COVID-19 in the US: Consumer Insights for Businesses — Edition 1, Part 2

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

Brought to you by L.E.K. Consulting's Center for Consumer Insights, in partnership with Civis Analytics

In partnership with Civis Analytics, we’re publishing a series of insights on the consumer response to COVID-19. Our goal is to help our consumer-facing clients monitor sentiment and behaviors as they take shape during this unprecedented period. At the same time, we acknowledge that the pandemic is a humanitarian crisis first and foremost. We at L.E.K. Consulting extend our heartfelt sympathies to all who are affected by this crisis.

Our COVID-19 Consumer Insights Series reflects the results of a recurring consumer pulse survey. Administered approximately every two weeks, the survey tracks the pandemic’s impact on consumer sentiment overall, as well as by segment, geography and product. Each edition offers an updated perspective on the current landscape and what the lasting impact will likely be.

We began to analyze the first edition of the survey last week, which includes insights regarding current consumer sentiment for the economy, as well as the estimated impact to date on travel and nontravel expenditures so far.

Our first survey yielded a number of additional insights that we are excited to share with you now, including:

Important note: All forward-looking data reported are a reflection of consumer sentiment/expectations as of the first edition of the survey and are not official L.E.K. Consulting forecasts.

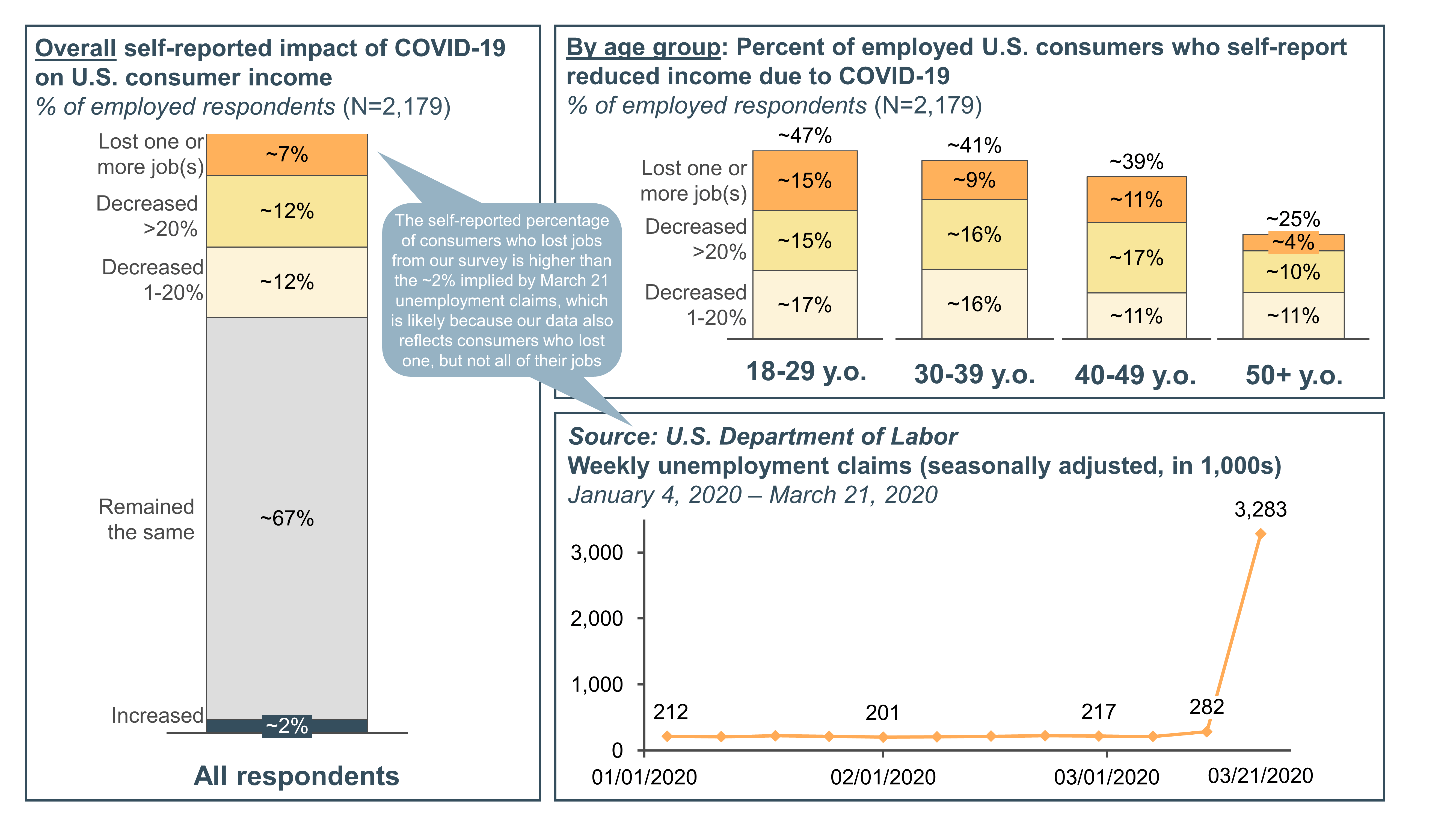

Consumers self-report a significant impact to their income resulting from COVID-19. Approximately 30% of all consumers report a decline in their income.

Specifically, ~7% report that they have lost one or more of their job(s) entirely. Another ~24% report that their overall income has been reduced since the outbreak began (~12% report a significant reduction in income of greater than 20%, and the remaining ~12% report a moderate reduction in income of 1%-20%).

Young consumers appear to be affected the most. Approximately 47% of respondents ages 18-29 reported a decrease in income compared to just ~25% of respondents ages 50+.

These self-reported income trends from consumers are very bleak. Unfortunately, they appear to be consistent with the trend seen in the latest unemployment insurance claims data from the U.S. Department of Labor. The latest report showed a sharp rise in the number of unemployment claims, from ~200,000 on March 7 to more than 3 million on March 21 after a long period of relative stability.

Important note: The self-reported percentage of consumers who lost jobs from our survey is higher than the ~2% implied by the March 21 unemployment claims, which is likely because our data also reflects consumers who lost one, but not all of their jobs.

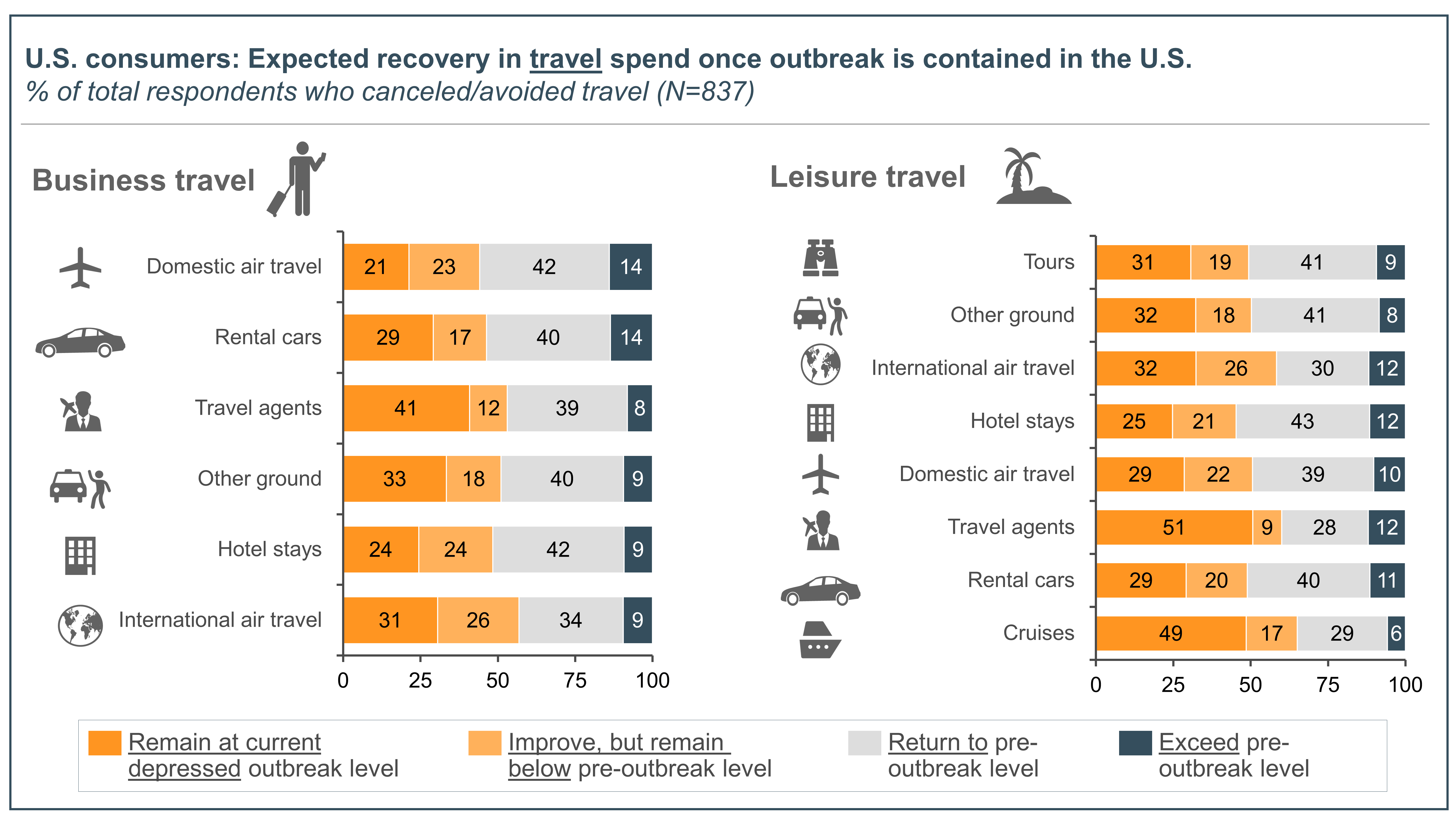

We asked consumers to imagine a future once the outbreak is contained. In that future, we asked them to estimate what “new normal” spending patterns might look like for travel categories.

Repeating some of the travel insights we shared last week, consumer outlook for travel spend post-outbreak is pessimistic. While 30%-40% of consumers expect travel spend to rebound to pre-outbreak levels, a greater portion of consumers expect spend to remain dampened even after the outbreak is contained. Only a small portion of consumers expect spend to exceed pre-outbreak levels once the virus is contained.

The pessimism expressed by consumers may be influenced by a high level of uncertainty regarding what the future holds, as well as a high volume of negative press coverage related to travel and transport.

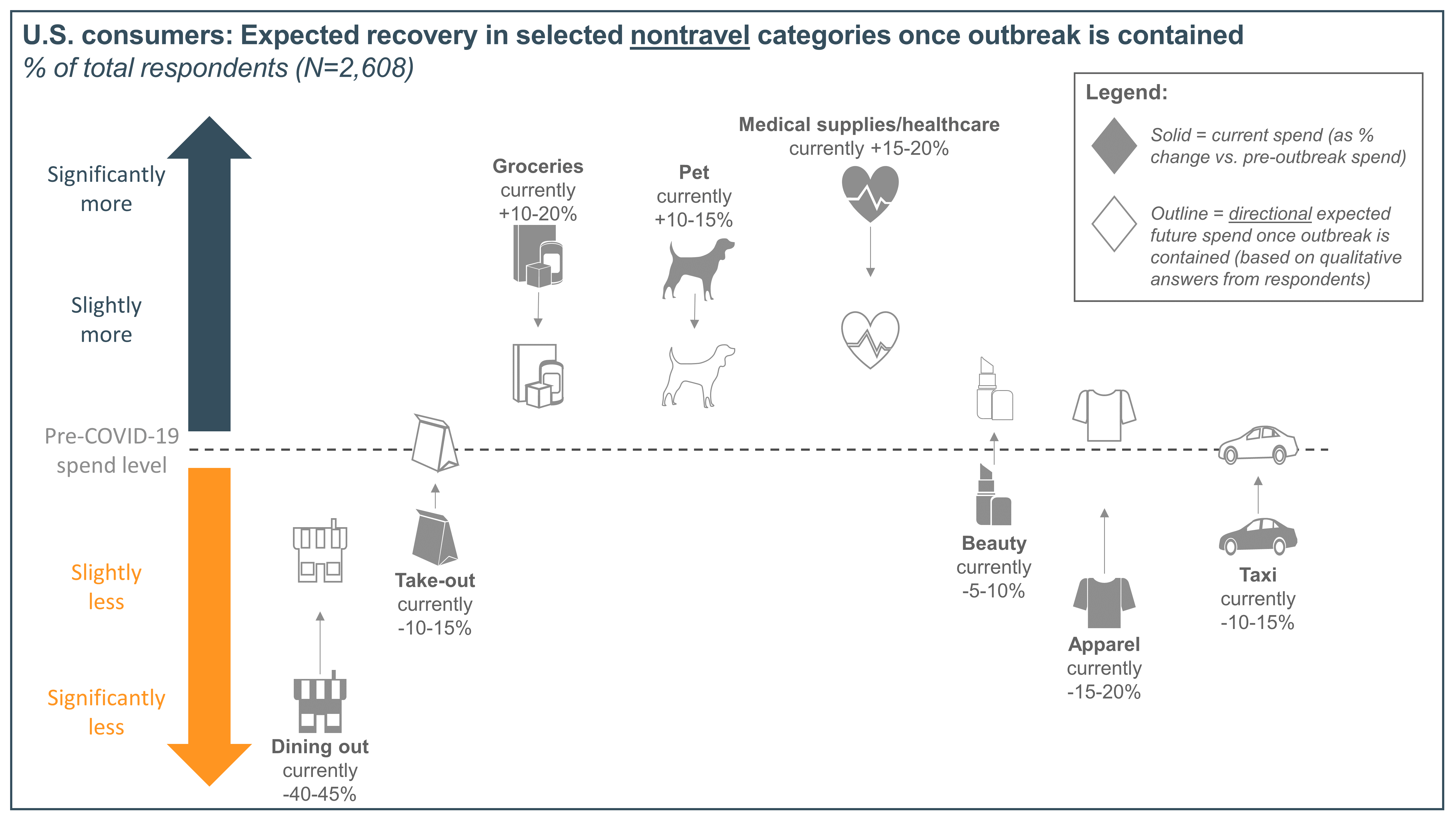

Dining habits may be impacted for some time even after the outbreak is contained

Consumers expect pet spend to exceed pre-outbreak levels

Consumers expect expenditure on both medicine/medical supplies and healthcare services to exceed pre-outbreak levels

Consumers expect spend on personal luxuries (e.g., fashion, beauty), which are dampened currently, to exceed pre-outbreak levels

Taxi/Uber/Lyft spend expected to return to pre-outbreak levels

Important note: All forward-looking data reflect consumer sentiments/expectations at this point in time and are not official L.E.K. Consulting forecasts.

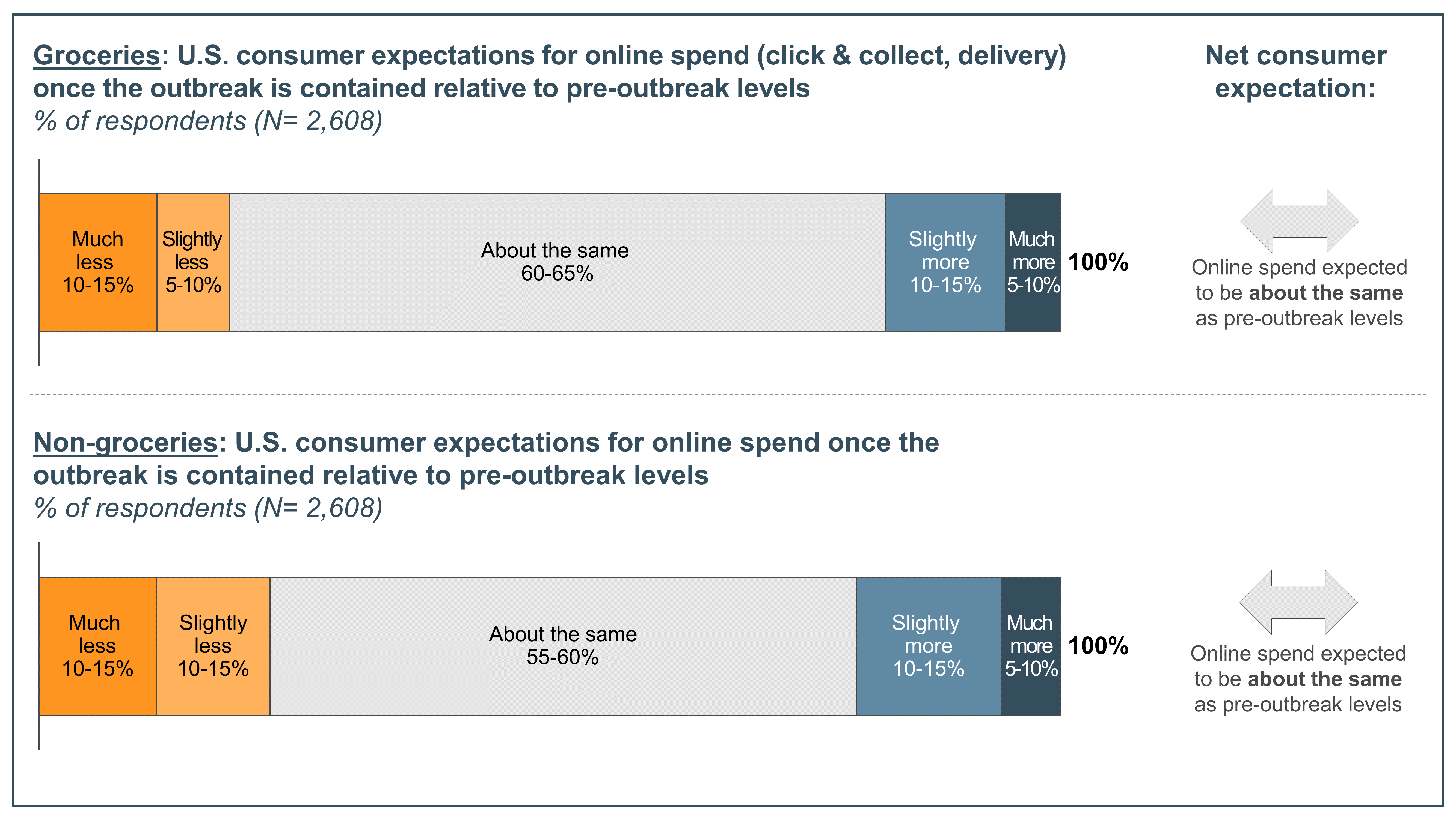

We asked consumers the degree to which they expect to shop online once the outbreak is contained relative to the degree to which they shopped online before the outbreak.

Most (~60%) consumers said they expect their online spend levels to return to what they were before the outbreak began. The remainder of consumers were split roughly evenly between spending more online and spending less online once the outbreak is contained. Net, these responses indicate that consumers expect online channel share for nontravel goods to remain largely unchanged by the COVID-19 crisis.

Although consumers feel this way, we can think of many potential reasons why online channel share could be positively impacted by this crisis, including:

Despite these hypotheses, the responses from consumers may reflect a desire to return to normal and return to much-missed in-store/outside-the-home experiences.