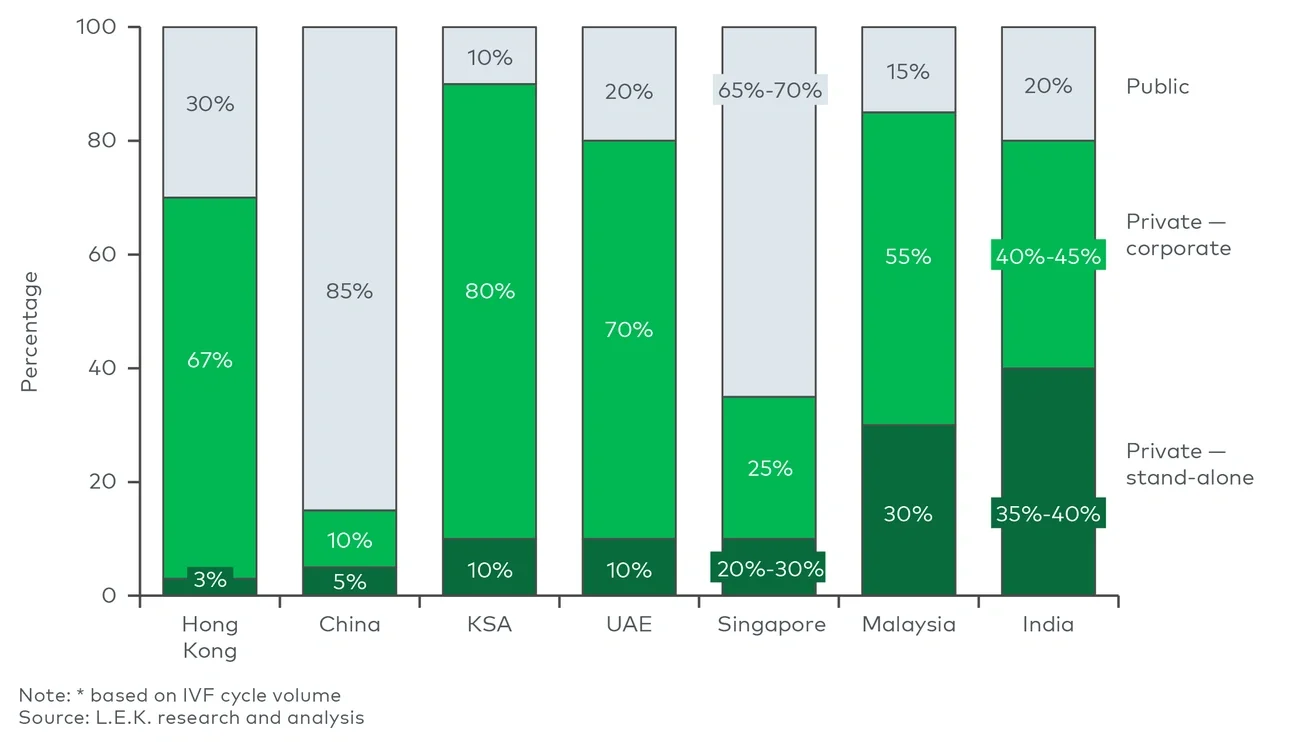

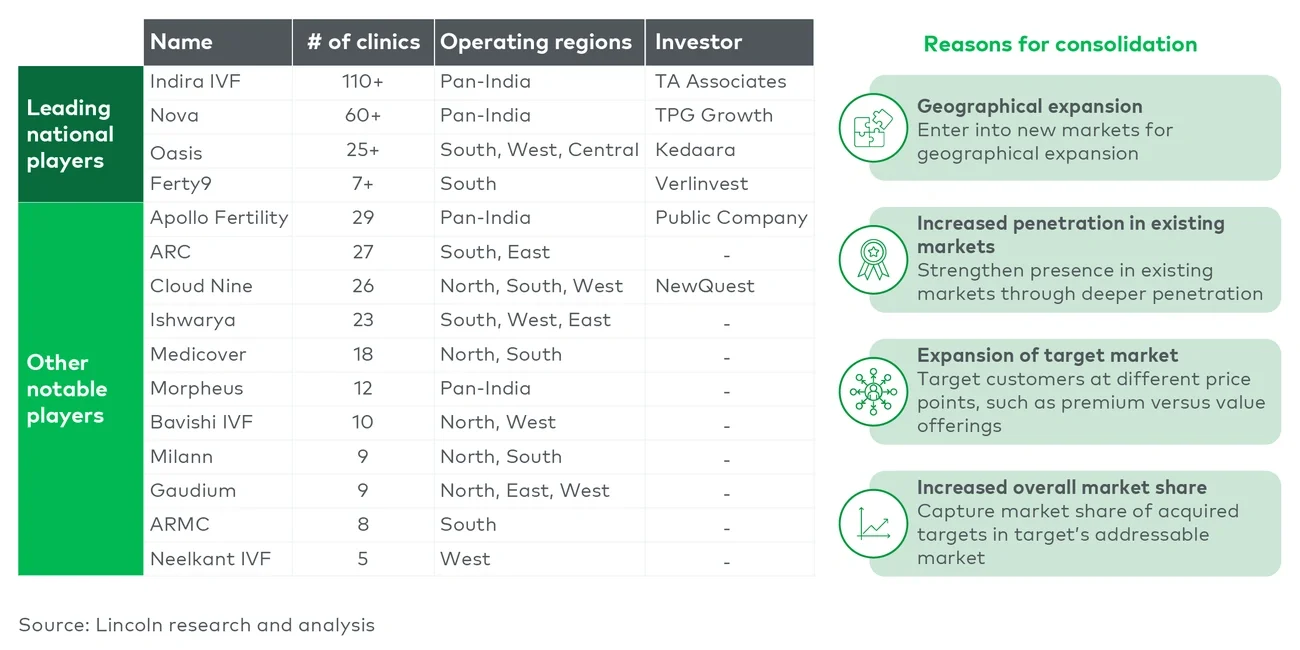

Market consolidation: Opportunities remain for scaled play and consolidation in the regions as more providers are emerging with rising market share due to increasing formalization. Fragmented markets such as India and China are expected to consolidate, driven by the expanding presence of corporate providers due to favorable regulations as well as better access to capital.

-

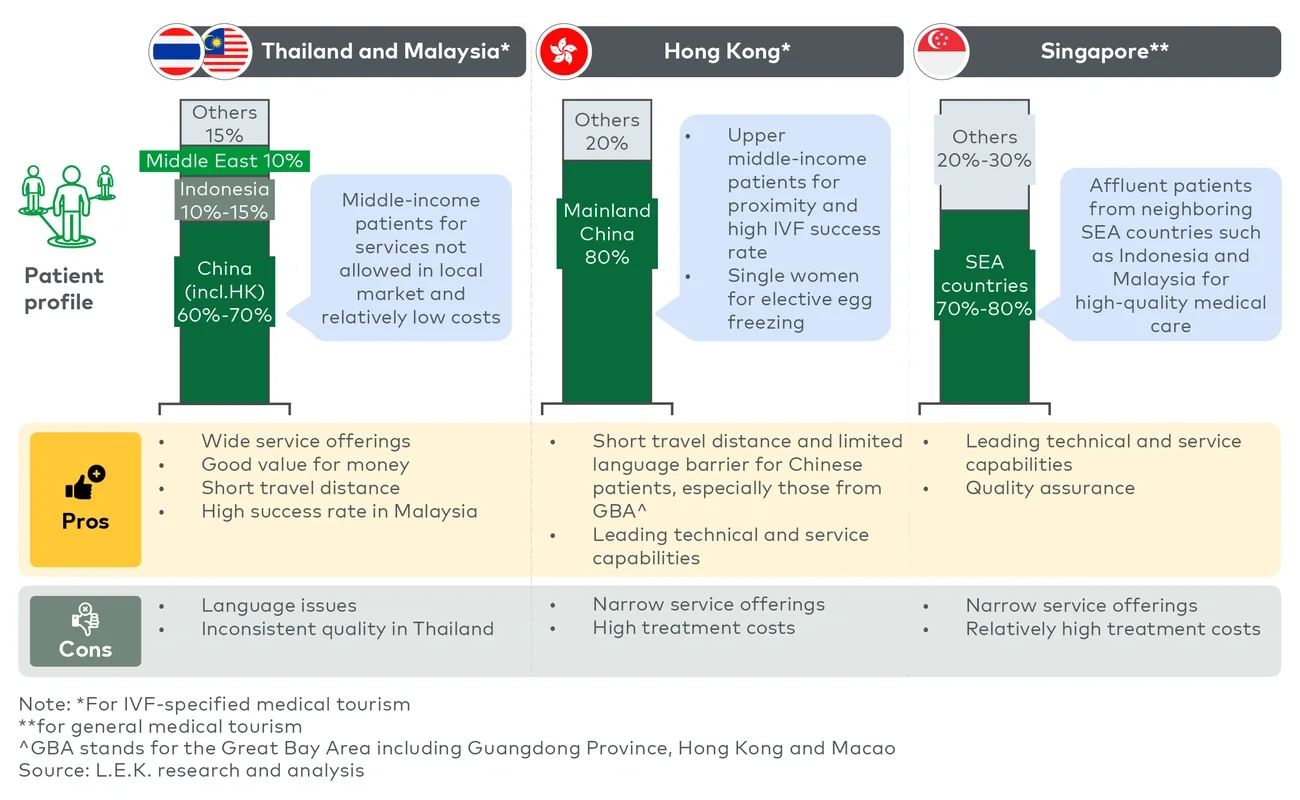

Potential of medical tourism and regulatory arbitrage: Demand from medical tourism is rebounding post-COVID-19. Given regional differences in regulations, regulatory arbitrage acts as a growth driver for IVF. Cautious planning is essential, though, considering that changes in the regulations can be unpredictable.

-

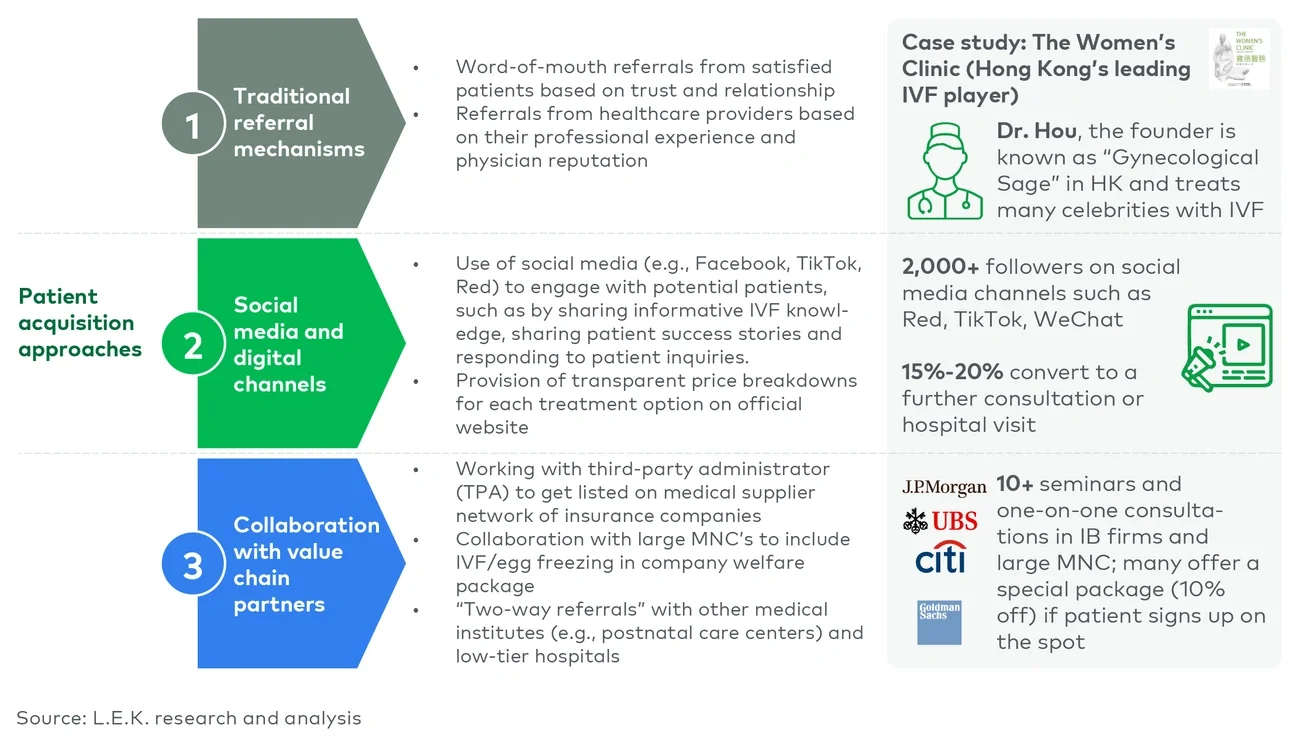

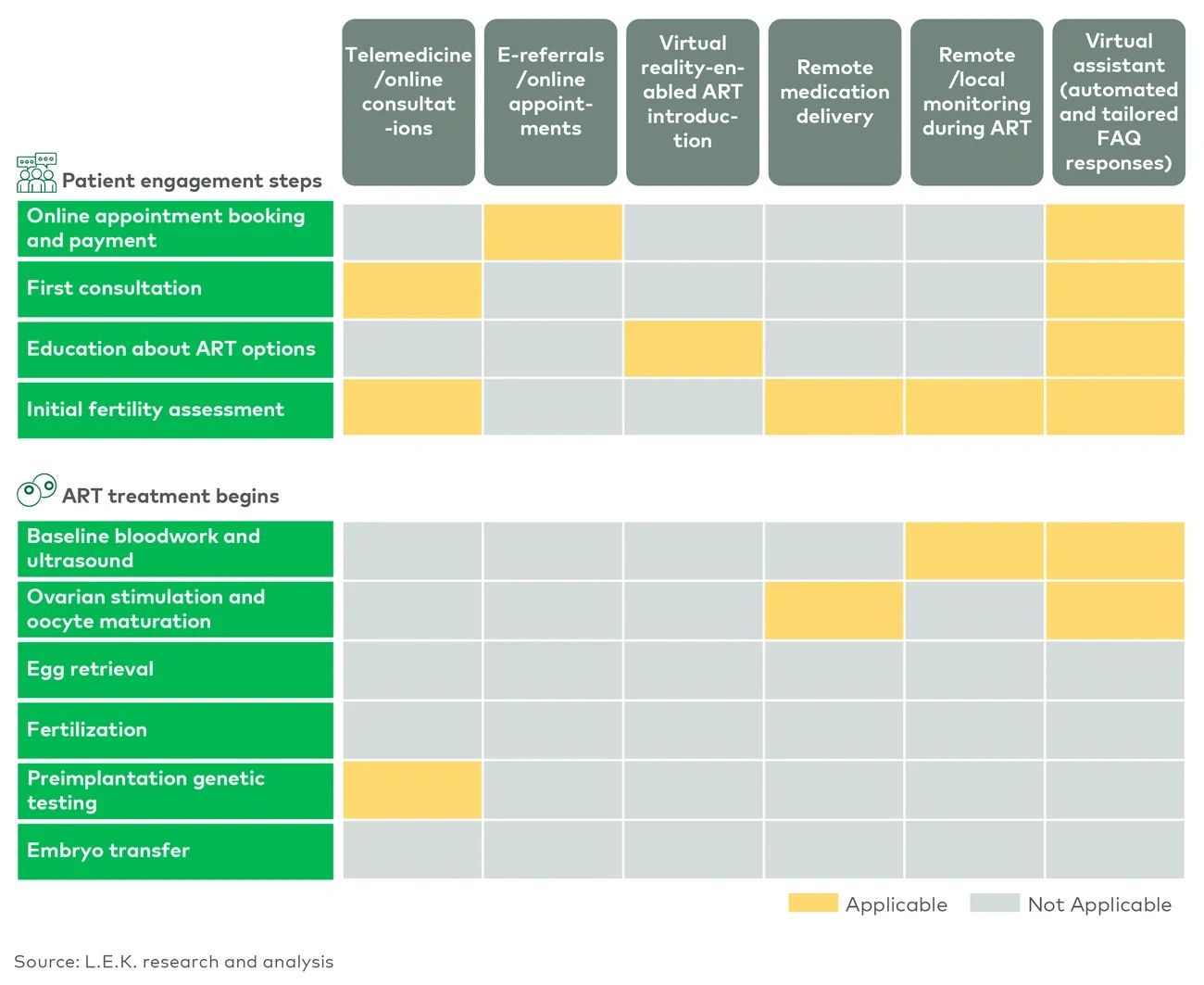

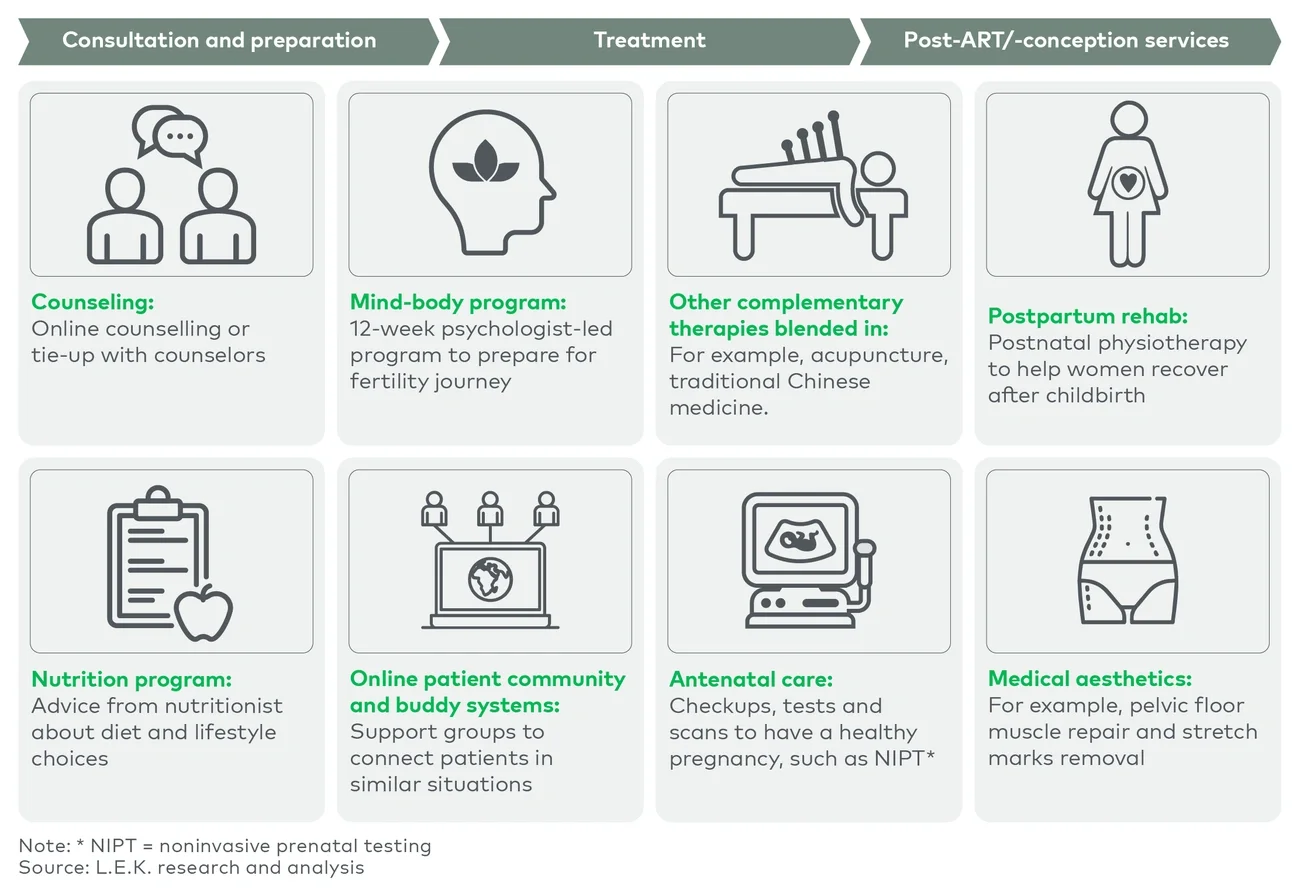

Innovating to grow: From an operational perspective, adopting technology and standardization can help IVF clinics reduce their reliance on star physicians and embryologists while improving success rates.

The favorable characteristics of the IVF market present an attractive opportunity for a variety of investors:

-

Private equity: We observe strong interest from private equity (PE) investors in the APAC and Middle East IVF market, which is characterized by the emergence of national leaders with scalable business models and favorable economics. PE investors can add value to such businesses through operational improvements and aiding their expansion into international markets.

-

Domestic providers: IVF providers can expand their footprint in local and international markets, leveraging their expertise, growing demand and regulatory framework enhancements. Market consolidation is expected to be driven by leading corporate providers.

-

International providers: The APAC and Middle East regions demonstrate stronger growth momentum and potential than developed markets. International providers can leverage best practices in developed regions and technology to explore expansion opportunities if they can customize their value proposition to meet local market needs and ensure that their services are affordable in emerging markets.

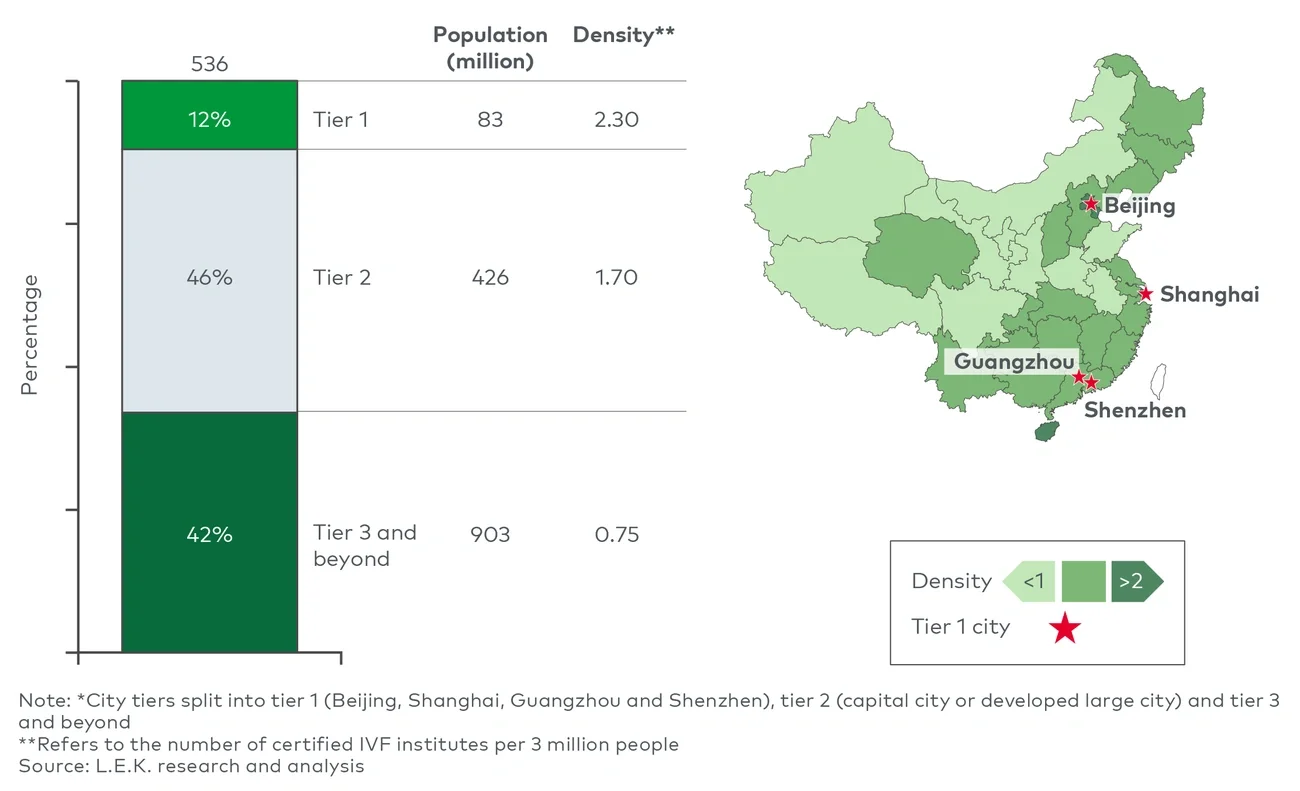

Malaysia stands out with strong IVF cycle volume growth of about 10% per year compared to the regional average of approximately 7% per year (2021-25F). Favorable medical tourism policies, wide service availability, reasonable costs and proximity to key markets are essential drivers. China is expected to remain the largest IVF market in the region, considering its large population base and rising infertility rate. Outbound medical tourism demand from mainland China will remain stable in the near future. India’s IVF market is expected to observe positive change driven by regulatory framework enhancements, while consolidation by leading corporate players will offer exit opportunities to current investors and owners. Overall cycle volumes will see continued growth at about 8% per year (2021- 25F), though donor cycle contributions will reduce in the near term. Singapore, Hong Kong and the Middle East are more mature markets. Without main regulatory changes, these countries are expected to remain key destinations for affluent medical tourists from nearby countries seeking quality treatment.

Growing IVF cycle volume

IVF cycle volume in APAC and the Middle East reached 1.5 million in 2021 at a five-year CAGR of 8%. Pertinent growth factors are as follows.

Accelerating macroeconomic growth

IVF treatment growth demonstrates a strong correlation with the macroeconomic development stage (see Figure 1).