Executive Summary

Over many years, France has built a well-established healthcare system that offers comprehensive care access through state-funded social health insurance and contributes to the country’s high life expectancy, compared with the European average. However, the system has struggled with shortages of healthcare professionals (HCPs) and in 2020 was one of the nations hardest hit by COVID-19 (by caseload and number of deaths per population), which worsened staffing pressures and caused a significant increase in hospital spending to support the country’s pandemic response.

Today, hospitals in France are concentrating on improving the quality of patient and clinical care; alleviating staffing pressures; controlling spending; expanding further into outpatient services; investing in digital health; increasing their supply chain resiliency; implementing environmental, social and governance (ESG) initiatives; and exploring outcome-based pricing models.

In this Executive Insights, L.E.K. Consulting shares key findings from its 2023 European Hospital Survey and discusses some of the key trends affecting hospitals in France.

Key findings

We have identified seven key themes from the European Hospital Survey that are of particular importance to hospitals in France.

-

Enhancing clinical and patient care quality is the most important priority for French hospitals; staffing is also important due to current shortages of non-clinical staff and allied medical specialists

-

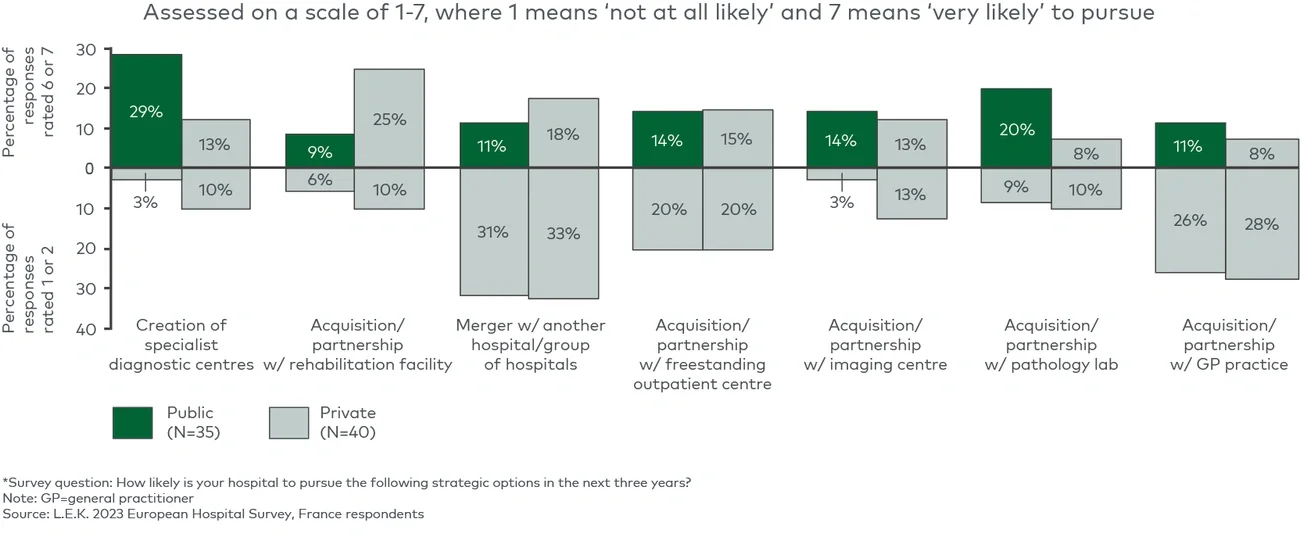

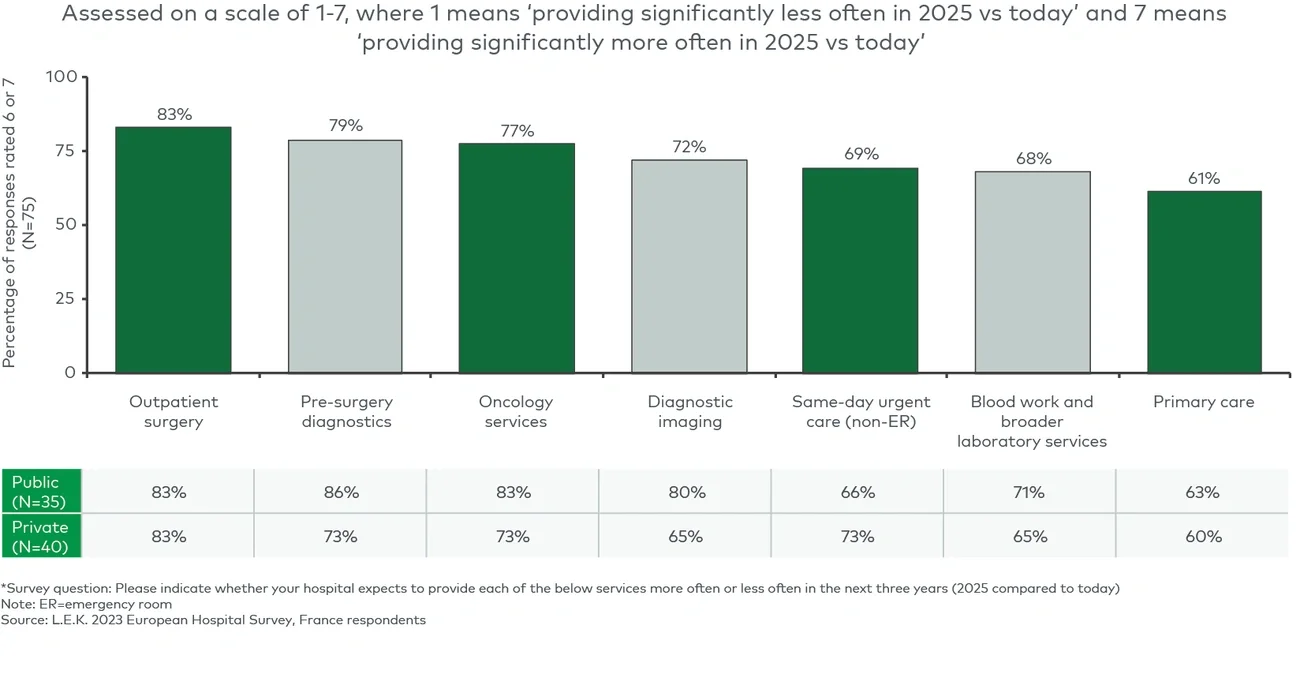

The majority of hospitals expect to increase the frequency of their outpatient services, particularly outpatient surgeries, as continued innovation enables faster recovery times, and shifting towards greater outpatient care creates cost savings

-

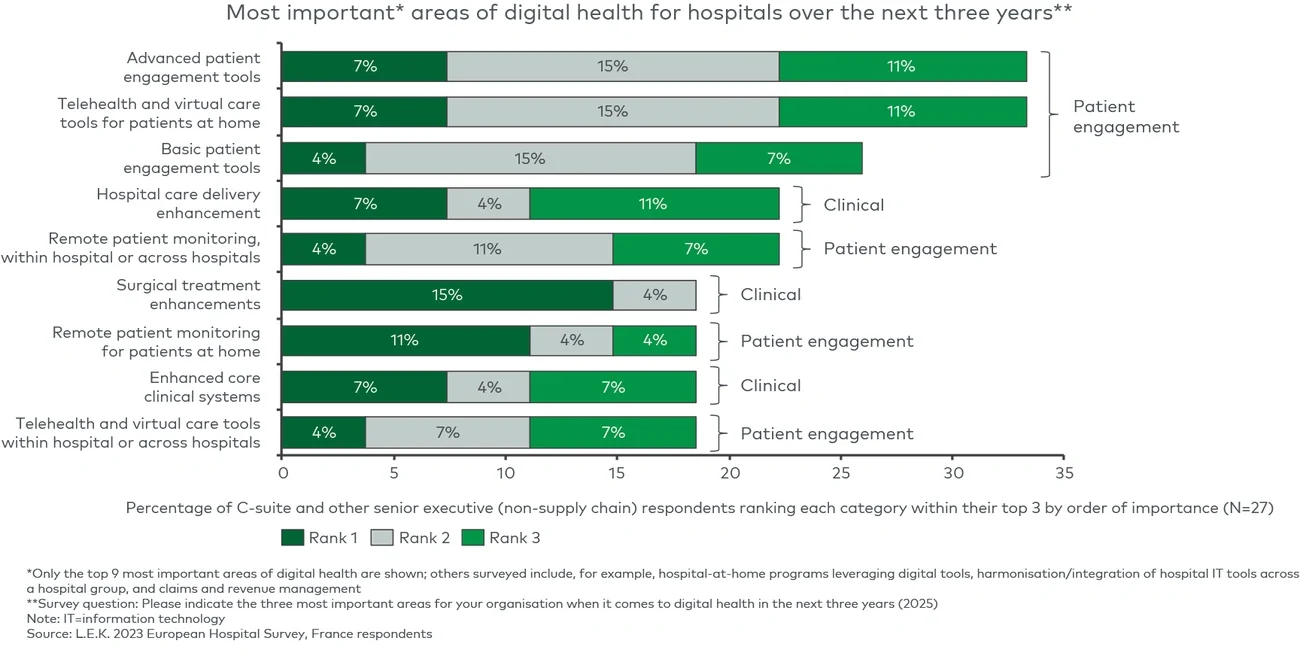

Digital health tools for patient engagement and monitoring, which will support the focus on improving patient and clinical care, are top digital priorities for many hospitals

-

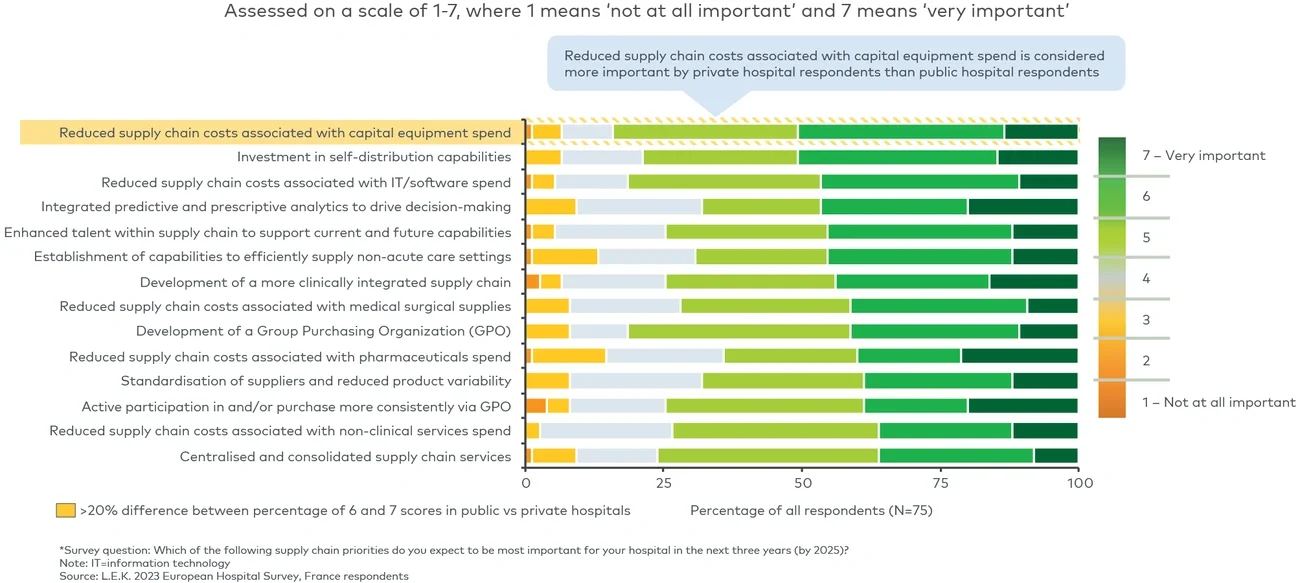

Following the challenges of the COVID-19 pandemic, many hospitals are looking to increase supply chain resiliency (e.g. by investing in new self-distribution capabilities) and reduce supply chain costs

-

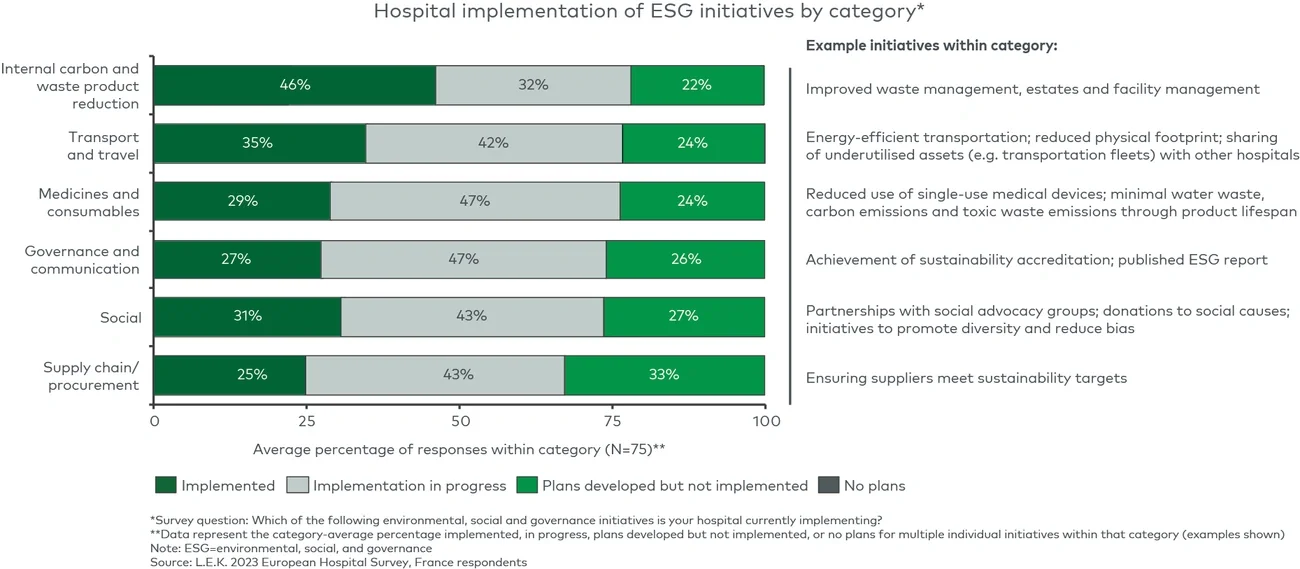

Hospitals have already or are currently widely implementing several types of ESG initiatives, including those relating to internal carbon and waste product reduction, transport and travel, and medicines and consumables

-

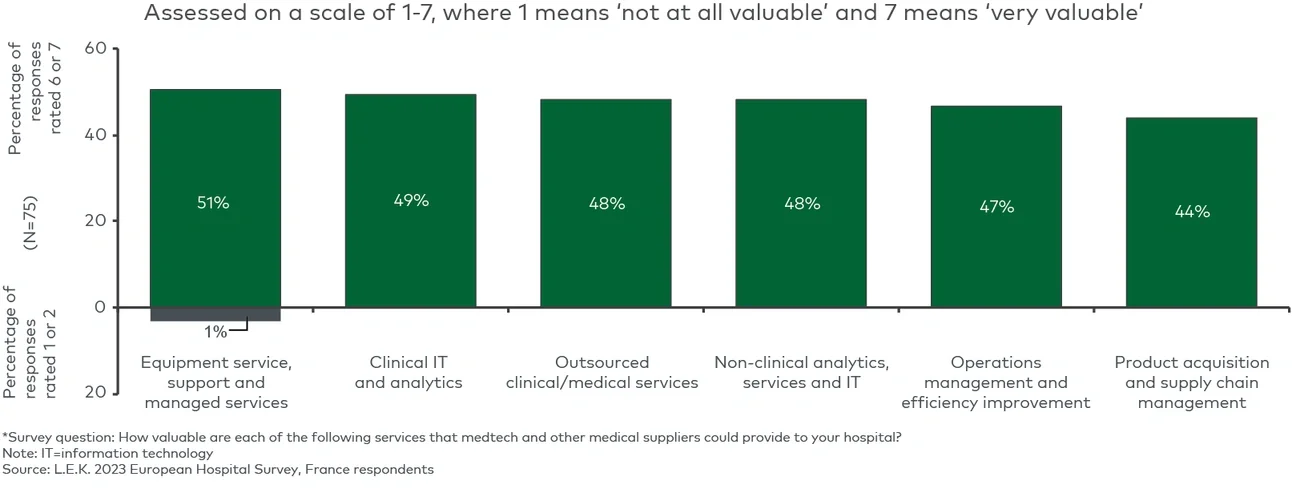

A significant proportion of hospitals are interested in services from medtech or other medical suppliers and see value in a broad range of services, including equipment service support and clinical information technology (IT) support

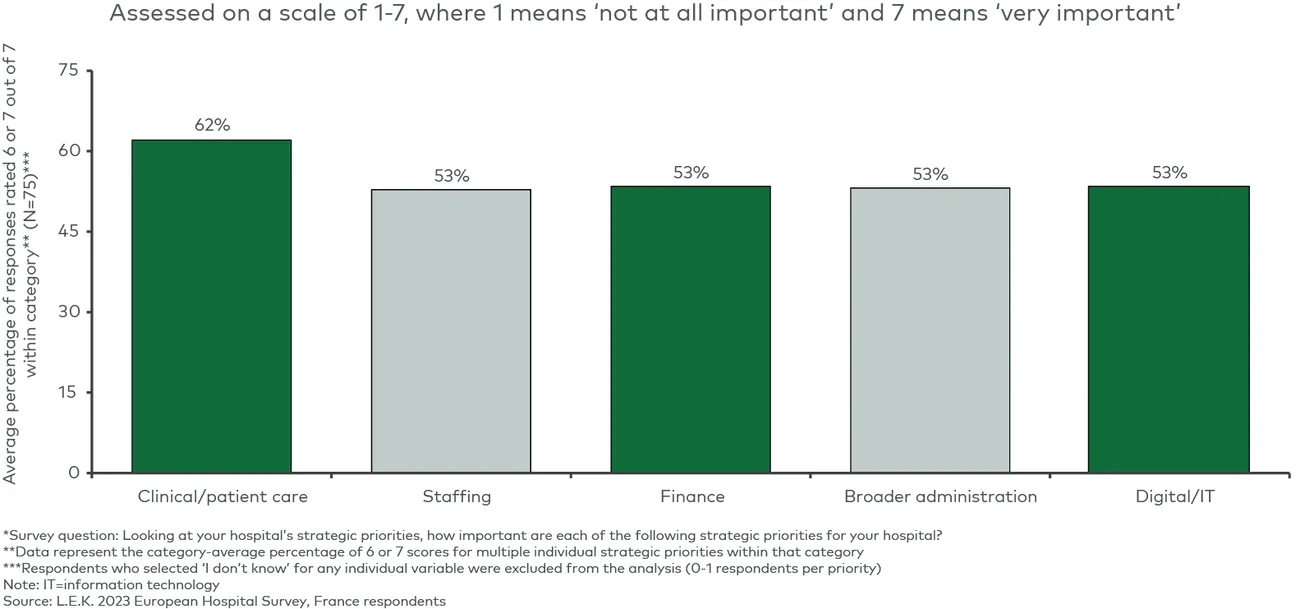

1. Enhancing clinical and patient care quality is the most important priority for French hospitals; staffing is also important due to current shortages of non-clinical staff and allied medical specialists

Hospitals in France are balancing a broad range of priorities across patient and clinical care, staffing, broader administration goals, financial metrics, and pursuit of digital/IT priorities, with patient and clinical care considered to be most critical (see Figure 1).