Sustainability1 is more important than ever. In just the past few months, we’ve seen growing political commitments to net zero, stricter developments in corporate sustainability reporting and a general acceleration of businesses’ sustainability plans.

Investing has exploded. Capital inflows to sustainable funds, the number of financial institutions committing to low-carbon investment and the value of sustainability funds launched are all at record levels. In part, this is due to a long-term evolution in investor attitudes and behaviours. ESG is also more important to society at large, particularly climate-conscious younger generations, and women — who are twice as likely as men to say it is ‘extremely important’ that their investment portfolio considers ESG factors. On top of this long-term trend, the coronavirus pandemic has further accelerated awareness of ESG in investing.

But there is still no clear definition of what ‘sustainable investing’ means, and the market has attracted a lot of negativity. We’ve seen greater scrutiny of what sustainable funds invest in, growing scepticism about those with potentially harmful products like tobacco and sugary drinks, increasing controversy over the definition of ‘net zero’ and ‘creative carbon accounting’ (such as a high-profile debate over Mark Carney’s Brookfield claims), and even a US Securities and Exchange Commission (SEC) warning over ‘misleading’ claims by ESG fund managers.

There has been particular confusion in the private markets. While 63% of UK private equity (PE) firms now take ESG principles into account in their investments, lower reporting requirements and accountability compared to the public markets has meant a wider variety of sustainability strategies and higher scepticism about their impact. As one report sums up, most PE ESG approaches are “nascent and superficial”.

Our experience resonates with these issues. Since the pandemic struck, we have spoken to over 100 corporates, investors and experts on sustainability. We’ve learnt that there is a lack of consistency in how sustainability is defined, measured and reported, and many organisations are unsure how to pursue a strategy that maximises value for investors, investees and society at large — and takes far greater responsibility for the planet.

In this article, we aim to help PE investors as they approach ESG. We explain key elements of the sustainable investment landscape, share our core observations on future developments and highlight recommendations for a way forward.

Types of sustainable investing

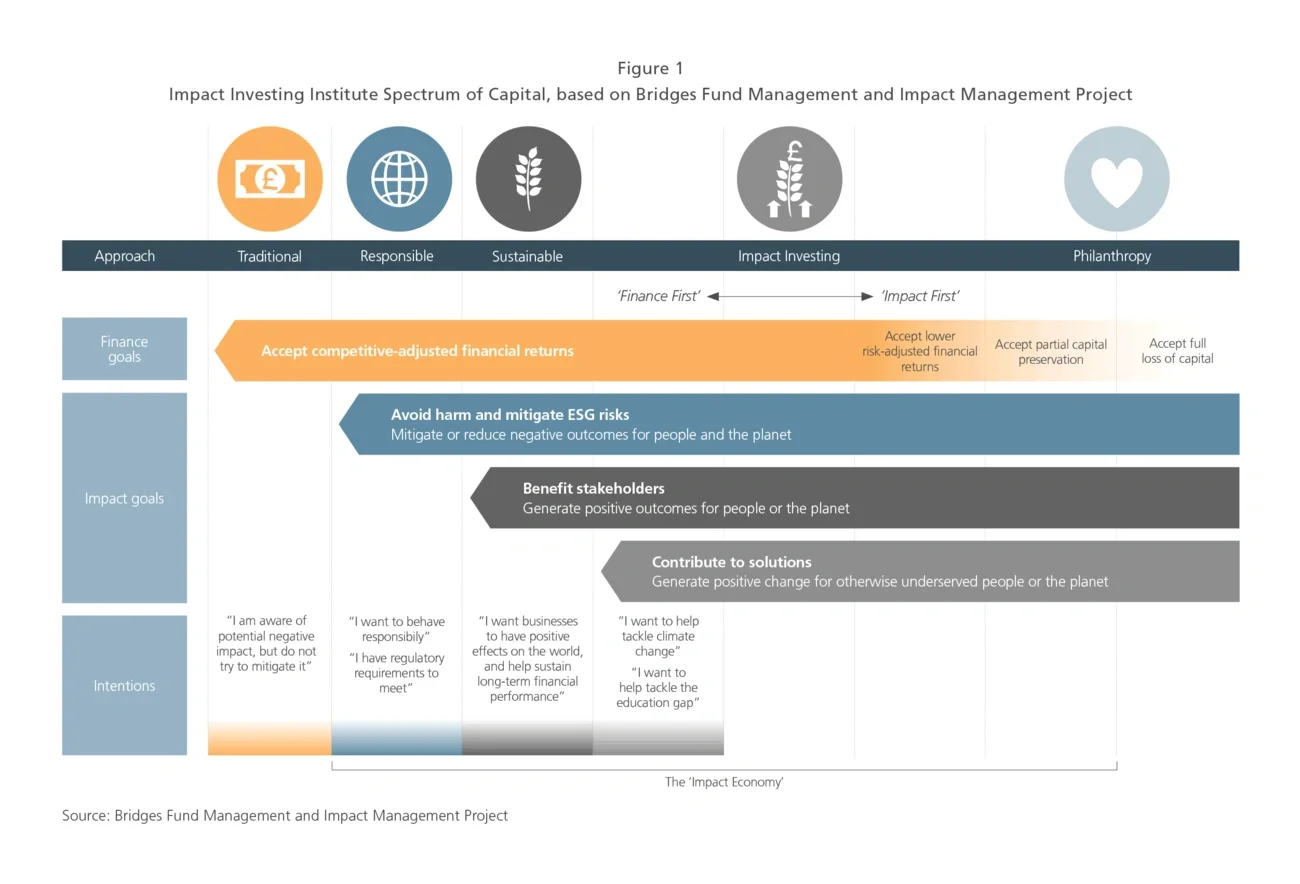

One tool often used to understand the diverse sustainability investing landscape is the Spectrum of Capital (Figure 1, below). This maps different styles of investing based on their purpose or intended outcome. ‘Traditional’ funds focus on risk-adjusted financial returns; ‘responsible’ funds seek to reduce harm; ‘sustainable’ funds aim to benefit people and the planet; and ‘impact’ funds try to create positive impact, particularly for underserved people or the planet. Other definitions describe sustainable investing as focusing on the ‘how’ of a business’s operations, while impact investing focuses on the ‘what’ of a business’s products and services.