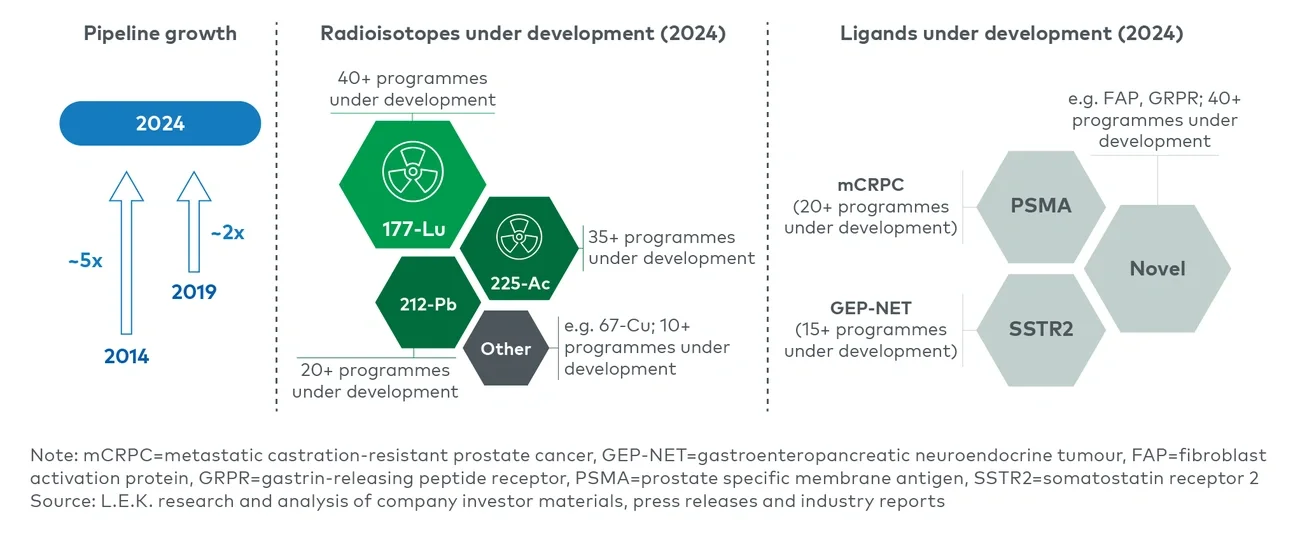

For beta-therapies, 177-Lu sees large late-stage activity, partially driven by the development of generic alternatives to Lutathera; multiple entrants submitted applications for approval in H1 2024. Copper-67 (67-Cu) provides a lesser-proven alternative isotope that mostly sees activity in early-stage Phase I/II development combined with de-risked ligands trialled with 177-Lu assets (e.g. PSMA, SSTR).

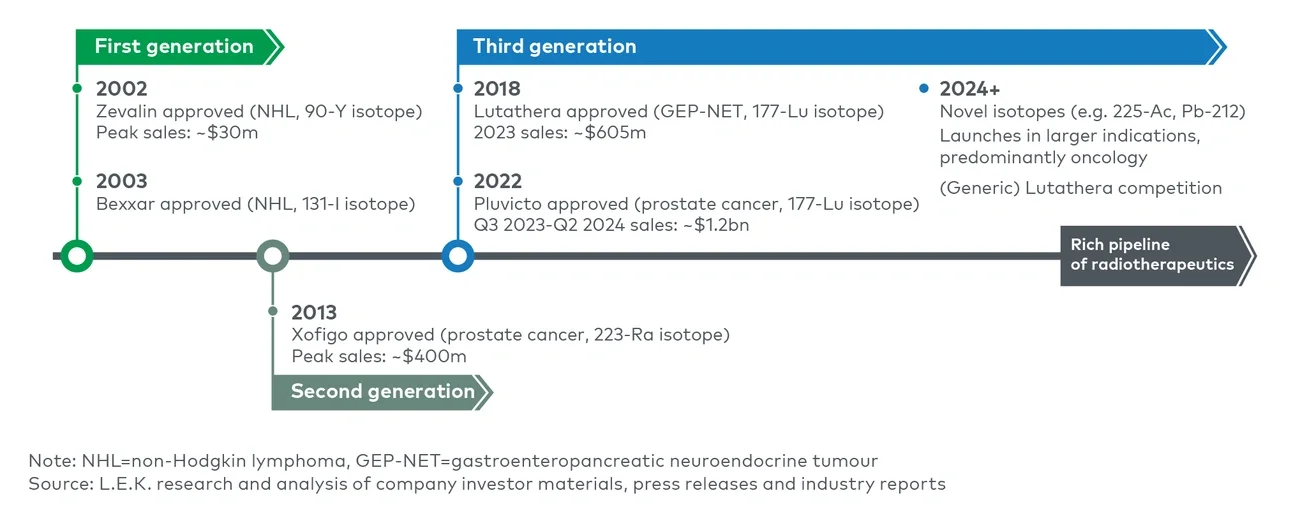

For alpha therapies, discussion around the optimal isotope is continuing. Despite Xofigo’s first 223-Ra launch, research activity had gravitated towards 225-Ac with pipeline assets positioned as the next wave behind 177-Lu. Interest is driven by its roughly 10-day half-life and relatively manageable ability to be linked to targeting moieties. 212-Pb is, however, increasing in popularity among investigators, where a substantially shorter half-life of around 10 hours opens the possibility for optimising a dosing schedule through administration of a lower number of larger doses (fractionation) as well as balancing of adverse exposure to healthy tissue while achieving a therapeutic effect.

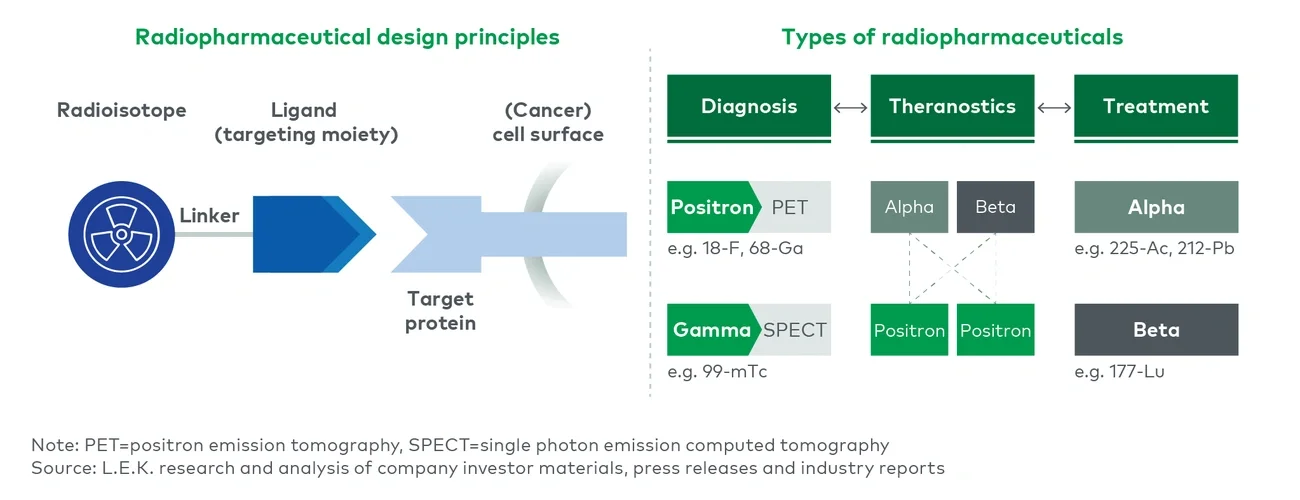

The industry is expanding its interest beyond PSMA and SSTR targeting ligands with the emergence of novel targets for other predominantly oncology indications. In particular, FAP (fibroblast activation protein) has seen early-stage development activity due to its theranostic potential across tumour types.

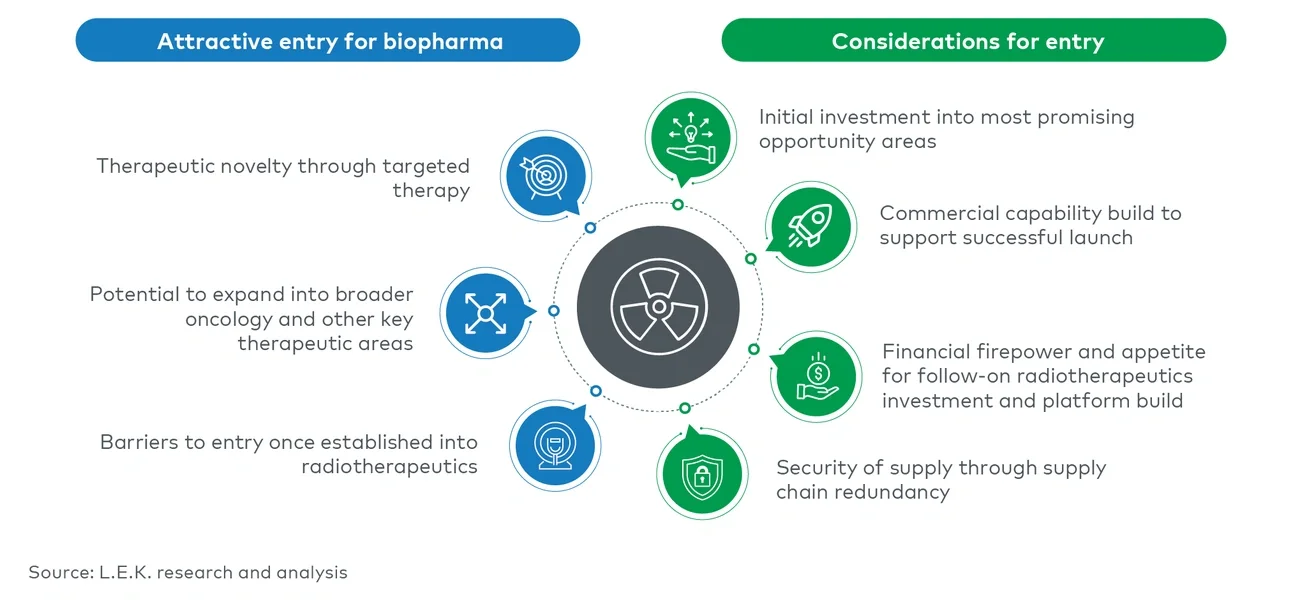

Key considerations for biopharma assessing potential entry into radiotherapeutics

As the radiopharmaceuticals sector is experiencing unprecedented interest, biopharma will need to consider key elements to succeed (see Figure 4). Initial investment in the right innovation areas – by isotope, ligand, therapeutic indication – should be carefully assessed, in addition to follow-on investment to build a broader radiotherapeutics platform. To support a successful launch, consideration must be given to commercial capability build-out, as well as decision-making regarding whether to in-house or outsource manufacturing, which itself can be quite complex. Notably, the shorter half-life of some of these radioisotopes (i.e. those that are measured in hours) will require different manufacturing and supply chain infrastructure that could significantly impact operations and financials.

M&A offers biopharma an accelerated path into radiotherapeutics and has been a preferred route in recent years for big pharma. Novartis, AstraZeneca, Bristol Myers Squibb and Eli Lilly were responsible for four of six key radiotherapeutics acquisitions announced since February 2023, with a total deal value equalling $8.6bn. Other big pharma companies, such as Sanofi, are increasing exposure to radiotherapeutics through agreements with early-stage private companies.