Executive summary

Spain’s healthcare system has a highly varied distribution of healthcare practitioners across different regions and over the recent past has received only modest funding to support it. Per-capita spending has been consistently below the EU average and, as a result, many hospitals have old medical equipment, nursing staff shortages and long wait times for treatment that are affecting the quality of care in some areas. The COVID-19 pandemic has further exacerbated some of these challenges. Staffing shortages have intensified and the primary care sector is unable to meet demand, leading to patients instead saturating hospital accident and emergency departments.

Today, hospitals in Spain are focusing on improving the quality of patient care; increasing access to doctors and nurses in regions with greater need; increasing outpatient services provision; continuing to advance digital health capabilities; achieving cost optimisation; implementing environmental, social and governance (ESG) initiatives; and, in the future, exploring outcome-based pricing models.

In this Executive Insights, L.E.K. Consulting shares key findings from Spanish hospital respondents from its broader 2023 European Hospital Survey and discusses some of the key trends affecting hospitals in Spain.

Key findings

We have identified seven key themes from Spanish respondents in the European Hospital Survey that are of particular importance to hospitals in Spain:

-

Continuing to improve patient outcomes and clinical care and attracting and retaining staff are the top strategic priorities for hospitals in Spain

-

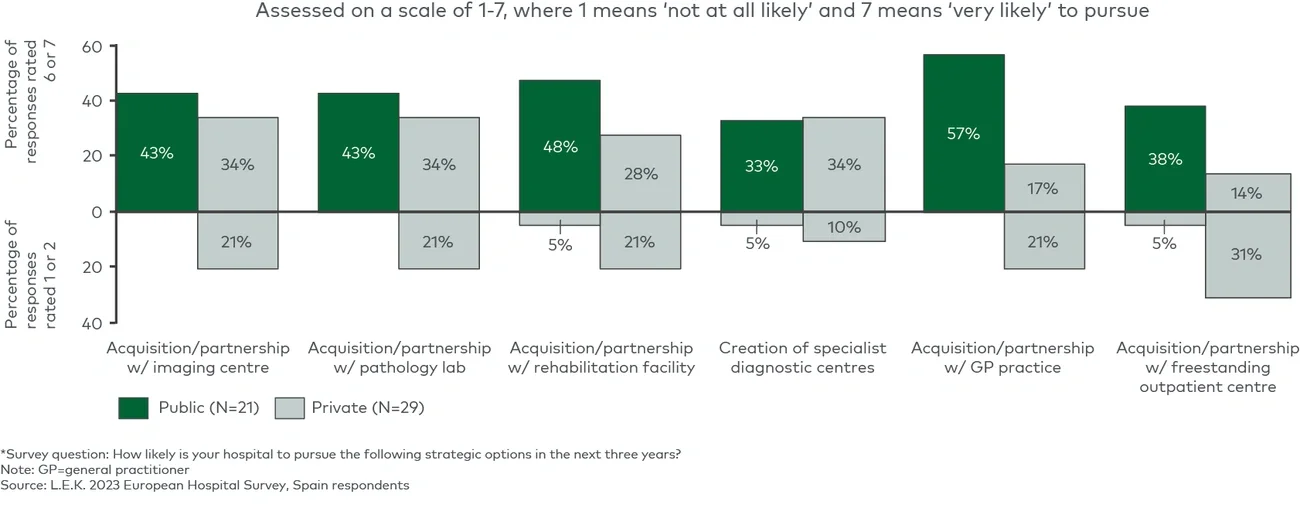

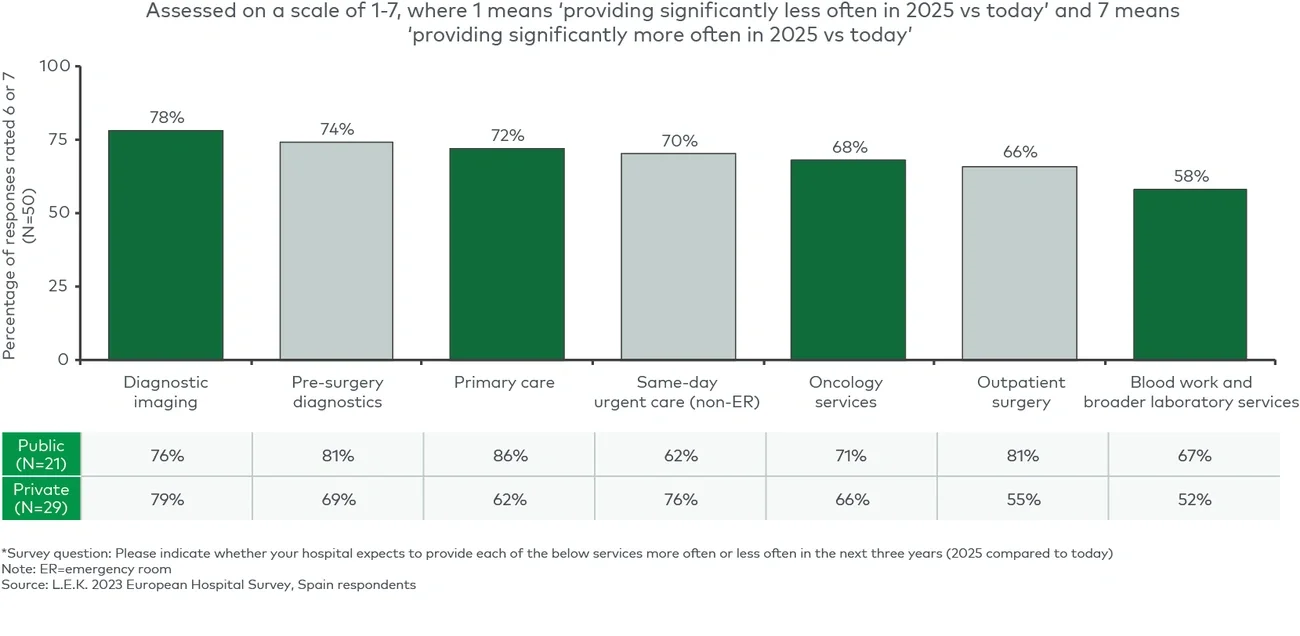

The majority of public and private hospitals expect to provide more outpatient services in the next three years, notably in diagnostics, primary care and urgent care

-

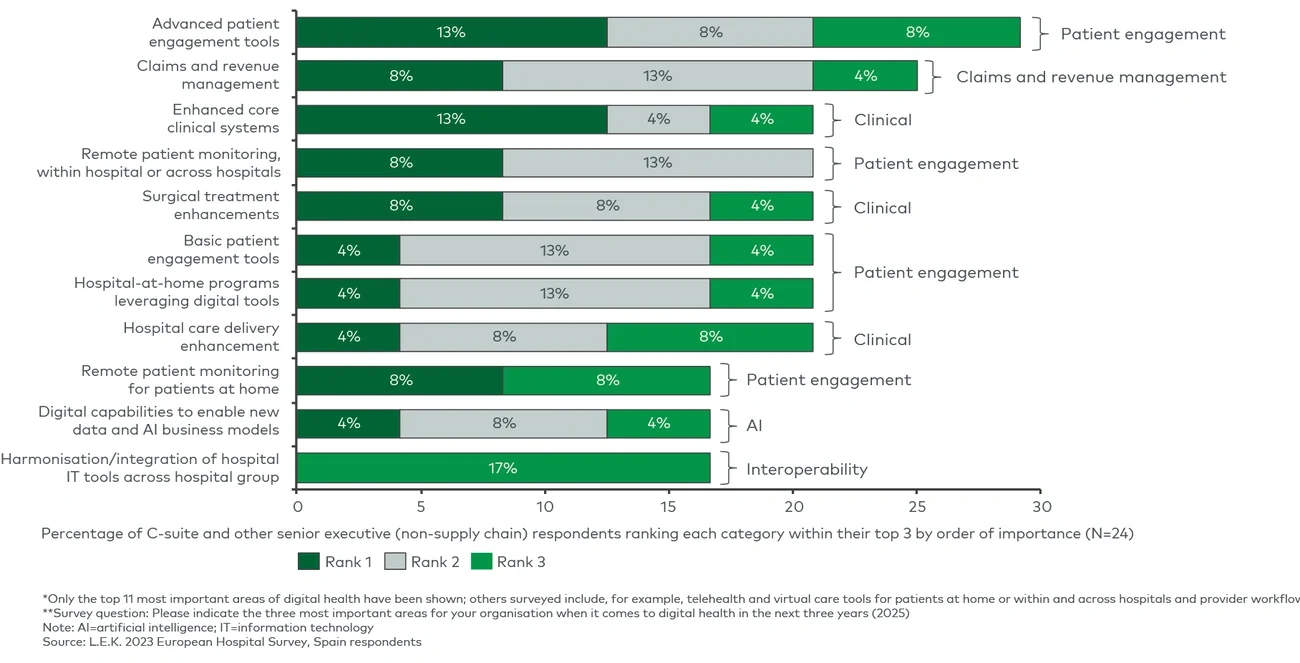

Patient engagement, claims and revenue management, and core clinical system enhancement are top digital priorities for many hospitals and will support their focus on improving patient and clinical care

-

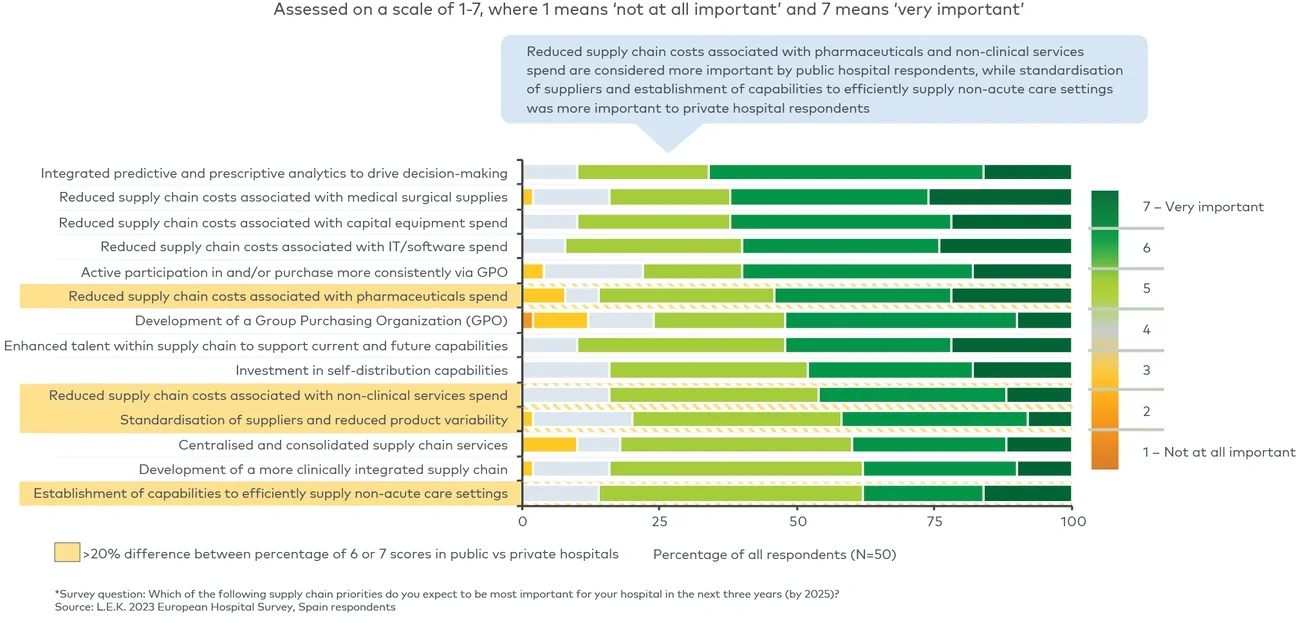

Many hospitals are looking to reduce costs within their supply chains as well as prioritise integrating predictive and prescriptive analytics to drive decision-making processes

-

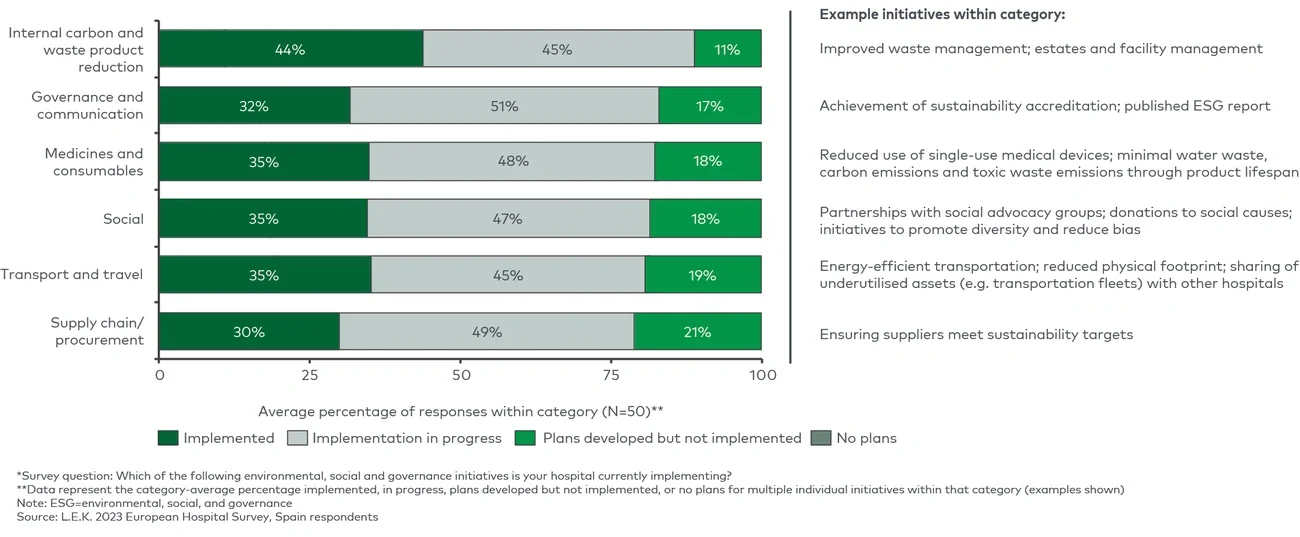

Hospitals are widely implementing ESG initiatives, particularly those relating to internal carbon and waste product reduction such as improved waste management

-

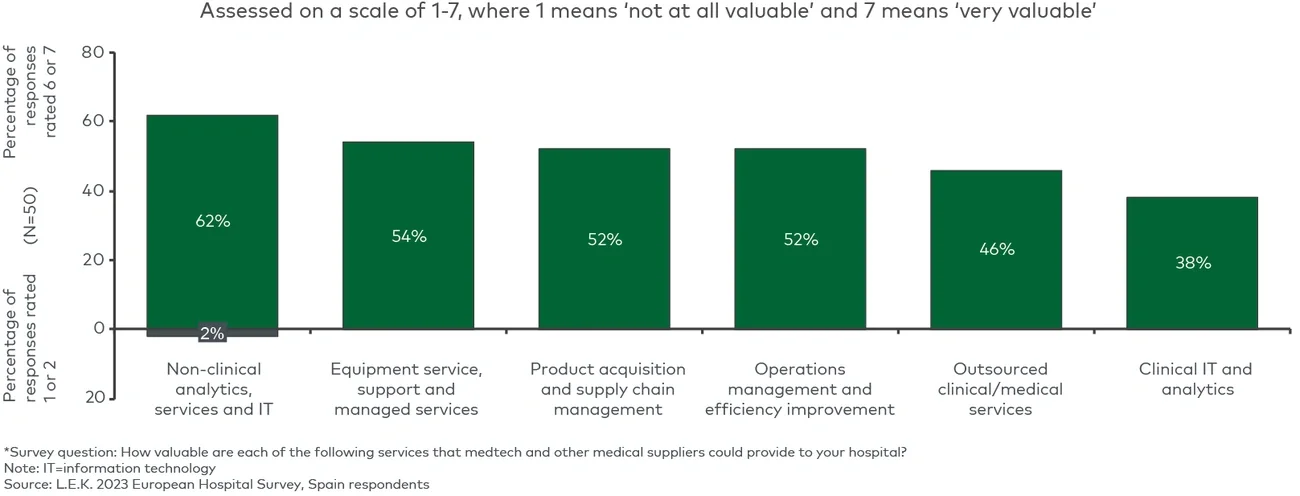

A significant proportion of hospitals are interested in a broad range of services from medtech or other medical suppliers, including non-clinical analytics and equipment service and support

-

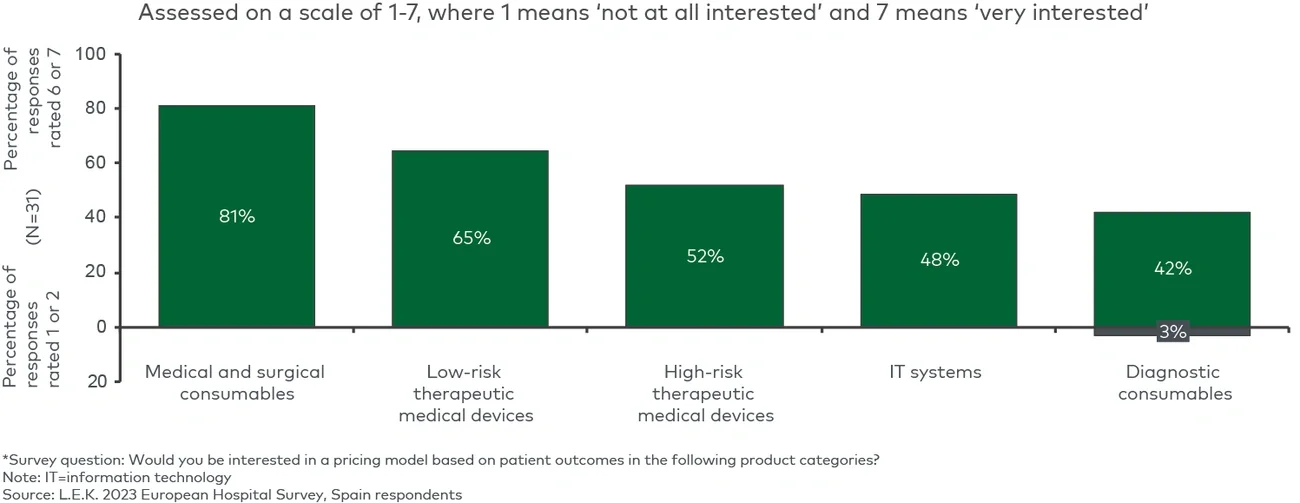

In line with the expected emergence of outcome-based pricing options, some hospitals show interest in using such models for certain product categories, particularly medical and surgical consumables

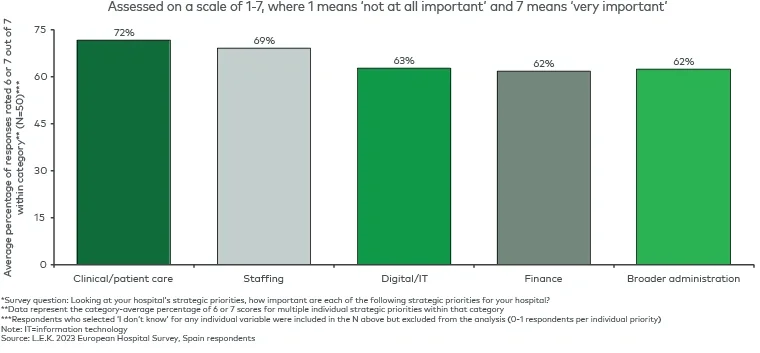

1. Continuing to improve patient outcomes and clinical care and attracting and retaining staff are the top strategic priorities for hospitals in Spain

Hospitals in Spain are balancing multiple priorities across patient and clinical care, staffing, digital/IT, finance, and broader administration goals. Staffing and patient/clinical care priorities are considered the most critical (see Figure 1).