Lenders can use a variety of levers to create successful going-forward strategies. These strategies differ by bank type and lending class and include especially strong opportunities for specialist lenders and/or those with complex, data-driven underwriting capabilities.

Big banks. To help them capture the seven out of 10 Americans who say they would switch to a financial institution with more inclusive lending practices, big banks should use machine learning and big data tools to augment credit reports with real-time income or cash-flow data. They should also continue their accelerated shift to online channels, as all lenders will need to keep investing in seamless engagement, underwriting and servicing experiences. Large financial institutions that prioritize digital innovation to optimize their consumer interactions are likely to see the most competitive upside over the long term.

Small banks. Against a backdrop of increased interest in lender trustworthiness; intuitive digital application processes; personal loans for new entrants; and self-serve, omnichannel digital lending experiences, small banks should position themselves to meet changing consumer demand.

Specialist lenders. To capture customers that the larger prime banks have turned away, specialist lenders should actively position and market themselves to newly nonprime borrowers. Specialist lenders should also continue to offer tailored solutions through open banking for those with complex and nontraditional financial needs. Doing so will help streamline the mortgage approval process; it will also help the specialist lending sector deliver tailored solutions to this growing segment of the market with greater speed and efficiency.

Subprime lenders. To meet the evolving preferences and needs of consumers, subprime lenders should also actively position and market themselves to customer groups that have been newly rejected by mainstream lenders. Subprime lenders could also offer POS financing as an alternative to credit cards. Presenting line of credit financing as personal loans to consumers who make frequent, small-dollar transactions will help combine the strengths of personal loans and credit cards to target initial consumer transactions. And to better assess customer risk profiles, subprime lenders should invest in automation, which will help remove any replicable rule-based process from humans by leveraging AI and machine learning, allowing lenders to scale up without the need for a corresponding increase in team size.

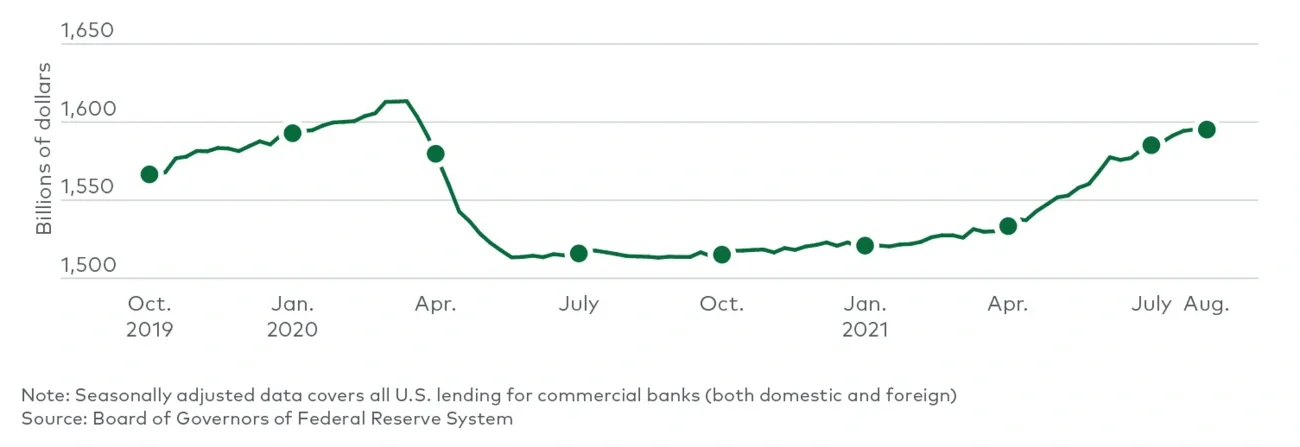

COVID-19 has prompted U.S. lenders across the board to reconsider their participation in consumer lending. And those lenders that remain have pulled back on new business volume as they try to determine:

- How secure their funding is and the level of volume it will support

- To what degree new lending should match up with the overall operating cost base of their business

- How to assess the creditworthiness of new customers

- How confident they are in both the performance of their back books and their cost expectations to allow for increased collection activities

Economic shocks and the downturns they yield also create opportunity, and COVID-19 is no different. And unlike in the great financial crisis, the federal government has provided a significant amount of fiscal relief to help consumers meet their loan obligations. Banks and specialist lenders, and their investors, need to embrace strategies that make the most of their capabilities while directly addressing the needs — and evolving behaviors — of their target customers.