The activation of open loop payments in our transit systems is continuing at pace. Open loop unlocks material benefits for an adult full fare-paying transit customer. But it also poses challenges and a range of considerations for transit agencies:

- How do they strike a balance between customer benefits facilitated by open loop payments and the use of lower-cost fare channels?

- How do trends in debit and credit use affect the Cost of Fare Collection (COFC)?

- What is their capacity to pass through credit card costs to the customer?

- Should concessions be supported by open loop payments?

- What are the risks of fraud associated with open loop payments?

A catalyst for investment in fare collection

The capacity to support contactless open loop payments has been a major catalyst for transit agencies around the world to invest in their fare collection systems in recent years. Some selected examples:

“[open loop payments is] to be rolled out in phases across [metro train] stations and [CBD and highway] buses [in the Philippines], with the intention to scale contactless payments acceptance across ferries and other modes of transportation in the future, and eventually across the country”

- Mastercard content exchange, February 2024

“The Victorian government [awarded] Conduent a $1.7B contract … to replace the card-based ticketing system with an account-based ticketing system, giving Victorians the future ability to pay for public transport using debit and credit cards, as well as connected smart devices”

- Innovation Aus, June 20232

The introduction of open loop also extends to Hong Kong, which launched the second and, arguably, most successful, closed loop smartcard system in 1997. Some 98% of Hong Kong residents have an Octopus card for both transit travel and low value retail purchases. However, in December 2023, open loop payments were introduced into the Hong Kong MTR heavy rail network via an exclusive arrangement with Visa. It comprised two gates per station with the target market being international tourists. Further expansion is planned.

Transit customer benefits

There is little doubt that open loop unlocks major benefits from a customer perspective, specifically a full fare-paying adult customer. There is no longer a need to carry a dedicated transit card or have funds tied up in a card e-purse. Customers can also use a digital wallet, eliminating the need to present a physical card. The benefits are even greater for the non-resident who is spared the cost and time of acquiring yet another transit card and loading funds to the card.

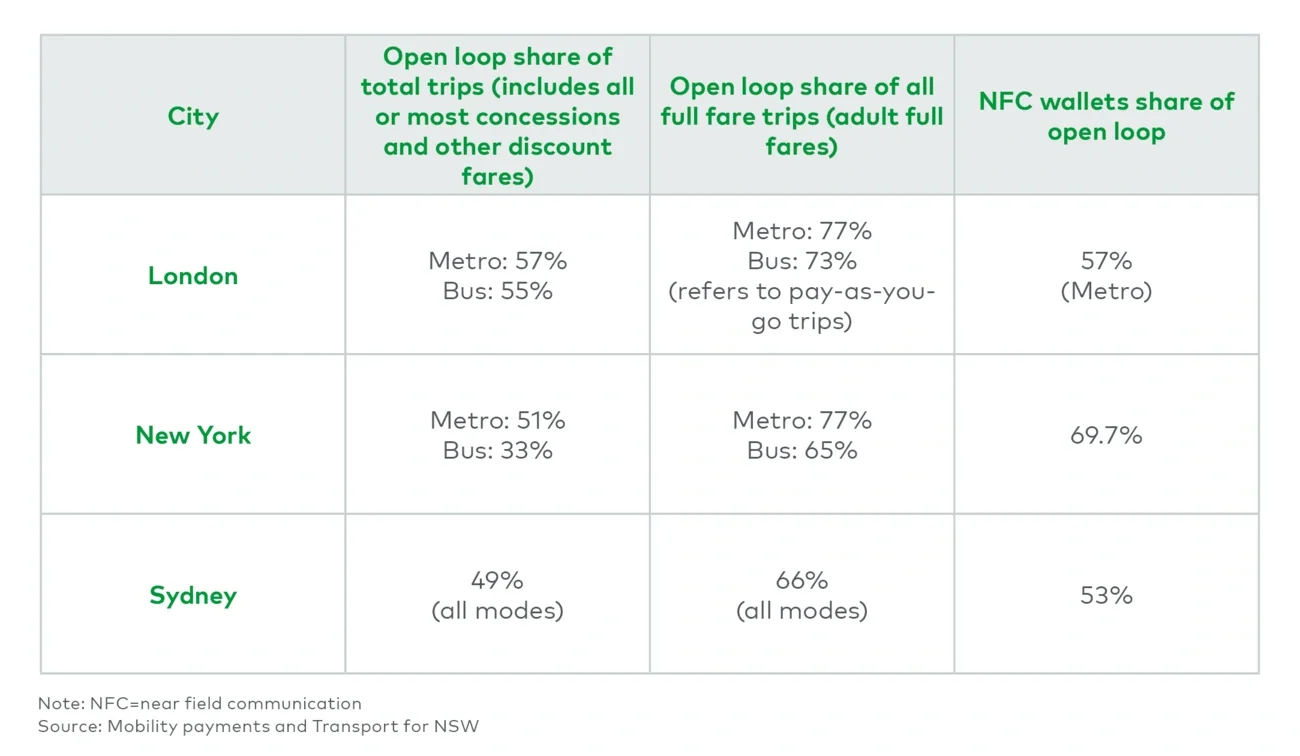

Data from three major international cities highlights the attractiveness and success of open loop. The open loop percentage of total adult full-fare trips ranges from the mid-50s in Sydney to the mid-70s for metro (subway) services in London and New York. Moreover, the majority of these transactions are being supported by a digital wallet rather than the presentation of a physical card (see Table1).