Key takeaways

-

The worldwide orphan drug market grew from $79 billion to $114 billion over the past five years and is expected to top $178 billion by 2020.

-

However, achieving commercial success in this space has become increasingly difficult and is not without risks, underscoring the need to understand the unique aspects of each orphan drug opportunity.

-

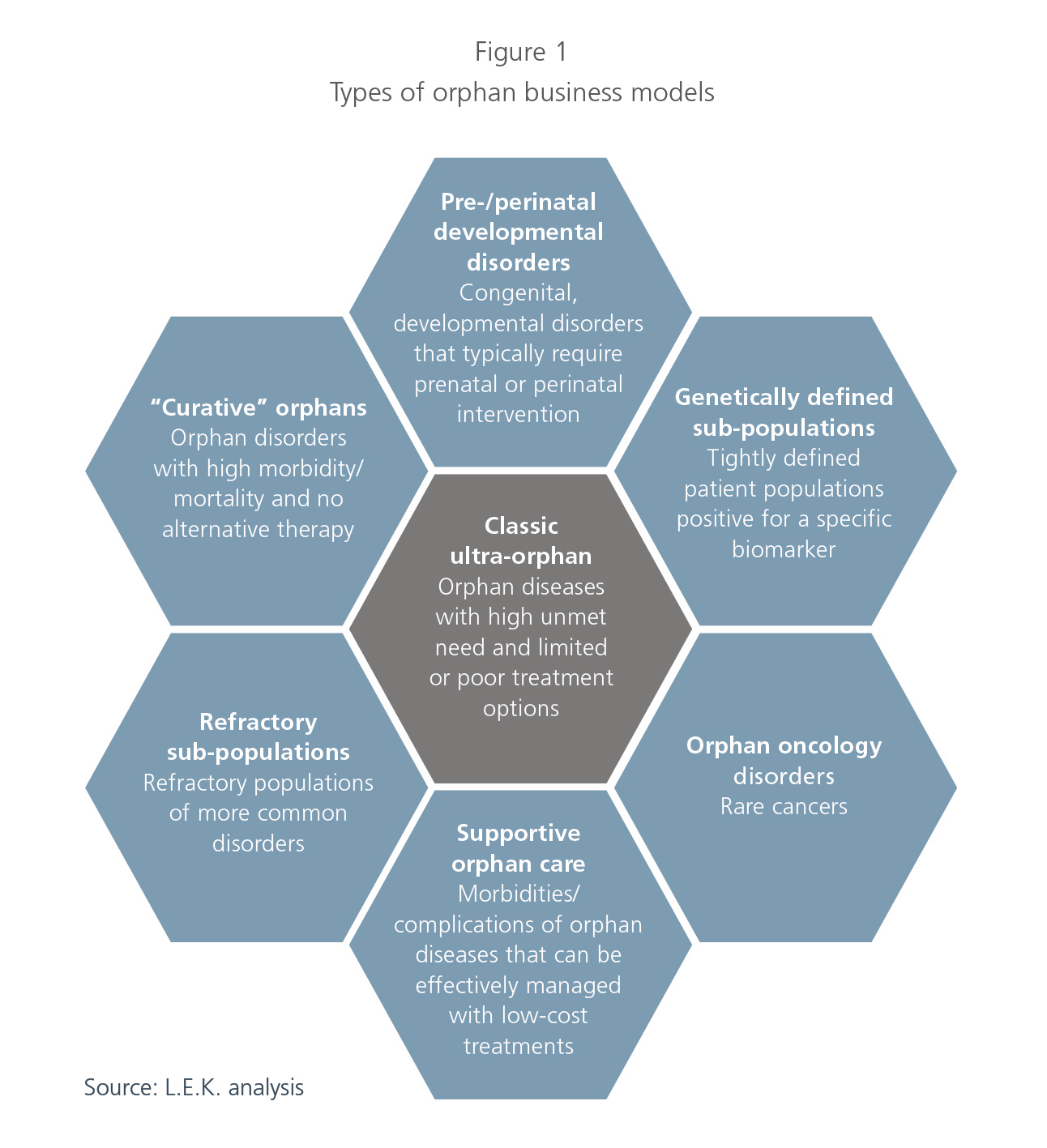

The orphan drug market, rather than being a one-size-fits-all homogeneous market, can be segmented into seven distinct business model archetypes.

-

Companies that have been most successful in the orphan drug market have tailored their approach to the unique needs of each sub-segment in the orphan disease landscape.

Orphan drugs are expected to play an increasingly prominent role in the biopharmaceutical industry. Driven by the promises of improving the prognosis for patients with serious and often life-threatening conditions and by high price points and limited competition, the worldwide orphan market grew at approximately 8% per year over the past five years (from $79 billion to $114 billion). This rise in orphan drug spend is likely to continue unabated, with analysts expecting the 2020 worldwide orphan drug market to top $178 billion.1

However, as we discussed in “Raising Orphans: How Pharma Can Capture Value While Treating Rare Diseases,” achieving commercial success in this space has become increasingly difficult. Despite attractive market attributes, many new entrants to the orphan space have experienced unexpected challenges in finding and executing the right commercial business model to support their products. For example, UniQure’s Glybera (the first European Medicines Agency–approved gene therapy in 2012), developed for familial lipoprotein lipase deficiency, failed to drive patient volumes due to its high cost ($1.3 million per dose) and significant reimbursement challenges. As a consequence, its marketing authorization was not renewed in 2017. Similarly, Pfizer’s Elelyso (approved in 2012 for type 1 Gaucher disease) has had a poor commercial performance (2016 worldwide net revenue of $48 million)2 due to the lack of differentiation from its competitors (Shire’s VPRIV and Genzyme’s Cerezyme).3 These difficulties underscore the need to understand the unique aspects of each orphan opportunity, as these in turn dictate the appropriate business model, including cash flow and risk implications, that biopharma companies must consider.

In this Executive Insights, we offer an L.E.K. Consulting viewpoint on how the orphan market is actually a collection of seven distinct business model archetypes that are driven by key disease, patient and market characteristics. It is our hope that by disaggregating and characterizing these business models and their key success factors/risks, we may enable readers to focus their corporate strategies to optimize the value and impact of their orphan therapies.

Seven distinct business models

The orphan drug market, rather than being a one-size-fits-all homogeneous market, can be segmented into distinct business model archetypes, each with its own particular set of challenges. When considering opportunities in the orphan space, players need to carefully evaluate the relevant archetype and optimize their strategies accordingly. Through our work with numerous clients in the space, we have identified the following orphan business model archetypes:

- Classic ultra-orphan

- Pre-/perinatal developmental disorders

- Genetically defined sub-populations

- Refractory sub-populations

- Orphan oncology disorders

- “Curative” orphans

- Supportive orphan care

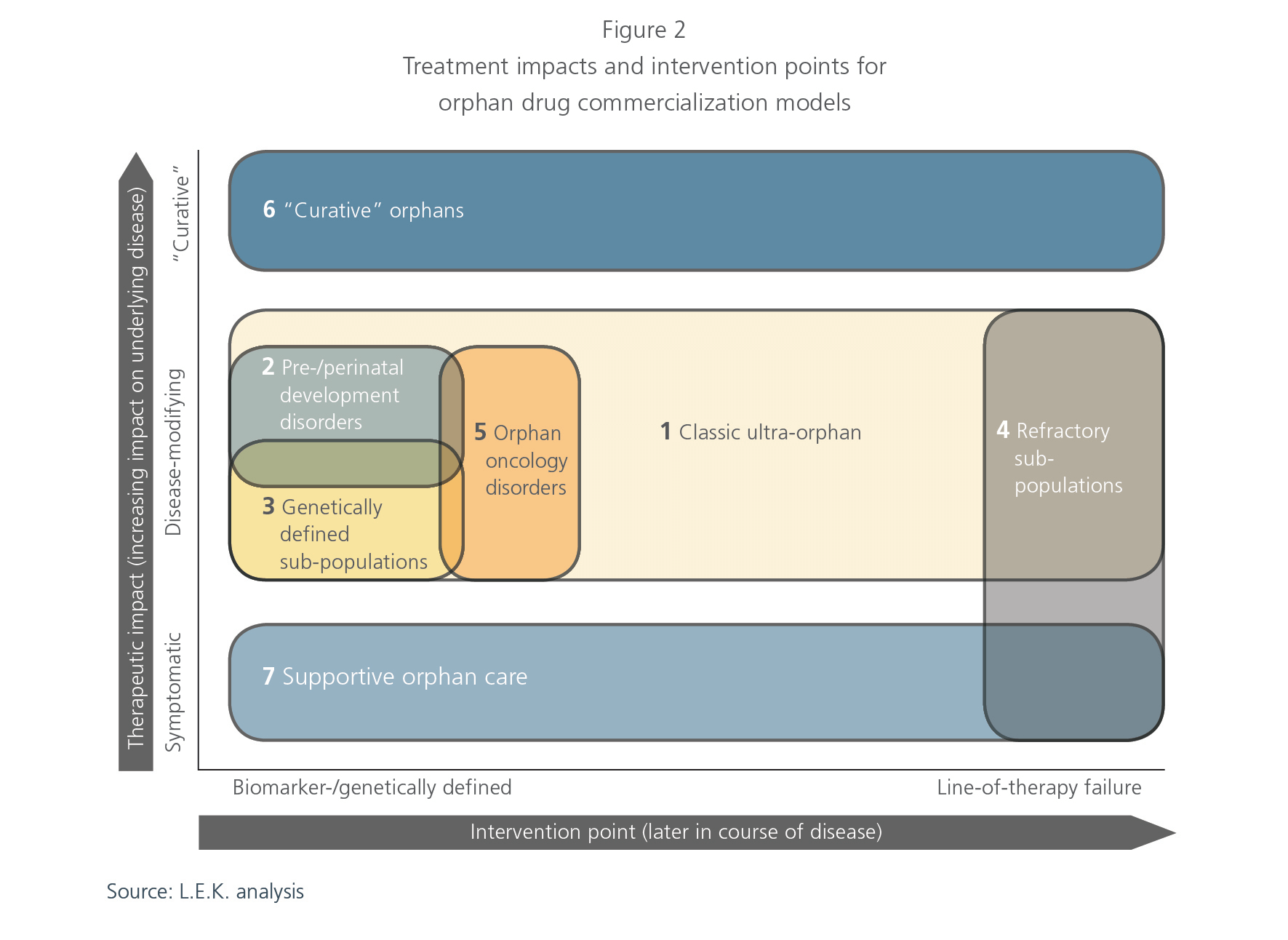

While these archetypes are defined by unique combinations of considerations, they are not necessarily mutually exclusive; a particular orphan disease/treatment could benefit from key aspects of more than one archetype. Thus, it is critical to deeply understand the value drivers related to a specific opportunity in order to tailor development and commercialization initiatives accordingly.

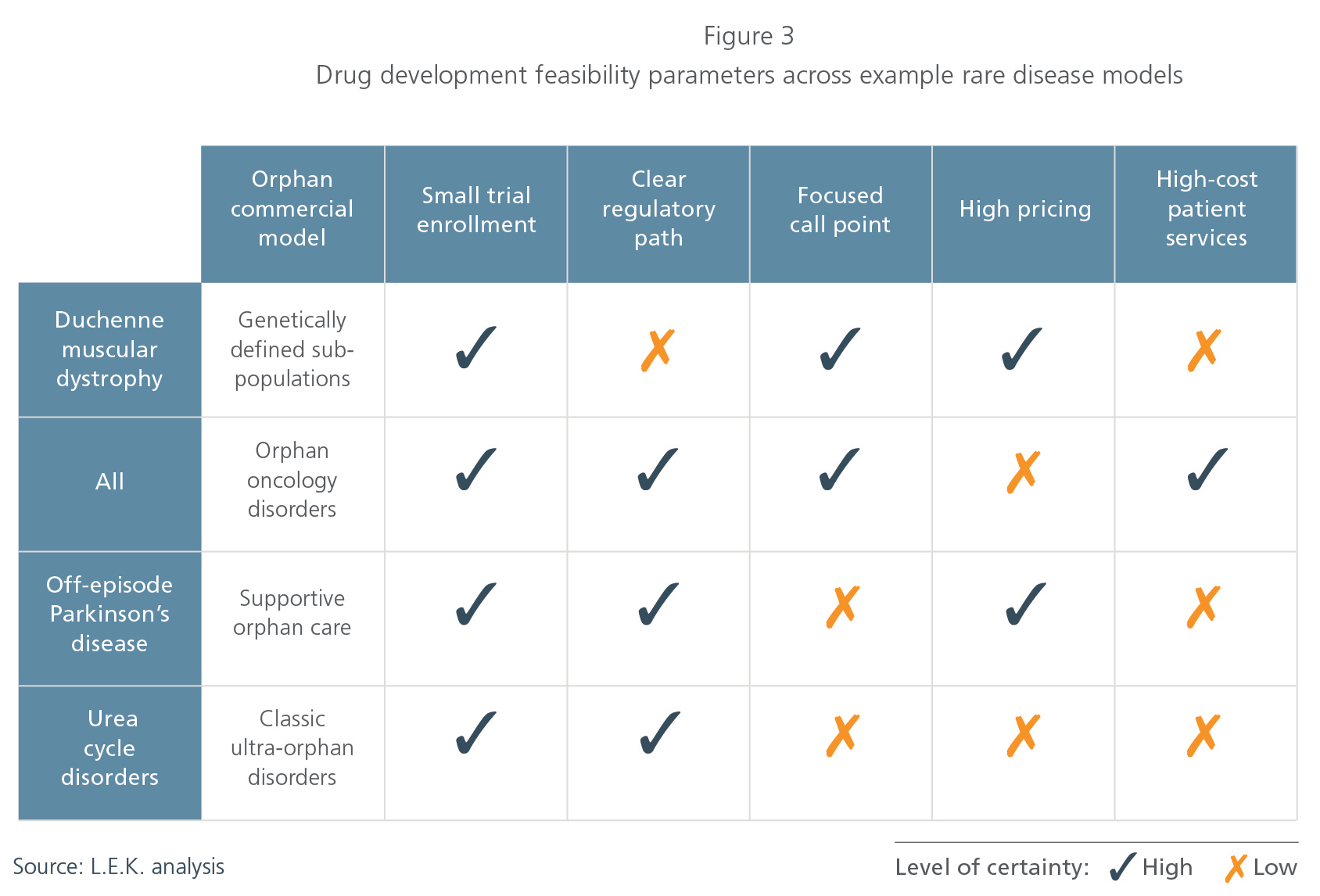

1. Classic ultra-orphan

The commercial model for classic ultra-orphan opportunities is what one typically envisions when thinking about the orphan drug space. This model, which was initiated by Genzyme in the 1980s, is mostly associated with conditions that have a prevalent population of less than 10,000 people in the U.S. (in the EU, a disease is considered to be ultra-orphan if prevalence is less than 1:50,000),4 significant morbidity or mortality resulting from lack of suitable treatment options, and genetic abnormalities resulting in absent or improperly functioning enzyme variants. For this reason, treatments have often consisted of enzyme replacement therapies that are priced at several hundred thousand dollars.

Given that classic ultra-orphan disorders are very rare and often lack treatment alternatives, the addressable population is not well-diagnosed or defined, especially during a product’s early stages of development. This puts a premium on development and commercial strategies that emphasize patient identification and retention. Successful companies have maximized their commercial opportunity through high-touch patient engagement strategies, often connecting with the patient community through channels outside of hospitals and/or treatment settings. For example, Sanofi/Genzyme has worked closely with the international patient communities to understand the epidemiology and treatment outcomes of Gaucher disease. Sanofi/Genzyme provided financial and organizational support for the creation of the Gaucher registry, which not only assisted in Ceredase’s/Cerezyme’s development, but also continues to engage the patient and physician community. This involvement had the combined effect of both patient identification and broad awareness-building for Ceredase/Cerezyme across physician and patient groups, positioning Genzyme as a leader in Gaucher care.5

The classic ultra-orphan archetype has provided a strong foundation for the orphan disease market. In addition to “high touch” patient services, players looking to succeed in this model should continue to emphasize patient identification and retention. This archetype has also established a precedent for high prices for therapies that benefit extremely small patient populations, a delicate balancing act that companies should continue to assess as these markets develop. While many orphan players owe much to the classic ultra-orphan model, as we will see, additional considerations will drive other orphan business model archetypes.

2. Pre-/perinatal development disorders

In contrast to the classic ultra-orphan archetype, companies focusing on pre-/perinatal conditions face a host of unique challenges given the affected patient population. There is no denying that ensuring the development and delivery of healthy babies is an area of great unmet need, but it is associated with a number of unique challenges, including:

- Identification of patients before symptoms arise; many

- diseases (e.g., hemochromatosis) can be terminal before birth or only manifest symptomatically after birth (e.g., hypophosphatasia, spinal muscular atrophy)6

- Measurement of impact on potentially longer-term developmental effects

- Ethical considerations in “experimenting” on in utero, neonatal or early-life subjects

- Defining an acceptable experimental and regulatory pathway, given the above considerations

As a result of these challenges, there are very few companies that illustrate how to play in this space. One such company is Alexion Pharmaceuticals, which won Food and Drug Administration (FDA) approval for Strensiq in 2015 with an indication to treat perinatal, infantile and juvenile-onset hypophosphatasia (HPP).

In the context of perinatal developmental disorders, which are challenging for the reasons listed above, Alexion benefited from several advantages, such as a robust diagnostic paradigm for HPP and the availability of established biomarkers associated with the disease’s pathogenesis that helped to identify the target population. Additionally, Strensiq delivered key value propositions on ease of use and impact on survival.

Nevertheless, given the challenges commonly associated with treating perinatal diseases, it is no surprise that there are so few companies pursuing orphan drugs for pre- and perinatal conditions. Bucking this trend will require products that have a pristine safety profile, potentially creative regulatory paths and strong collaboration with relevant constituents.

3. Genetically defined sub-populations

The advent of precision medicine has facilitated the ability to optimize patient care by matching patients to treatments that address a specific underlying pathophysiology. It is not uncommon today for genetic testing to be used to diagnose patients with a particular disease and to identify a therapy that is “designed” for that specific abnormality.

The role of precision medicine in oncology, where it has allowed for the definition of genetically defined sub-populations, is relatively well-known. Key products such as Lynparza, Xalkori and Zykadia are indicated for patients with mutations in the BRCA (ovarian cancer) and ALK (non-small cell lung cancer) genes. However, we are seeing this dynamic play out in orphan diseases as well. For example, the use of Exondys 51 for Duchenne muscular dystrophy (DMD) is limited to the approximately 13% of DMD patients who have a mutation in exon 51 of the dystrophin gene. Similarly, Kalydeco and Orkambi are restricted to a number of mutations that account for approximately 5% (G551D) and approximately 50% (homozygous F508del), respectively, of cystic fibrosis patients.

In addition to the limited market potential associated with restricting a given indication to a genetically defined sub-population, the need for genetic testing introduces a number of leakage points that challenge value capture. First, it is critical to develop a test perceived to be necessary by physicians in consideration of competing alternatives. In addition, such a test needs to be reimbursed, or its adoption will likely be limited. Furthermore, the appropriate institutions (e.g., centers of excellence) need to incorporate the test/sample processing within their patient care protocols and may require training on the logistics related to the use and interpretation of the test. In order to address these challenges, companies typically partner with experts in companion diagnostics (e.g., Sarepta Therapeutics and Flagship Biosciences for Exondys 51, as well as various orphan oncology drugs with companion diagnostic devices) that provide both the technical expertise to develop the test and the commercial infrastructure to drive its adoption.

It should be noted that despite the challenges associated with pursuing genetically defined sub-populations in rare diseases, this archetype is associated with a favorable regulatory pathway, a potentially higher clinical impact on the relevant patient segments and favorable market access, given potentially lower-budget impacts.

4. Refractory sub-populations

Unlike classic ultra-orphan diseases, refractory sub-populations represent advanced, relapsed or severe subsets of patients of a particular disease. There are a number of advantages related to focusing on refractory sub-populations, including readily identifiable patients and the potential for relatively high price points given the focus on smaller, difficult-to-treat patient populations.

A key example of a therapeutic targeting this class of indications is Horizon Pharma’s Krystexxa (pegloticase), which was approved in 2010 to treat patients with chronic gout who are refractory to standard-of-care xanthine oxidase inhibitors (e.g., allopurinol, febuxostat). While diagnosed cases of gout have been estimated at approximately 2.13% of the U.S. population (approximately 4.8 million people), chronic refractory gout has an estimated prevalent population of approximately 50,000 in the United States. In these patients, treatment with the standard of care failed to normalize serum uric acid levels, the main contributor to chronic gout and associated complications (e.g., tophi deposits and kidney stones).

The pricing differences between a frontline branded gout therapy and Krystexxa illustrate the pricing power granted to a therapeutic targeting refractory sub-populations with orphan rarity. The annual cost of therapy for Uloric (febuxostat) is approximately $3,700 (approximately $10 per tablet), while the annual cost of therapy for Zyloprim (allopurinol) is approximately $3,000 (assuming a dosage of 600mg per day). In contrast, the wholesale acquisition cost per month of Krystexxa can be approximately $40,000, and patients typically have one course of therapy that ranges anywhere from less than a month to six months.7

While regulatory pathways can be clearly defined for treatments for refractory sub-populations, finding patients in time to make a demonstrable clinical impact can be difficult. There are also challenges that are unique to addressing this class of indications, perhaps most important of which may be that orphan status is dependent on a sub-population of refractory patients within the broader disease. Additionally, there exists the possibility of competitors in development that could enter at an earlier line of therapy and reduce the rate at which patients become refractory to care.

5. Orphan oncology disorders

Orphan indications in oncology have developed into attractive targets for drug companies, as substantial opportunities can be found in small cancer types or in later lines of therapy for metastatic cancers where the populations are relatively small and the unmet needs significant. Unlike with other rare diseases, healthcare professionals may be more adept at diagnosing and treating orphan oncology disorders, resulting in patients who are easier to identify, as they are well-tracked by a large dedicated network of cancer hospitals and government databases. Considerable amounts of funding in cancer research have also led to well-established therapeutic targets. However, there are a few challenges to consider when focusing on orphan oncology compared with classic orphan diseases.

There are usually broad-spectrum standard-of-care approaches (albeit with potentially poor patient outcomes) for any cancer, whereas classic ultra-orphan diseases usually lack a standard of care. Moreover, while there is a clear regulatory pathway for orphan oncology drugs, cancer drug trial designs have increased in complexity and duration given the degree of competition in the marketplace. Furthermore, because patient populations are small, the abundance of clinical trials draws a meaningful number of patients out of the treatable pool, limiting revenue potential for approved drugs. For example, approximately 10%-20% of metastatic cancer patients are enrolled in checkpoint inhibitor clinical trials.

While a large, well-established cancer network of hospitals is beneficial, another challenge comes from a commercial and marketing perspective, as there is the potential need for a greater sales force. A larger, more broadly distributed network of cancer centers throughout the country usually results in approximately 100-200 sales representatives for many oncology drugs. This is compared with a more limited number of centers of excellence for an ultra-orphan disease, which may only require approximately 20-30 representatives.

Finally, challenges exist in pricing. While high pricing potential can be considered with orphan oncology drugs, there needs to be awareness of the impact of combination therapies on the total price of treatment, as multiple high-priced drugs can result in a prohibitively high total cost of care. For example, Lynparza (a PARP inhibitor) is a high-priced orphan oncology drug (approximately $15,000 per month) that can be used in combination with other cancer drugs such as PD1/L1s like Imfinzi (approximately $12,000 per month), thereby raising treatment costs to potentially unsustainable levels (approximately $25,000-$30,000 per month).8 Other treatment paradigms, such as those for multiple myeloma, have introduced combination therapies in which targeted agents, such as Revlimid and Velcade, are dosed together with steroids to substantially improve patient outcomes.9 Currently, triple-stacked therapies have evolved into the standard of care, and the introduction of other novel drug classes such as daratumumab (Anti-CD38) have driven clinical trials with combinations of agents. However, there is concern that these combination therapies result in exceedingly high prices that can lead to downward pricing pressures from payers as orphan oncology expenditures become a larger portion of healthcare expenses.

6. “Curative” orphans

Given recent technological improvements associated with cell and gene therapy, we are seeing orphan products surpass disease modification and venture into effectively “curing” a condition. Two examples of “curative” orphan drugs are GSK’s Strimvelis for severe combined immune deficiency “bubble boy” disease and BioMarin’s BMN-27010 for hemophilia A. Both treatments offer a solution to rid patients of all symptomatology by addressing the underlying pathophysiology of the disease with a potentially permanent approach.

Key challenges faced by the developers of “curative” orphan products include limiting off-target effects, demonstrating longterm therapeutic value, and engaging in novel payment and reimbursement models. Because many “curative” treatments are mechanistically novel and are expected to permanently alter the patient’s genetic or cellular physiology, long-term off-target effects may have serious and currently unknown consequences. Furthermore, while a functional cure may be obtained with a given “curative” therapy, the duration of the cure is not currently known. This may have implications for long-term cost savings for payers if additional doses or boosters are needed years after the initial treatment. While “curative” treatments have the potential to replace a lifetime of care, this undoubtedly introduces uncertainty that exacerbates the misalignment between developers and payers. Thus, payment models with high upfront costs may be unattractive to payers due to lingering uncertainty regarding the long-term savings in chronic care, in addition to the substantial practical impact these costs would have on annual budgets.11 Alternative payment or reimbursement models, such as annuities, which would allow payers to spread out the treatment cost over several years, may enable “curative” orphan products to receive greater access and reimbursement.

7. Supportive orphan care

While many pharmaceutical companies tend to associate orphan designations with disease-modifying therapies, opportunities also exist within target patient populations that require symptomatic support for an orphan disease. Many therapies have been able to achieve orphan designation by treating symptomatic morbidities or complications associated with orphan diseases, though they do not incorporate the high degree of patient centricity that is typically associated with orphan diseases (e.g., Gaucher).

The supportive orphan care commercial business model resembles the specialty pharma business model, particularly in the sense that prices for supportive orphan drugs are more in line with those of specialty pharma products, and have lower pricing potential than typical disease-modifying orphan drugs. This can be a key challenge for supportive orphan care products. While their prices are lower than those of typical orphan drugs, they are still managing a disease with low prevalence, and may find it difficult to compensate for their small patient population with high drug prices. For example, Lundbeck’s Onfi (for the adjunctive treatment of seizures associated with Lennox-Gastaut syndrome) and Sigma-Tau Pharma’s Cystaran (for treatment of corneal cystine crystals in cystinosis patients) were approved with orphan designation in 2011 and 2012, respectively.12 They were both priced lower than typical orphan drugs, with Onfi available at a price of $3,000 per month and Cystaran available at a price of $500 to $1,000 per month. Furthermore, a distributed patient population may require a larger commercial footprint and a larger overall investment from the company.

Companies should carefully consider the potential commercial challenges of supportive orphan care products, given the small prevalence and distributed population inherent to orphan diseases, before investing in symptomatic orphan opportunities.

Synthesis and implications

Successfully entering the orphan disease market requires a clear understanding of the applicable business models required for each potential indication and each development program being pursued. There is no one-size-fits-all clinical or commercial strategy for orphan drug development and commercialization, and the challenges and key success factors must be assessed against a company’s internal capabilities and culture. A firm must be thoughtful in choosing which strategy to pursue in the orphan market, and in considering the skills and competencies that will be needed to successfully execute this strategy. Much as it has with the specialty and oncology markets, the bar will likely continue to rise for new therapeutics in this class as the orphan market matures and its share of drug spend increases and attracts more payer attention and scrutiny.13 While the orphan market continues to be an attractive growth area for many drug developers, it is not without risks. Those companies that have been most successful have tailored their approach to the unique needs of each sub-segment in the orphan disease landscape.

Editor’s note: This article was first published in Life Science Leader.

1EvaluatePharma Orphan Drug Report, October 2015

2EvaluatePharma (includes worldwide Elelyso revenue except Brazil)

3FierceBiotech, Reuters

4Orphanet Journal of Rare Diseases

5Company press releases

6National Organization for Rare Disorders (rarediseases.org)

7Price Rx

8Price Rx

9Leukemia Supplements (Nature)

10There are other curative hemophilia “cures” in development

11Nature Biotechnology

12FDA

13FiercePharma

11082019151140