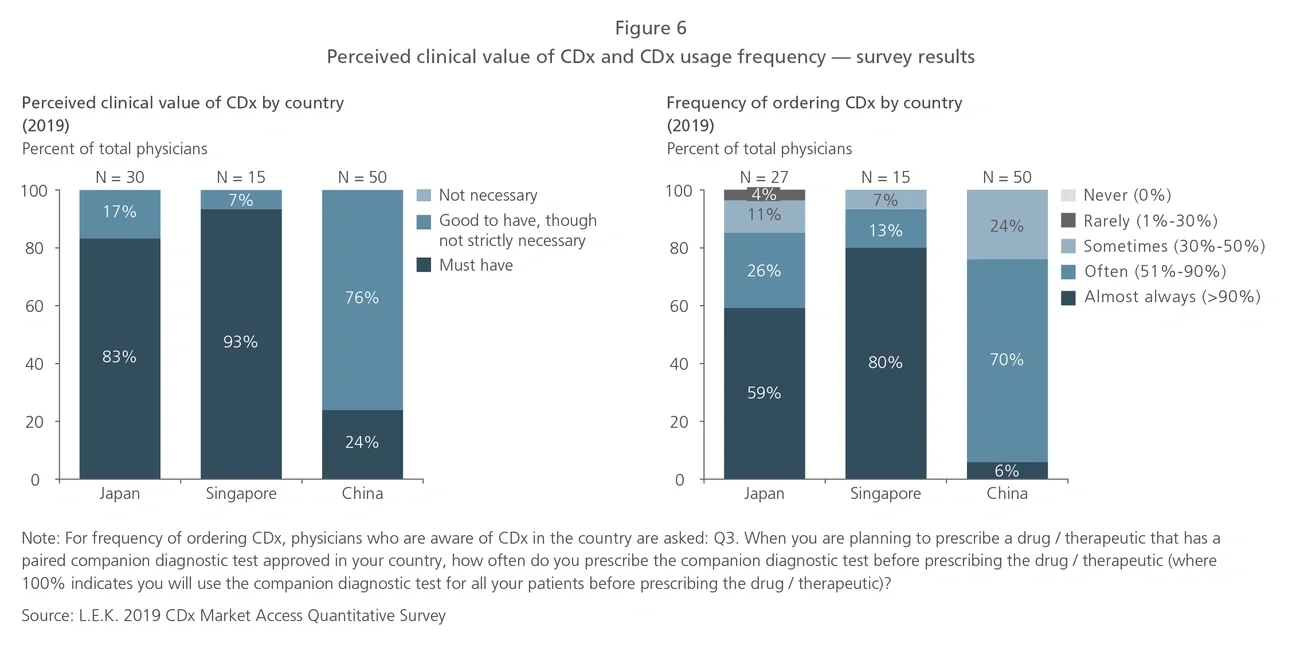

The Asia-Pacific (APAC) region, which is home to 60% of the world’s population, makes up a significant share of the global cancer burden. Given the higher prevalence of specific cancers in APAC and distinct Asian patient genotypes, diagnosis and treatment should be tailored to the APAC population. Therefore, opportunities exist for industry players to develop and increase the clinical use of precision oncology therapies and diagnostics to meet the specific needs of the APAC market.

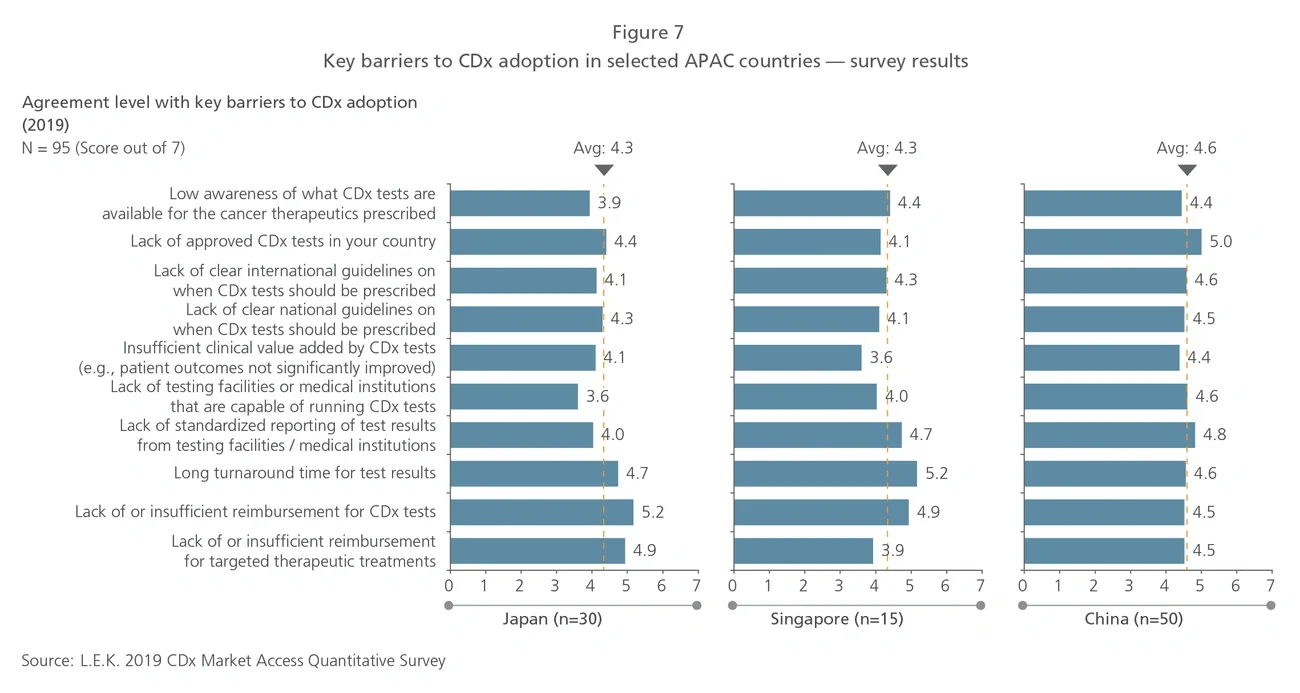

In 2018, APAC accounted for 60% of the world’s lung cancer cases and deaths, and 75% of all gastric cancer cases and deaths.1 APAC’s high cancer burden will lead to increased healthcare costs. Oncology spending in Japan and pharmerging countries such as China and India is expected to hit almost US$20 billion by 2022.2 This is still significantly lower than the US$140 billion projected to be spent by the U.S. and the EU-5. Pharmerging markets spend less on oncology therapeutics and diagnostics because usage is constrained by availability and reimbursement.

Interestingly, Asian patients also have distinct genotypes in specific cancer types. For instance, East Asian patients with non-small cell lung cancer are more likely than their Caucasian counterparts to develop epidermal growth factor receptor (EGFR) mutations, and are also more responsive to treatment with EGFR tyrosine kinase inhibitors.3

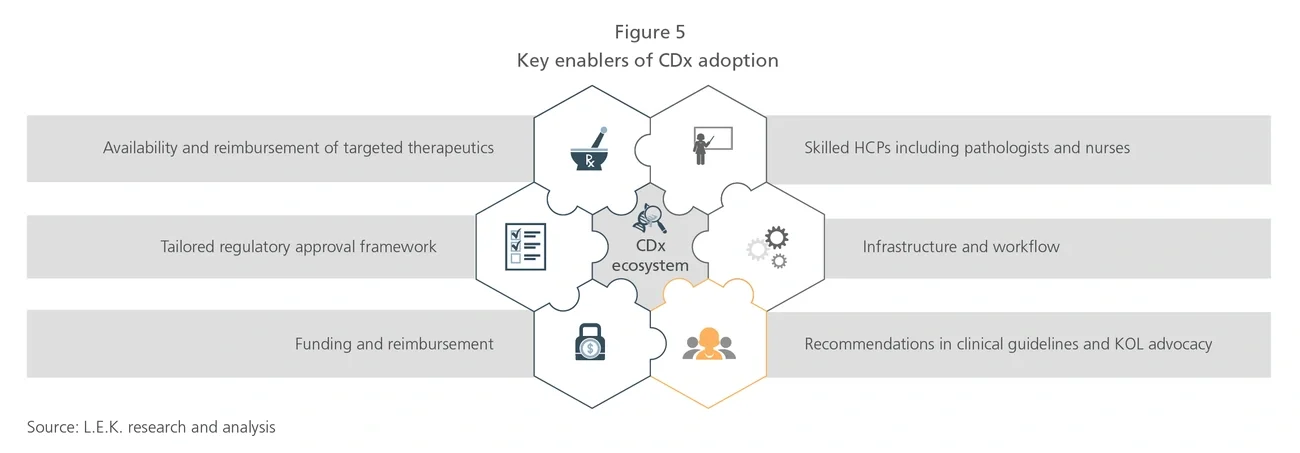

How CDx can play a critical role

Precision oncology involves various diagnostics tests, such as companion diagnostics (CDx), which determines whether specific targeted therapeutics should be prescribed. Unlike complementary diagnostics, which are associated with a class of drugs and are not limited to specific uses in the labels, CDx is typically linked to a specific drug within its approved label. Although multiple CDx types are used to test for corresponding targeted therapeutics in several diseases, over 90% of globally approved CDx tests are associated with targeted cancer therapeutics.4

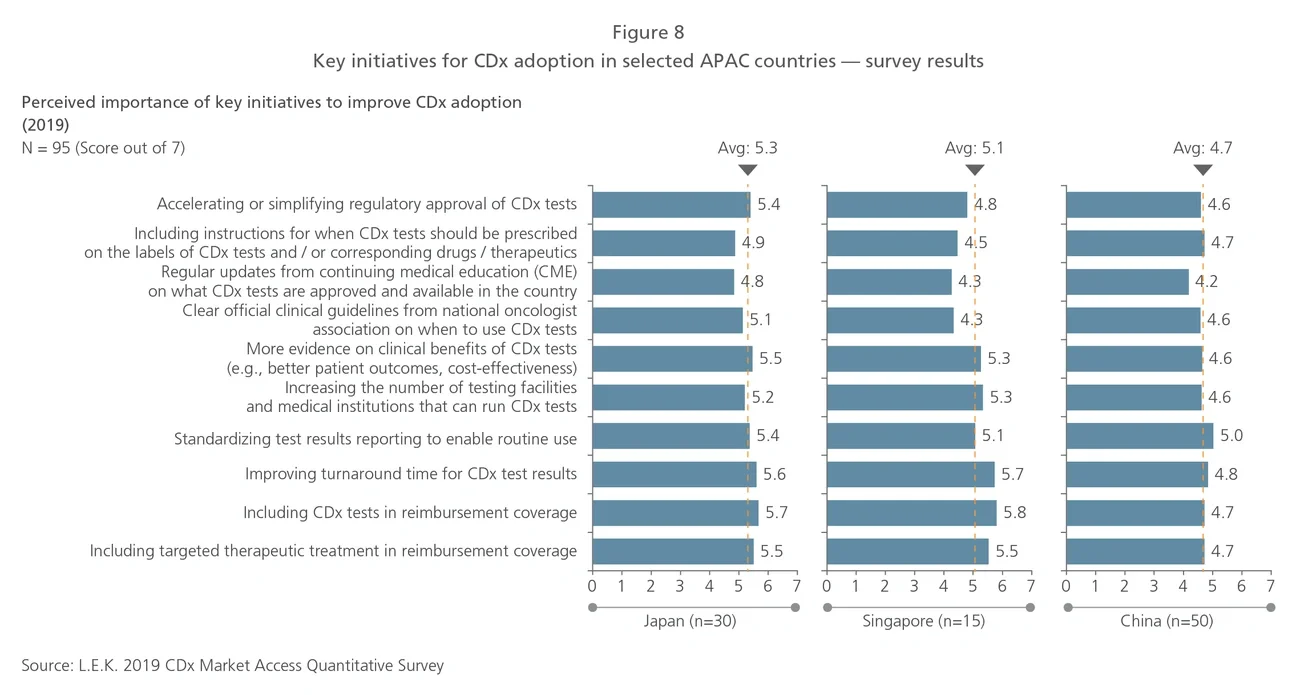

Studies have shown that under specific conditions, CDx can potentially improve the cost-effectiveness of oncology care. For example, a 2015 study on late-stage cancer patients in the U.S. demonstrated that genomic testing and targeted therapy can improve overall survival for refractory cancer patients while reducing average-per-week healthcare costs, resource utilization and end-of-life costs.5

Trends in CDx development

Most CDx tests consist of a mix of single-biomarker tests, performed largely on tissue biopsy samples using quantitative polymerase chain reaction (qPCR), immunohistochemistry (IHC) and fluorescent in situ hybridization (FISH) techniques. Next-generation sequencing (NGS) and liquid biopsy are recent technologies that will be increasingly used and thus will shape the future of the global CDx market. Current industry participants with NGS or liquid biopsy technologies include service providers such as Roche Foundation Medicine and Guardant Health, as well as equipment and reagent providers such as Thermo Fisher Scientific and Illumina. More players with products incorporating these technologies are expected to enter the market over the next five years.