The environmental services sector, which rebounded strongly from the initial COVID-19-related slowdown, is poised for sustained growth going forward, powered by long-term tailwinds and the enactment of the Infrastructure Investment and Jobs Act. Meanwhile, against this backdrop, a labor shortage combined with supply chain bottlenecks will present both challenges and opportunities.

This outlook comes from a recent study conducted by L.E.K. Consulting to assess the environmental services market outlook. Based on a number of in-depth conversations with environmental services executives, we identified eight core trends that current and potential investors in the space should keep top of mind for the rest of 2022 and beyond:

- The environmental services sector has been relatively sheltered from the impact of COVID-19

- Long-term tailwinds, including heightened environmental consciousness and the push for environmental, social and governance (ESG) policies, are expected to continue to support sustained growth

- The infrastructure bill will add to the sector’s existing funding tailwinds over the next decade

- Labor shortages will likely persist against the backdrop of growth

- Demand, combined with labor-driven supply constraints, could lead to pricing and margin growth

- Strategic differentiators will include digitalization, automation and offshoring, as well as effective labor recruitment and retention

- Industry consolidation and M&A activity are expected to continue in many environmental services segments

- Identifying synergetic acquisition platforms remains a winning value-creation strategy

Taken together, these trends make environmental services an interesting and dynamic space in which to invest.

The environmental services sector has been relatively sheltered from the impact of COVID-19

Compared to many other sectors, environmental services have been broadly shielded from the impact of COVID-19. While Q2 2020 saw some delayed projects, these delays did not last very long given the “essential business” status of the industry and the desire from public and private sector customers to keep projects going. Some segments even saw business activity accelerate due to greater demand for indoor hygiene and related facility services. Overall, the negative effects of COVID-19 have proven to be quite temporary, while the positive impacts of the renewed focus on health and hygiene are expected to stay.

Long-term tailwinds are expected to continue to support sustained growth

Certain subsectors, such as restoration and specialty waste services, have gained further speed from long-term growth tailwinds during the COVID-19 pandemic, among them a broader push for ESG policies. And with post-COVID-19 normalization continuing to set in, the long-term outlook across all subsectors of environmental services is now positive.

The infrastructure bill will add to the sector’s existing funding tailwinds over the next decade

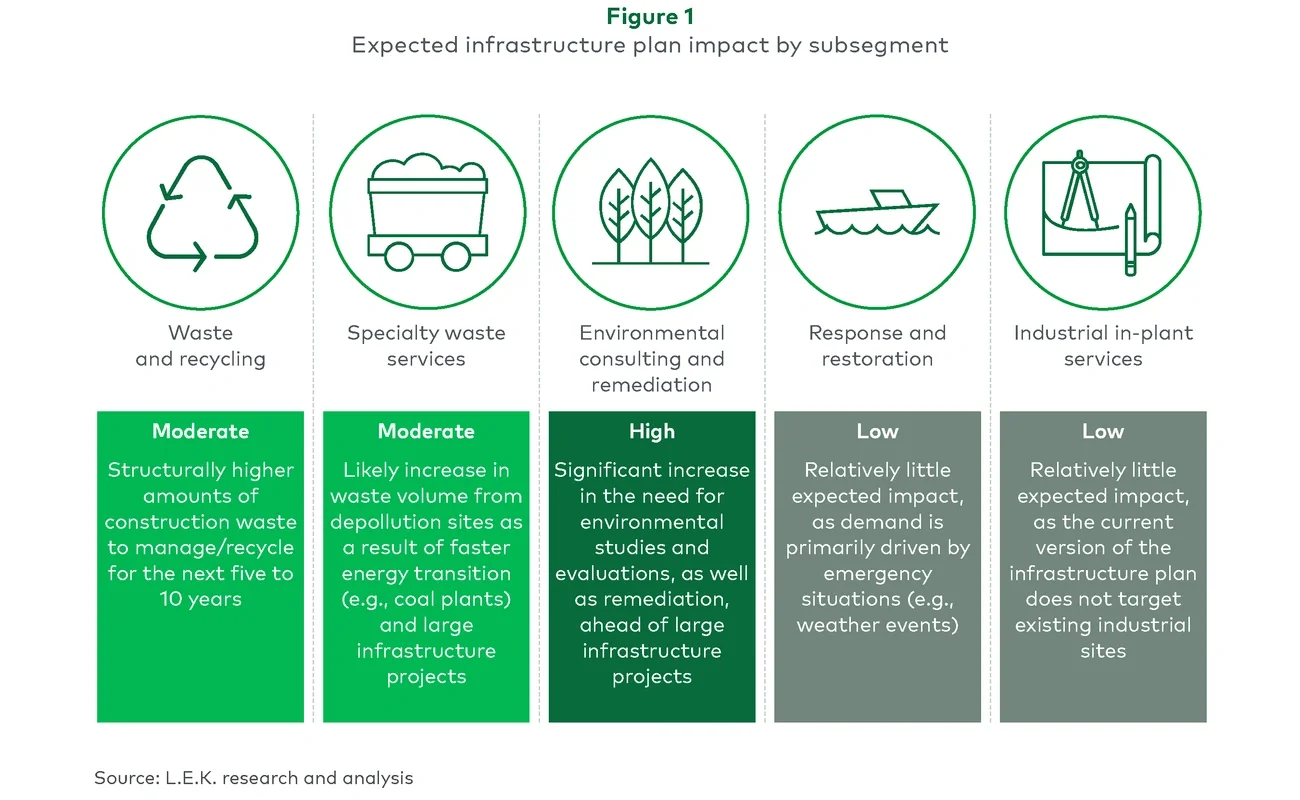

In November 2021, Congress passed the Infrastructure Investment and Jobs Act, which will add to the tailwinds already powering the sector by driving additional demand for a range of environmental services from abatement to remediation. As one restoration services senior executive put it, “If you combine the long-term tailwinds of the environmental services space and the expected impact of the infrastructure plan, you really get to a very optimistic picture.” Indeed, environmental consulting and remediation will be especially impacted by the $1.2 trillion bill (see Figure 1), which will provide the sector with a total of $1 billion to clean up more than four dozen toxic waste sites.