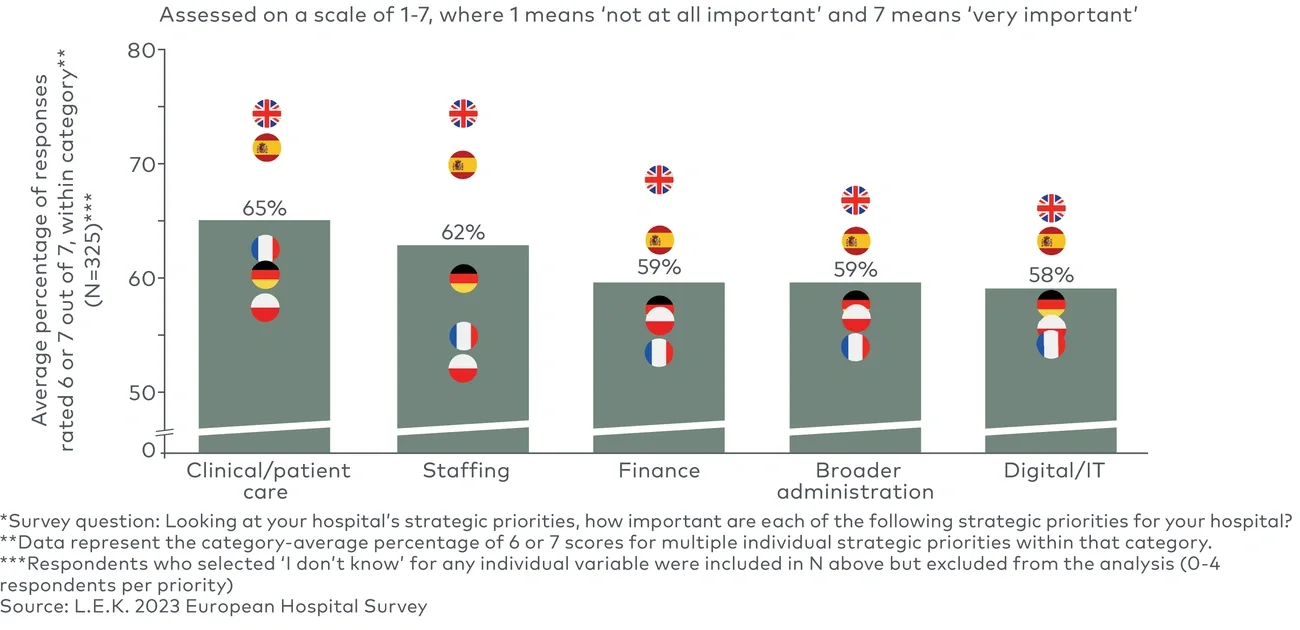

Quality of clinical and patient care

Preserving and improving clinical care quality continues to be at the forefront of hospitals’ priorities as they strive to keep advancing the standard of care whilst grappling with operational challenges such as staffing shortages, capacity constraints and funding pressures. In the UK, Germany, France and Spain, respondents reported at least three of their top five priorities focus on patient and clinical care.

When considering the most important patient and clinical care priorities, there were multiple areas of overlap as well as some nuances between EU countries:

-

Reducing medical errors was a top hospital priority among all countries surveyed, with c.80% of respondents rating its importance as moderately to very important (6 or 7 out of 7)

-

Secondly, improved infection control was rated as similarly important by c.60%-70% of respondents in France, Germany and Poland and c.80% in Spain and the UK, likely driven by the impact of the recent COVID-19 pandemic

-

Reducing readmission rates and improving performance on quality metrics, two of the many other patient care priorities, are considered somewhat more important by respondents in Spain and the UK compared to the other countries surveyed (though Spanish and UK respondents tended to provide higher importance scores for priorities in general)

In France, the focus on quality of clinical and patient care is especially pertinent due to the Financial Incentive to Quality Improvement (Incitation Financière à l’Amélioration de la Qualité, or IFAQ) budget, which provides additional funding to hospitals based on eight quality of care criteria. This creates an incentive for hospitals to focus on improving quality metrics and an opportunity for investments in medtech products to achieve this.

Overall, these priorities must also be considered in the context of staffing shortages, which will be discussed in detail shortly. Achieving high quality in these areas is more difficult when hospitals are short-staffed, and clearly hospitals are focused on maintaining or improving their ability to deliver on key priorities with the teams they have. Due to this, hospitals are likely to be more interested in exploring and investing in new product and service options that offer quality of care improvements and support stretched medical teams. Medtech companies should capitalise on this by tailoring their product design, evidence generation, value proposition, and sales and marketing to explain how their products can help hospitals improve on these metrics.

Staffing

As in previous years, staffing remains a top priority area for hospital providers as European countries grapple to varying degrees with staffing shortages; for example:

-

In Germany, the German Medical Association expects its current physician shortage to increase in the near future, as over 20% of its physicians are 60 and older as of about 2021. As such, German hospitals rated physician attraction and retention the number two strategic priority, with improved staff utilisation, attraction and retention of nurses and allied medical specialties/non-clinical staff rated the next most important priorities within staffing.

-

In Spain, while the number of doctors is increasing, there is significant variation in distribution, leaving some areas with far fewer HCPs per 1,000 population than others. Like German respondents, Spanish hospital respondents also rated physician attraction and retention a very important strategic priority, with attraction and retention of nurses and allied medical specialities/non-clinical staff considered somewhat less important.

-

In the UK, there were over 133,000 vacancies in the National Health Service (NHS) in September 2022 (c.57,000 of which were medical or nursing posts), which was an increase from c.104,000 in the previous year (c.48,000 of which were medical or nursing posts). Clinical staff shortages, including nurses and physicians, have been so widespread that they have triggered government involvement and have been included as a core focus area in the NHS Long Term Plan published in 2019, to support the NHS’ recruitment and training of professionals and to improve staff retention.

-

In France, staff shortages are concentrated mainly in non-clinical staff and allied medical specialties (e.g. dietitians, occupational therapists and physiotherapists), which is the top staffing priority for hospitals.

-

In Poland, actions are already being taken to attempt to boost medical staff numbers (e.g. financial incentives to attract doctors to areas with relatively fewer doctors).

One way that medtech companies can help hospitals address staffing challenges is to provide new innovations that allow more efficient patient monitoring and reduce the number of interventions required (e.g. automated or self-operated IV pumps, portable patient monitors, or automated patient turning solutions) or increase the number of outpatient procedures that can be performed (where, by definition the reduced length of stay will increase the productivity of staff). They can also develop devices and tools that support upskilling nonphysician staff and help providers better utilise their existing personnel.

Other priorities

Beyond patient care and staffing, respondents also considered areas of digital, administration and finance to be important. In particular, these include:

-

Respondents in the UK, Spain and Poland prioritised improving change management as a top administrative priority, with c.70% rating it as moderately to very important (6 or 7 out of 7 in importance)

-

Several finance areas were perceived to be high priority, including but not limited to participation in other value-based arrangements and access to capital for purchase of medical equipment as well as improved RCM/billing/cash recovery, which were each considered moderately to very important by c.55%-60% of all respondents

-

Lastly, important digital priorities included fully integrated electronic medical records across acute and non-acute settings, patient-facing technology, enhanced data connectivity, and improved clinical workflow efficiency tools, with some variation between countries

Variety of priorities in Poland

At a country level, Poland’s top priorities span the broadest range of areas, including finance (access to capital for purchase of medical equipment), broader administration (improved change management and implementation of process improvement), digital technology (clinical data connectivity and patient-facing technology) and clinical/patient care; this reflects the stage of development of Poland’s market versus those of Western European countries. Medtech companies serving Poland (and other Central and Eastern European countries) would benefit from offering a diverse and agile product range and communicating to hospital providers how particular products are adapted to fit changing priorities as the market further develops.

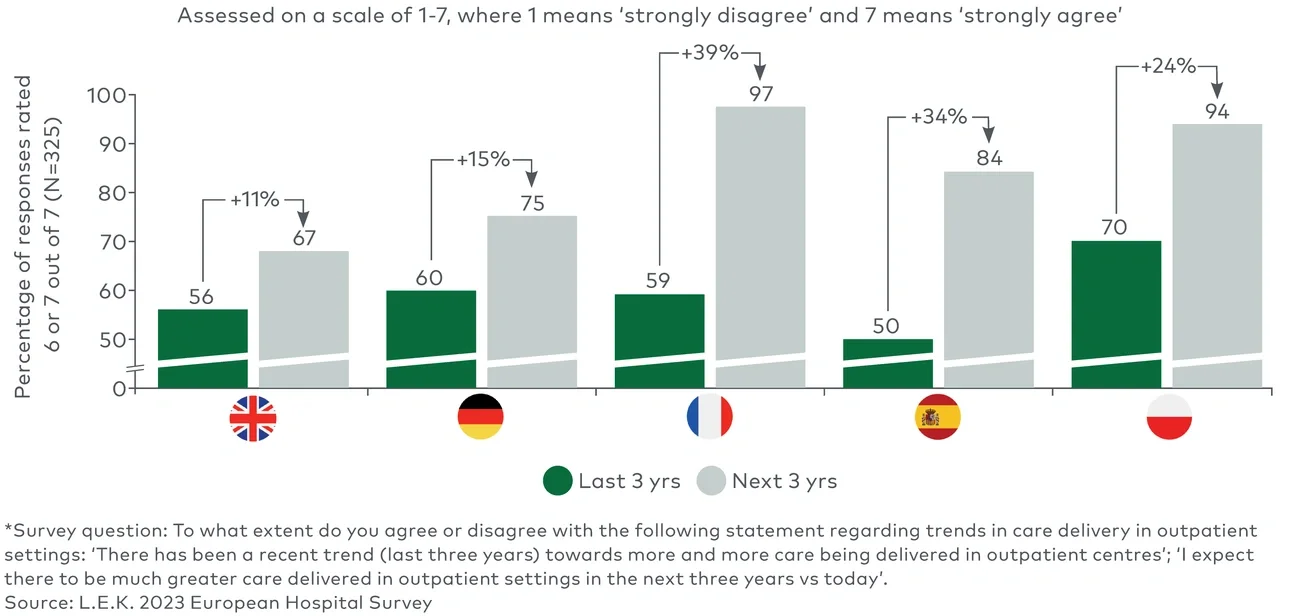

2. The trend towards outpatient/ambulatory care is accelerating; medtech companies should ensure they provide the products and services that will best match the needs of outpatient facilities

Hospitals cite a trend towards increased care delivery in outpatient settings, which they expect to continue and potentially accelerate over the next three years (see Figure 2).

On average across countries, c.60% of respondents cited strong agreement that this trend has been occurring over the past three years, and c.80% reported the same for the outlook across the next three years. This shift is motivated by the need to reduce costs while maintaining or improving quality of care, and it is enabled by improving medical technology (e.g. in minimally invasive surgery, anaesthesia), allowing more procedures to be performed in outpatient settings.