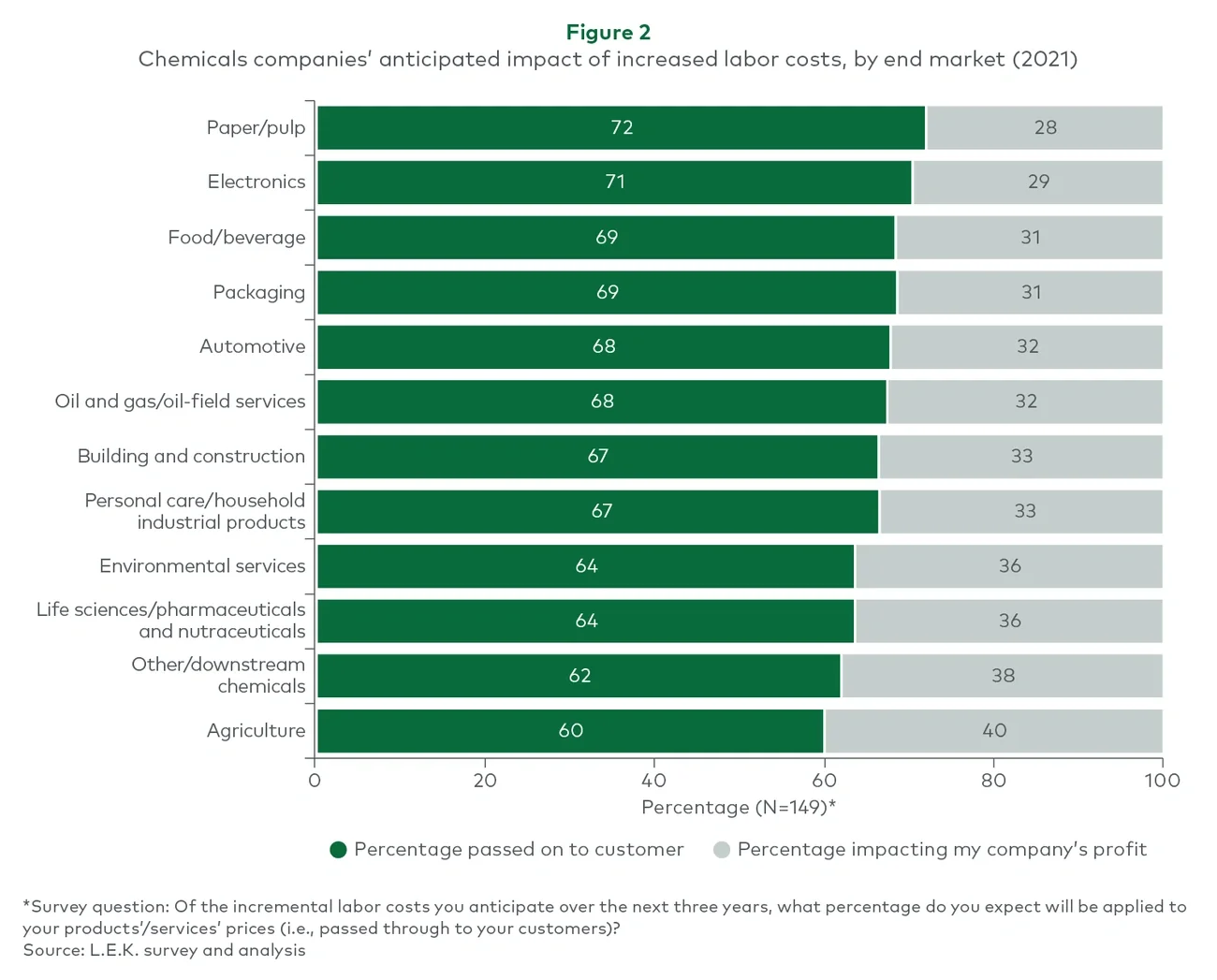

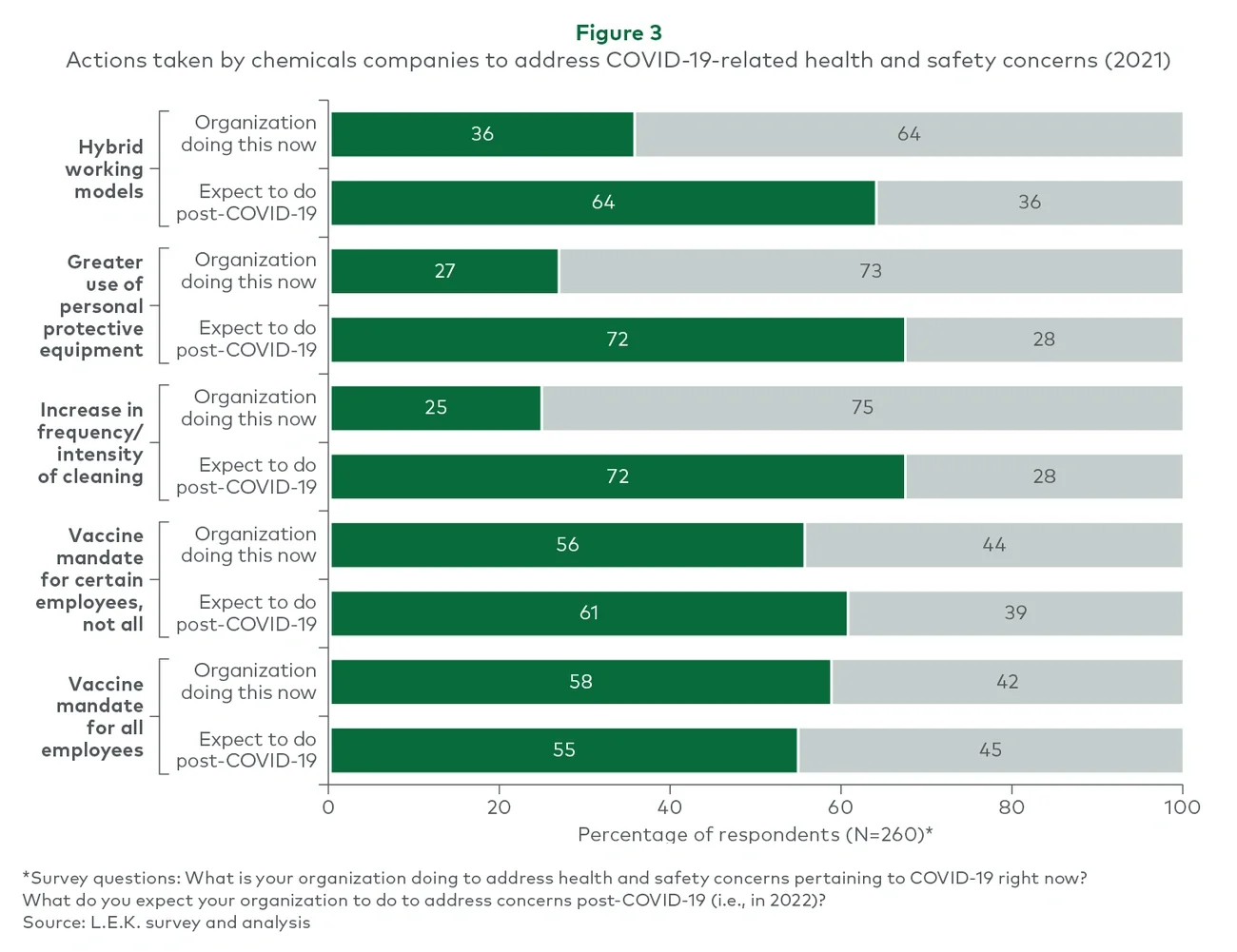

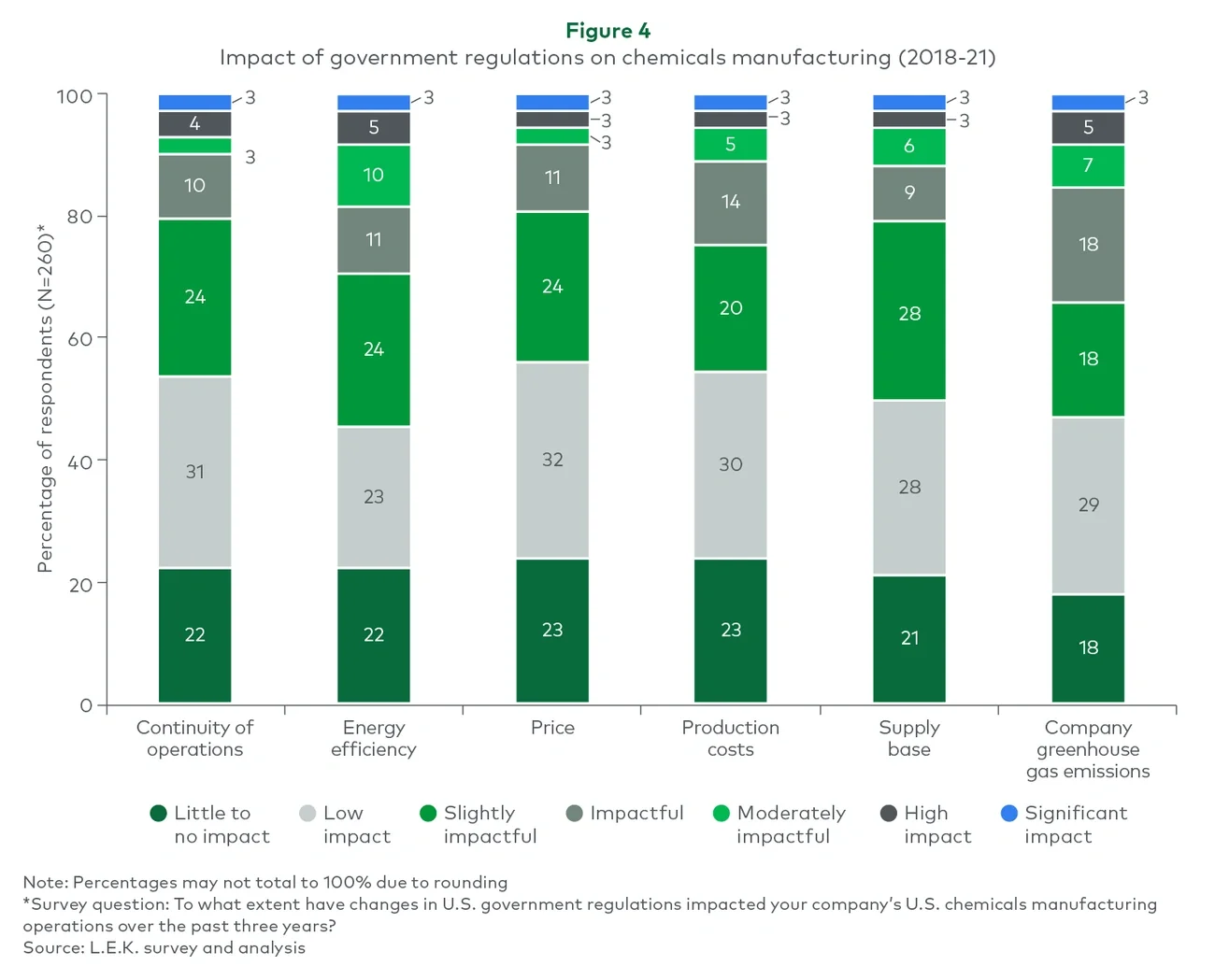

The past three years have been turbulent for the chemicals industry, and that turbulence is likely to continue. Most notably, the COVID-19 pandemic has disrupted supply chains and sparked labor shortages that continue to put pressure on operating costs. At the same time, global trade dynamics have driven rising production costs and margin pressure.

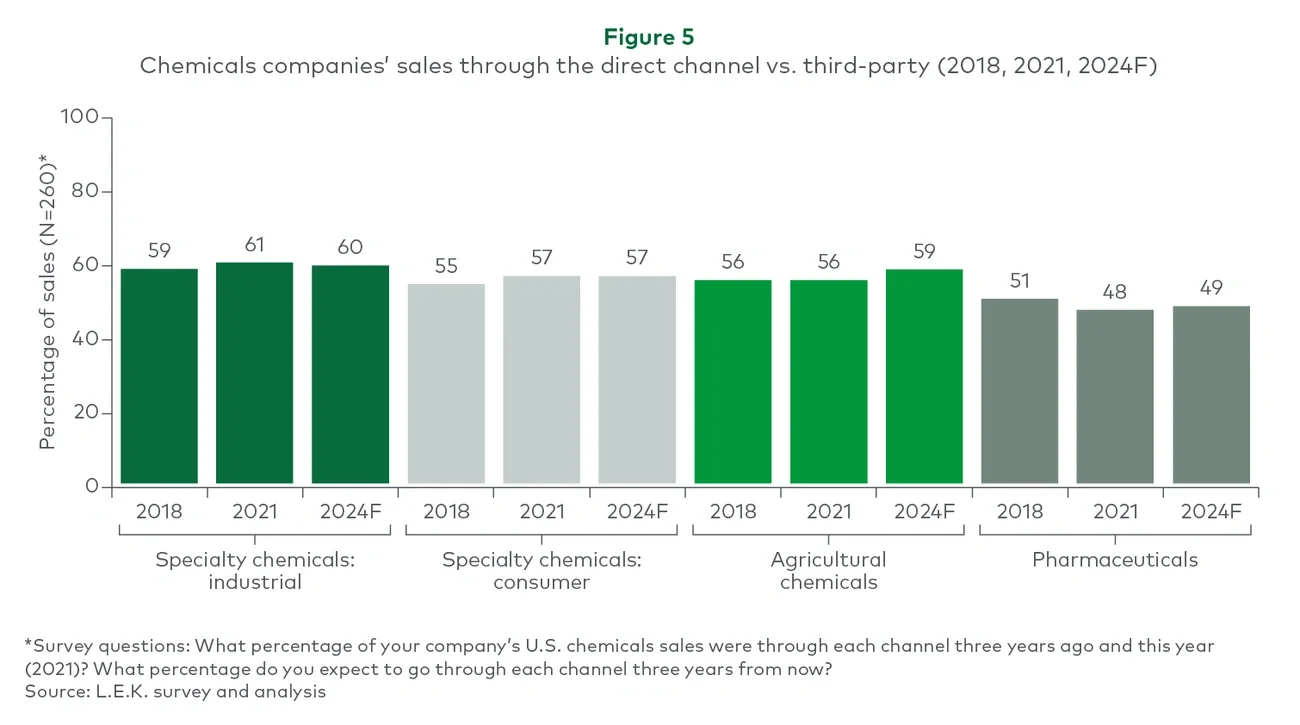

Industry professionals expect these disruptions to continue over the next three years. They anticipate ongoing pandemic-driven labor shortages and cost escalation, but they expect no changes in distribution channels, with third-party distribution predicted to remain 40%-50% of companies’ sales.

These are among the findings of L.E.K. Consulting’s first annual U.S. Specialty Chemicals Survey of 260 chemicals sector professionals across a broad range of industries and executive functions. The survey was conducted in late 2021. It reports on key issues impacting the industry such as supply chain, sustainability and digitization.

The added costs driven by COVID-19 labor trends and government regulation may lead to increased consolidation and vertical integration as organizations seek to maintain margins and streamline processes.

Our survey examined several disruptive forces that are all driving up prices. We discuss each in more depth below.

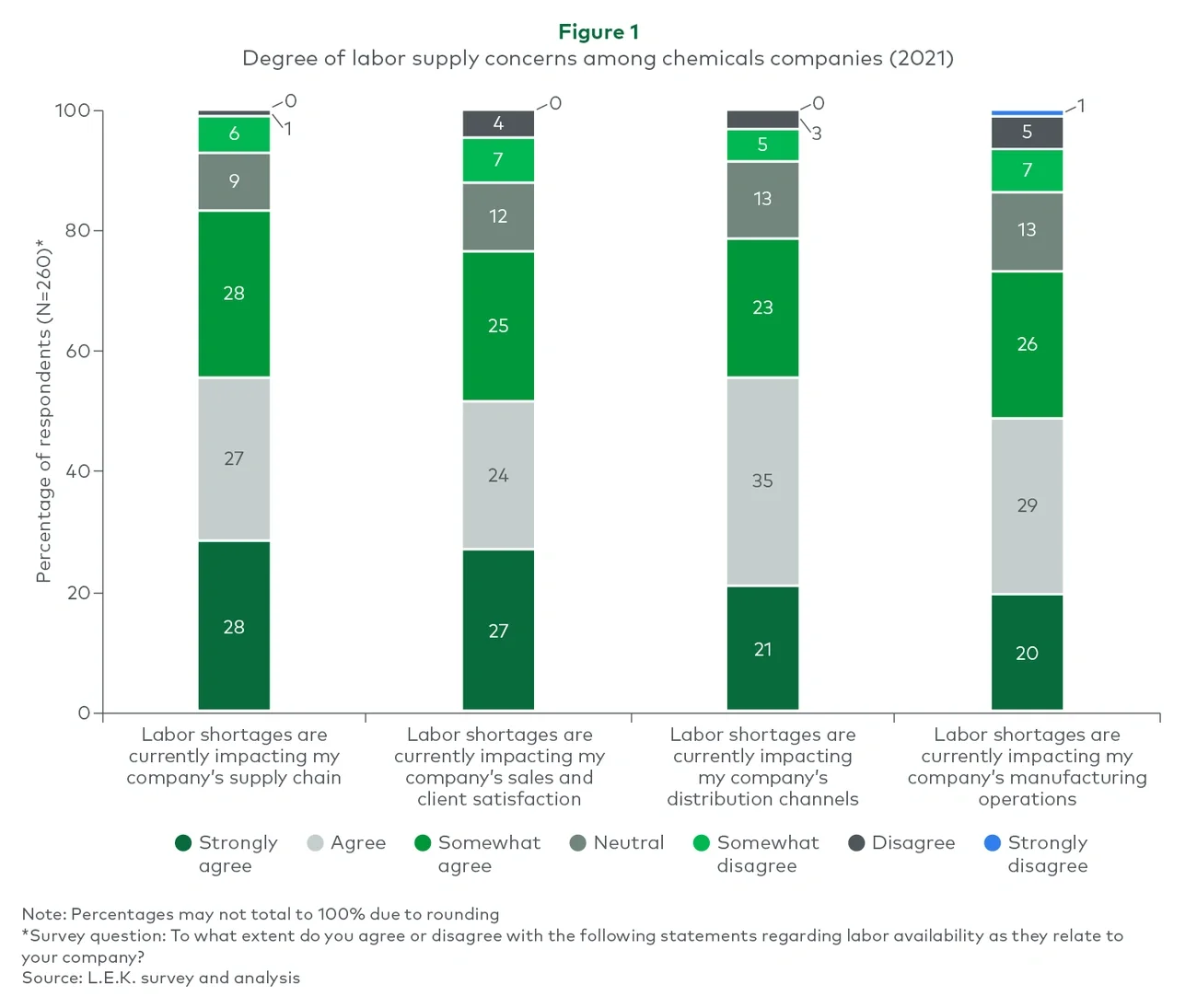

COVID-19’s impact on labor supply will outlast the pandemic

Among the major lasting effects of the COVID-19 pandemic is a significant labor shortage that is disrupting the entire chemicals industry. Approximately 80% of survey respondents indicate that labor shortages are impacting core areas of their business. Respondents strongly agree that labor shortages are affecting distribution (56%), the supply chain (55%), sales and client satisfaction (51%), and manufacturing operations (49%) (see Figure 1).