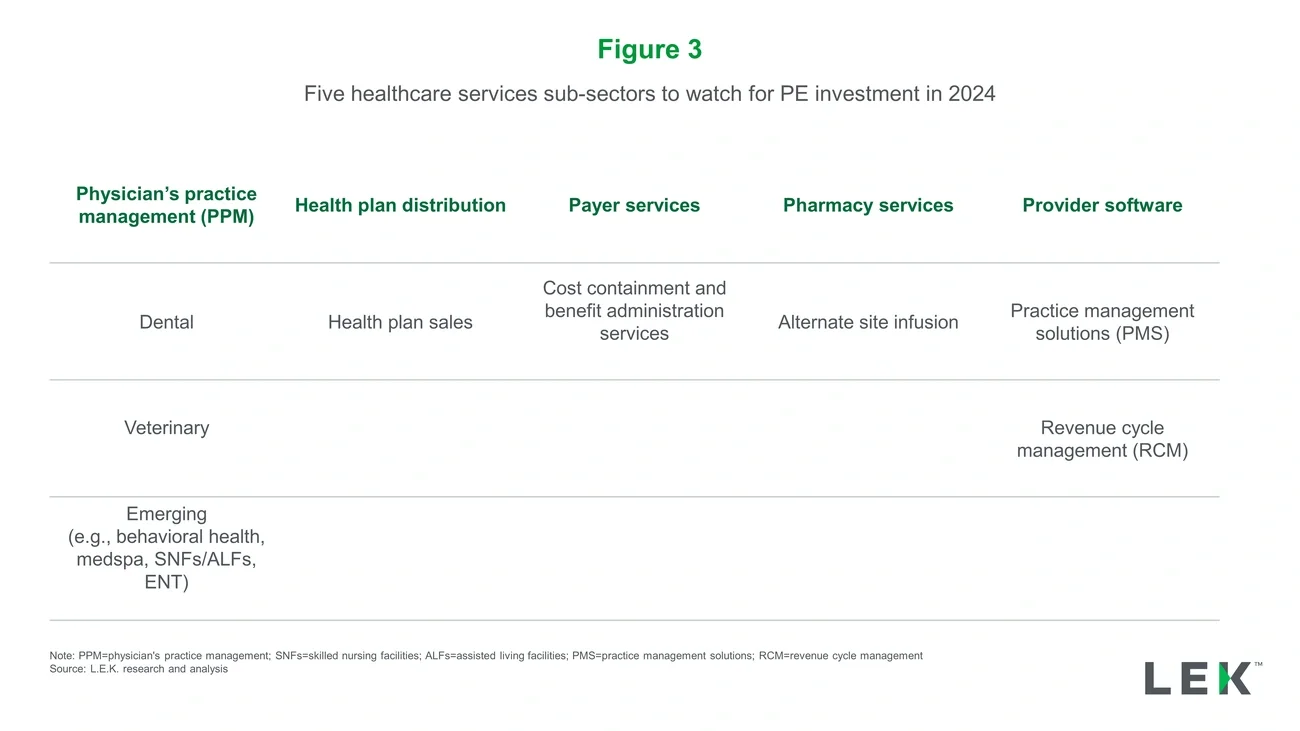

3. Payer services: An alcove for cost containment

Ever-escalating medical and pharmacy costs continue to place pressure on employer margins, heralding an increased focus on cost containment for self-insured employers. Third-party administrators are continuing to win share from traditional health insurers and are doing so through more innovative deployment of provider networks, use of cost containment solutions, navigation and care management solutions that when effectively combined help provide meaningful return on investment.

4. Infusion of innovation in pharmacy services

As the cost associated with specialty drugs continues to soar, payers are actively diverting patients into less-costly care settings like home or ambulatory infusion centers. The in-home and ambulatory infusion markets are enjoying double-digit growth rates and heightened patient satisfaction at a favorable cost to payers. This sector promises to be active in 2024 as a number of fast-growing platforms are expected to come to market.

5. Software elevation: PMS and RCM

Revenue cycle management (RCM) solutions respond to increasing complexities and costs in healthcare provision. Demand escalates for specialized, best-in-breed RCM tools, particularly for anesthesiology, orthopedic care and third-party claims, as well as home health and SNF settings.

Forward-looking insights

As the healthcare investment ecosystem evolves, so does the playbook for successful engagement. 2024 requires a strategic lens, one that sees value beyond conventional wisdom, focusing on subsectors where consolidated operations, technological advancement and innovative service models are shaping the future of healthcare.

The commitment to deep industry analysis that we bring to our partners remains resolute, as evidenced by sustained growth amid a contracting market. The sectors underlined here not only signify resilient investment pockets but also hubs for transformative healthcare service delivery — a golden opportunity for private equity practitioners and healthcare investors aiming to develop a legacy of impact and returns.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC