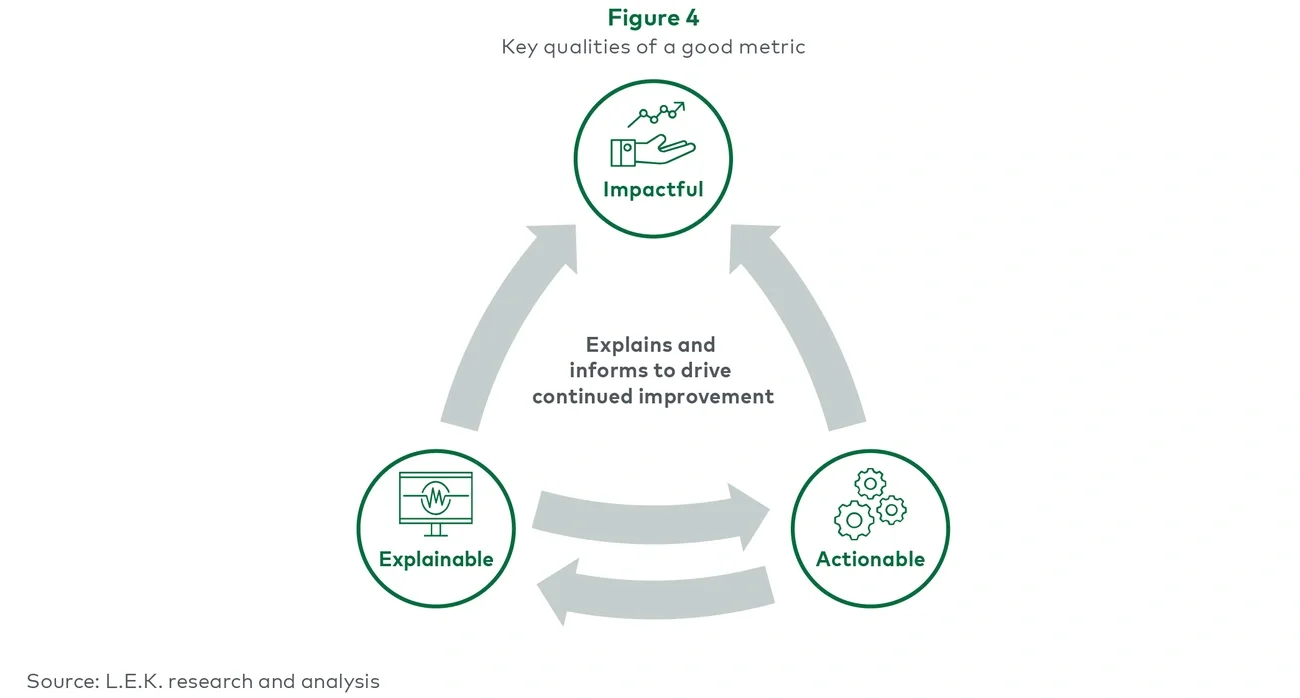

For decades, the insurance broking industry has relied on a limited pool of key metrics of which new business, retention rate and commission are core and have served businesses well. However, the market today is very different from what it looked like a decade ago, as the influx of private capital has transformed the scale of businesses, the level of competition and sometimes the mode of growth. This is complemented by deployment of technology and access to data at a scale that is unprecedented in the sector. Given these changes, it is time to consider the best ways to understand business performance that allow targeted action and measurement of cause and effect to enable more sustainable, organic value creation.

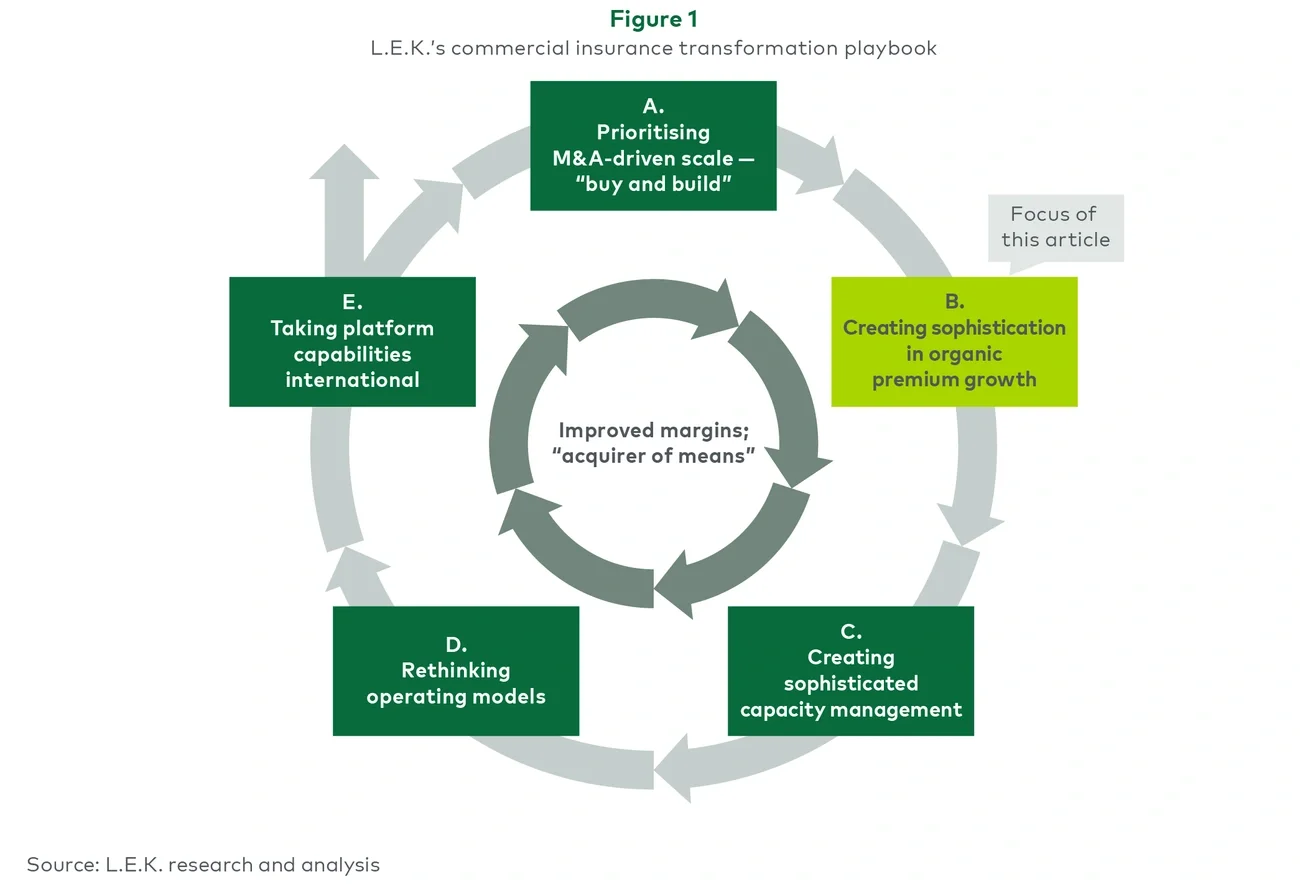

In our previous report “In the Foothills of Excellence: Spotlight on Commercial Insurance Broking,” L.E.K. Consulting proposed a commercial insurance broking transformation playbook with five growth levers (see Figure 1).