There have been many prophecies of disruption in insurance, but change has been slow and the role of the traditional insurance broker remains pivotal in the world of commercial lines and specialist personal lines business.

Insurance brokers handle over 100 billion euros of premiums p.a. in Europe alone, and similarly large quanta in North America and the growing markets of Asia-Pacific. Brokers’ access to customers remains robust, from micro-SMEs to large corporates. Millions of businesses look to their brokers to help protect against risks, both old and new (e.g. cyber), and navigate remediation when risks translate into claims.

However, this trust-based relationship is not an excuse for the broking industry to stand still. Market forces, the advent of technology and higher customer service requirements have created an imperative for change ― change that preserves the customer relationship while creating greater value for businesses and also enabling them to respond to future needs.

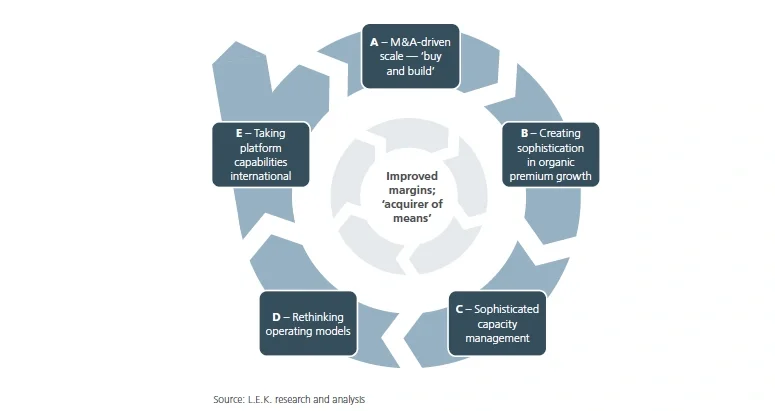

Change, however, is not straightforward, and brokers need to have a clear idea on the commercial agenda for their businesses. Scale is a significant consideration ― whether to deploy technology or to be more effective in capacity management. Inorganic growth is a key enabler of this, and it is important that becoming an ‘acquirer of choice’ and an ‘acquirer of means’ is a key design objective for companies.

In this Executive Insights, L.E.K. Consulting examines the key steps in the commercial insurance transformation playbook to achieve these objectives. These are pivotal in unlocking the significant value creation opportunity for customers, management teams and investors (see Figure 1).