The backdrop: 2025’s tariff overhang and jittery consumers

Tariffs have certainly been at the center of business planning in 2025. With the stop-start dynamic of tariff policies, it has been hard to understand how much prices are actually changing at checkout.

Regardless, consumers have noticed. While prices have been steadily rising these past few months, the latest L.E.K. Consulting consumer sentiment pulse surveys highlight that consumers expect to shoulder the expected rise in costs, feel they are already paying more than they’d like and thus expect to tighten their budgets.

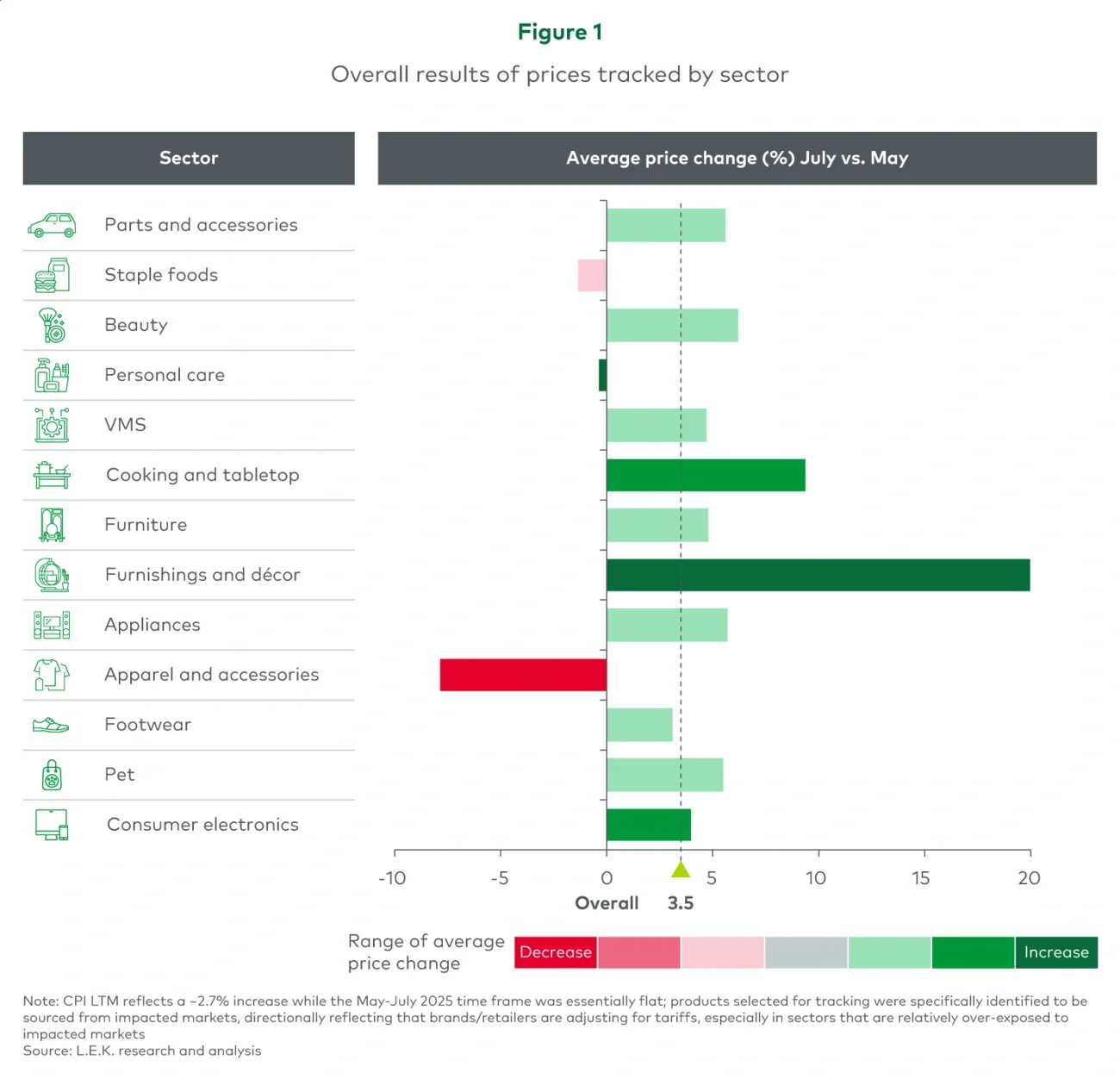

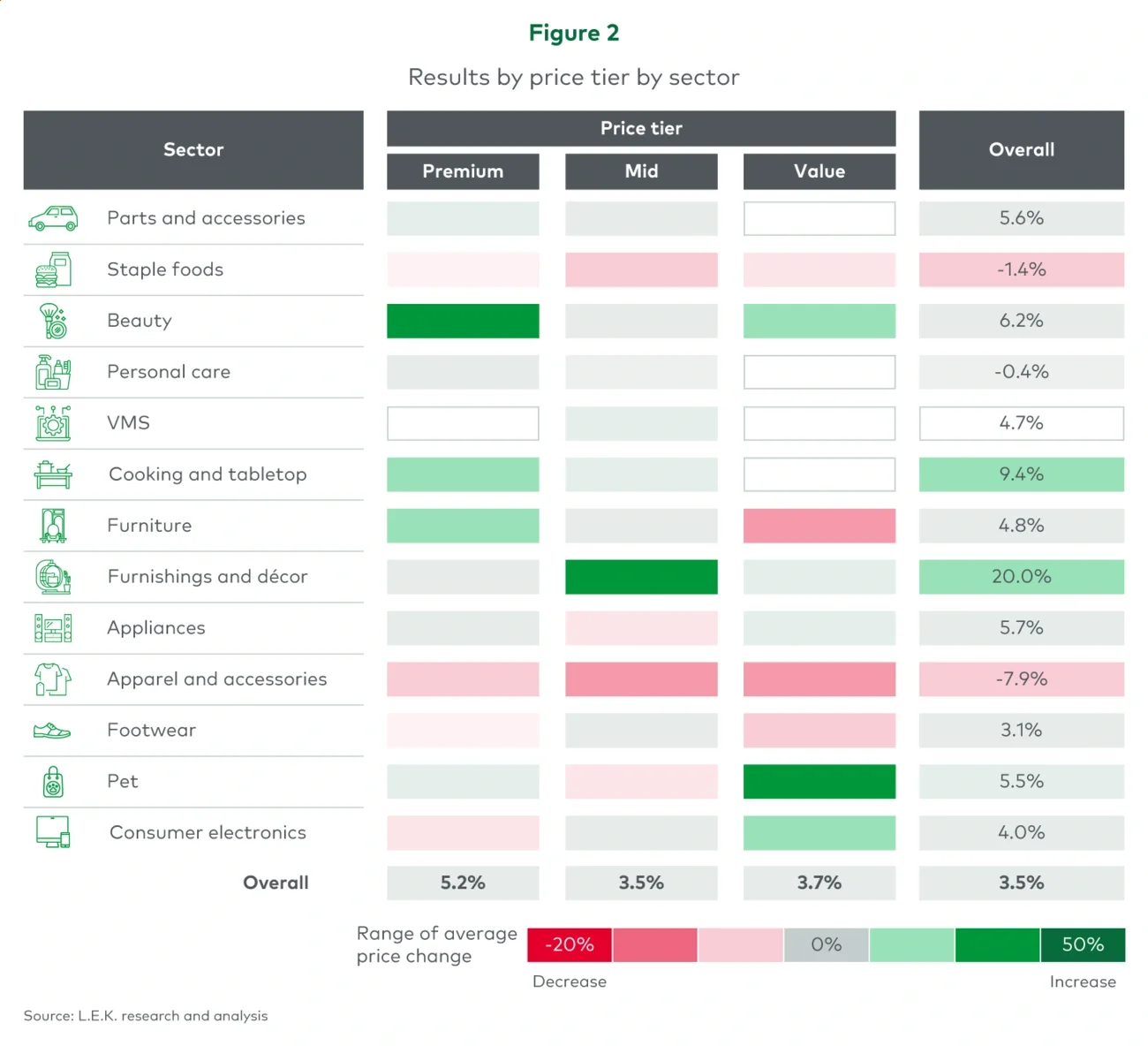

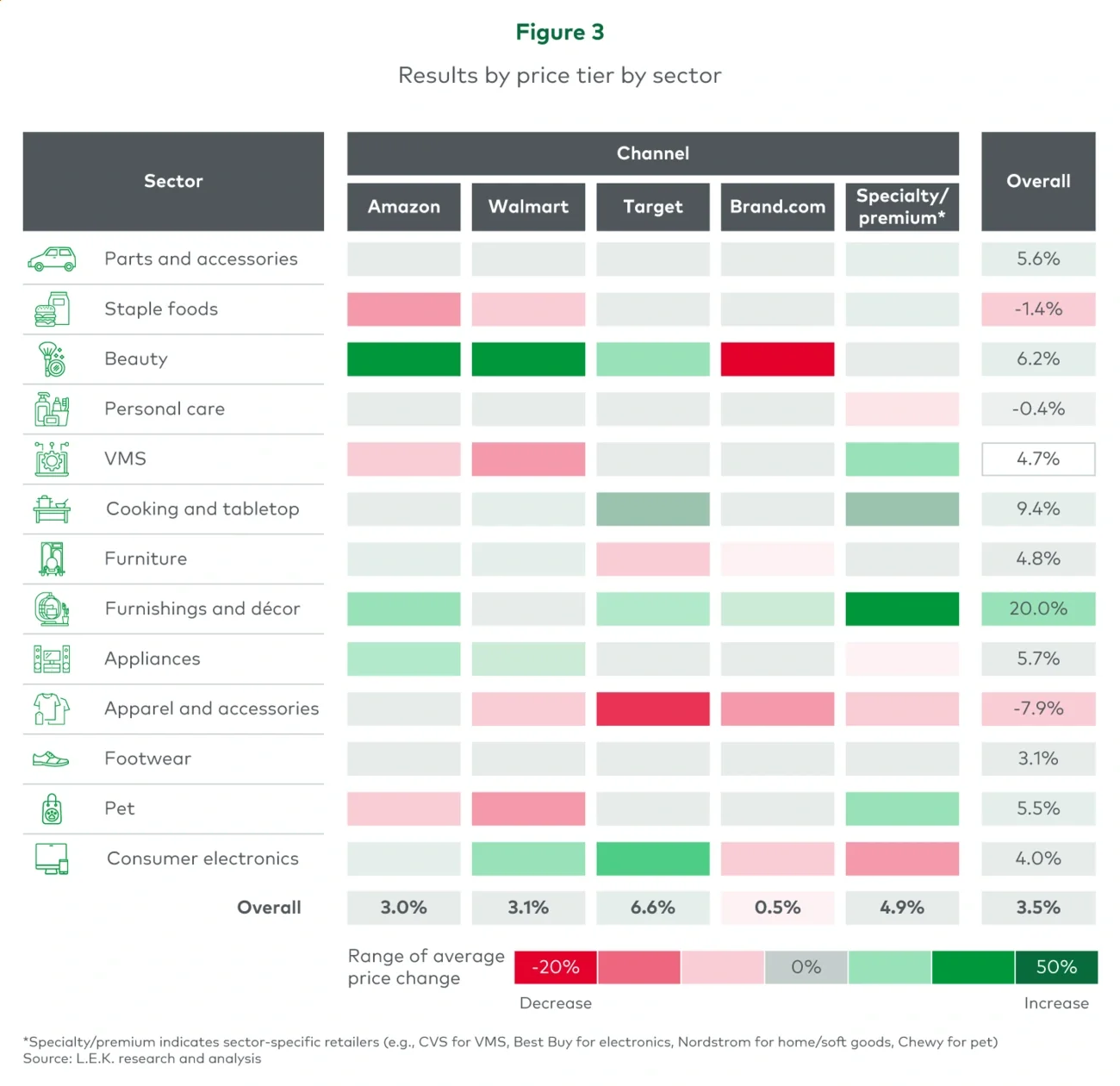

To further separate noise from signal, we tracked prices for approximately 300 stock-keeping units (SKUs) across six consumer sectors and about 130 retailers during that same time frame and found that net prices rose roughly 3.5% on tariff-exposed goods.

What we found: Prices did increase, but unevenly

The amplitude of price changes varied by category, price tier and channel (see Figure 1). Premium tiers and specialty channels did more of the “heavy lifting” on absolute price points; value channels emphasized stability. More specifically:

- Household essentials were steady (flat to slightly down) as retailers prioritized price image and trip loyalty in these aisles.

- Meanwhile, discretionary goods spiked, especially in home goods (e.g., cooking and tabletop) and beauty.

- Consumers feel it most in big-ticket discretionary categories such as household durables, where the highest share of respondents in our pulse surveys say they are now paying “above acceptable” levels. This was consistent with price-scraped findings.

- The apparel and accessories category is the price-cut outlier. We have seen in our consumer work that apparel is the key area where consumers will reduce spend in response to tariffs. That behavior is consistent with the market actually cutting average prices using more promotional activity as they work through pre-tariff inventory based on a likely higher level of demand.