Key takeaways

-

The growth of renewables in the Texas energy mix will likely present opportunities and challenges, creating disruption in the commercial landscape.

-

Investing in grid diversity, flexibility and management provides an opportunity to capture value in a more dynamic energy setting.

-

Lessons from Texas can be applied globally as international energy systems face unique challenges with rapidly changing generation mixes.

-

By identifying how energy dynamics are likely to develop and where pinch points might occur, players can invest ahead of the curve to meet challenges and unlock significant value.

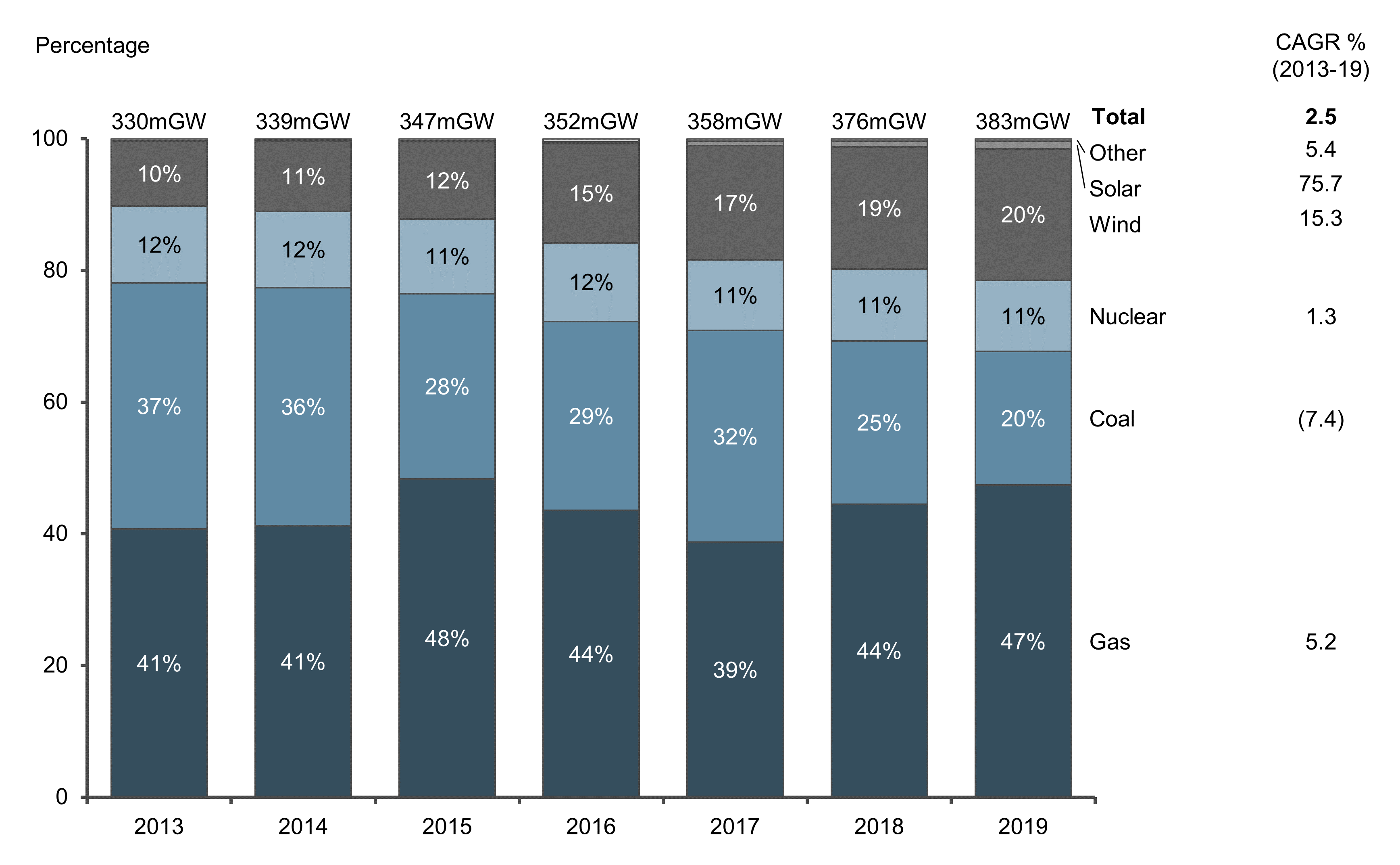

While recent discussions about energy and Texas have focused on the state’s fracking boom, Texas has also presided over a successful period of energy transition, doubling the use of renewables from 10% in 2013 to 20% in 2019 (see Figure 1). Not only has this energy diversification yielded benefit in the battle against climate change, but it has also been achieved with low average prices ($20/MWh-$40/MWh) in an environment of strong demand growth (2% p.a. since 2013).

This growth and affordability represent considerable successes, but challenges remain. Recent years have seen significant price volatility, including dramatic, if brief, price spikes in the summer of 2019 (up to $9,000/MWh). These events were driven mostly by the concurrence of low wind over wind farms in northwest Texas and high demand due to hot conditions in major cities, creating a mismatch in generation and demand that drove up prices in the Electric Reliability Council of Texas (ERCOT) electricity market. This gap between generation and demand is an increasingly important feature of grids with growing renewable penetration that varies by season and time of day, potentially causing price volatility.

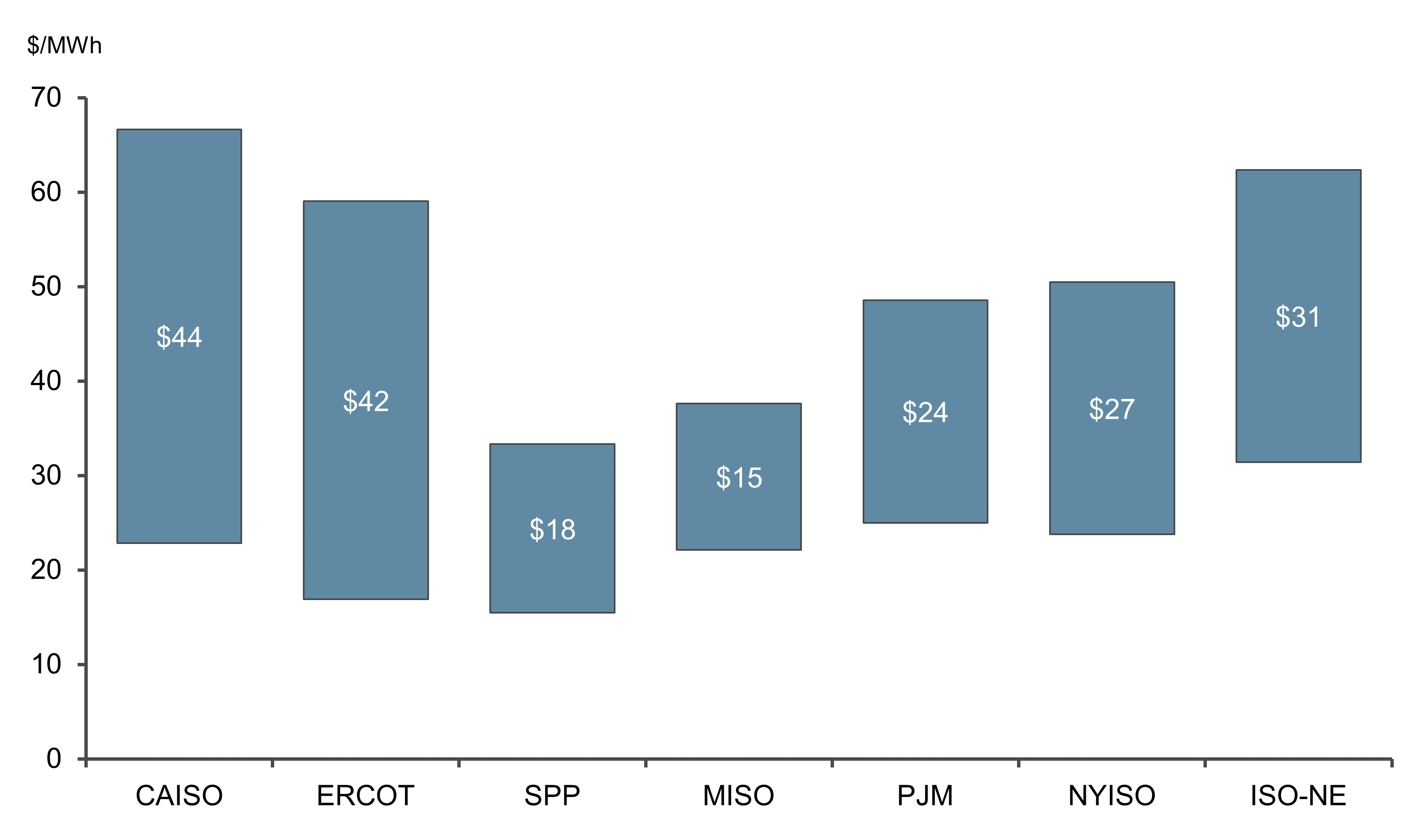

Price volatility is already higher in ERCOT than in most other U.S. grids (see Figure 2). As renewable penetration into Texas’ grid increases, demand continues to grow and climate change makes energy-intense heat events more frequent, geographic, seasonal and diurnal gaps between generation and demand could become more likely. However, preventing them is critical to ensuring stable energy provision. Otherwise, high price volatility could weaken business investment and undermine consumer confidence in energy transition.

Investors can both capture value and provide significant social/environmental benefits by resolving these challenges. By diversifying the renewable energy mix, providing energy storage and securing transmission, investors can meet demand peaks even when generation is low. Investors need to focus on providing supply flexibility rather than incremental increases in generation in order to bridge the seasonal, diurnal and event-driven supply/demand gaps that drive price volatility, thereby capturing maximum value.

ERCOT: The challenge and solution

Texas has pursued a multidecade plan to diversify its energy generation capacity and capture the environmental resources of the state. Between 2006 and 2013, Texas created Competitive Renewable Energy Zones in order to incentivize the development of transmission lines to deliver electricity from northwest Texas (where wind resources are plentiful) to major urban centers (Dallas, Fort Worth, Austin). Over a similar period, the levelized cost of energy (LCOE) for wind decreased by over 70%, from $135/MWh in 2009 to $41/MWh in 2019. As a result, wind power generation has increased at approximately 15% p.a. since 2013, adding around 44GWh of capacity.1

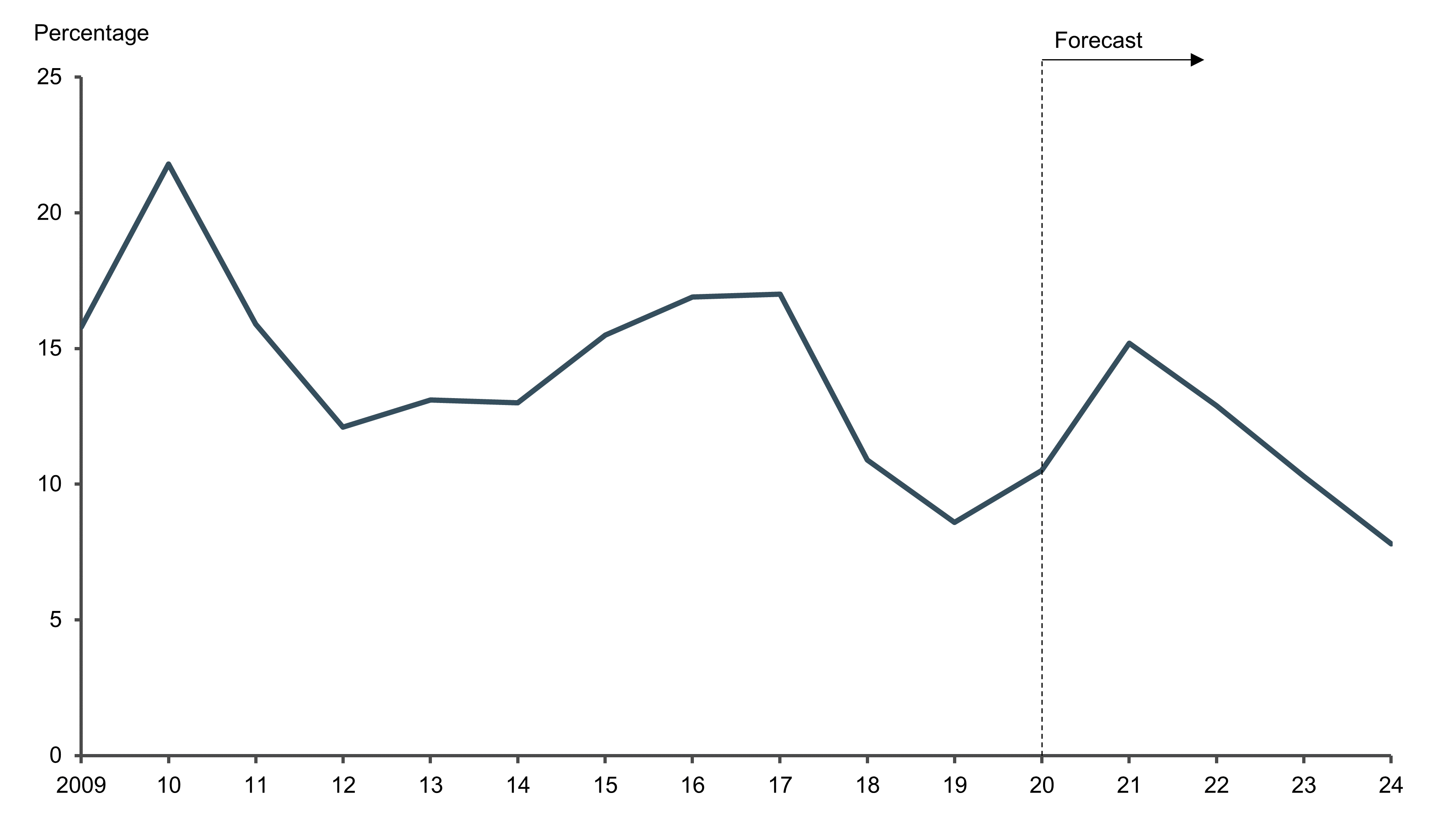

Also over a similar period, natural gas prices have declined to a persistently low level, falling from a peak of $8.7/MBtu in 2008 to $2.6/MBtu in 2019, and remaining below $4/MBtu since 2014. This has placed significant pressure on Texas’ coal generation capacity, which has been characterized by significant plant retirements. As a result, the summer capacity reverse margin on ERCOT, reflecting energy “headroom,” has declined from approximately 16% in 2009 to approximately 9% in 2019, and is forecast to fall further, to roughly 8% by 2024 (see Figure 3).

Declining headroom creates a potential challenge to maintaining stable low prices, given the hot Texas climate. Texas summers create a significant uptick in energy demand in the form of air conditioning, raising peak hourly demand from 60GW to 70GW. This high demand places significant stress on generation assets, particularly during periods of low wind. Furthermore, as renewable penetration increases, daily gaps may widen, given the mismatch between peak renewable generation times and peak demand periods (as in California’s infamous “the duck curve”). Meanwhile, demand is growing and climate change is increasing the risk of extreme weather, intensifying the threat of production shortfalls.

Lessons for investors

Investors in Texas energy need to invest wisely in order to meet these challenges. Simply investing in greenfield capacity additions risks further depressing prices, without resolving the fundamental volatility challenge for the state’s consumers and businesses. The greatest opportunity to realize value in the Texas energy market is in addressing the supply/demand mismatch and creating supply flexibility. Key lessons include:

Capture diversification in the renewable mix

While Texas has successfully exploited its wind resources, it has yet to exploit its tremendous insolation resources. At present, less than 5GW (1%) of power in Texas is generated by solar energy,2 yet the state’s insolation rates are among the country’s highest. Furthermore, solar LCOEs at utility scale have declined by approximately 90% over the past decade, to $36/MWh-$44/MWh, making it highly competitive. As a result, solar energy is expected to grow rapidly over the next three years, with planned installations of 10GW by 2022, on top of a base of 2.2GW in 2019.

If the Texas energy grid diversified into solar, operators could benefit on hot summer days when wind production is low, possibly taking advantage of price peaks. Investors, however, should remain cautious; capacity additions could depress generation prices, limiting upside. For example, a BloombergNEF analysis suggested that adding 3.4GW of new capacity in 2020 could depress average summer peak prices by around $4/MWh. Furthermore, while solar power may reduce event-driven generation/demand mismatches, it is vulnerable to daily mismatches.

Develop storage capacity

Storage capacity can most directly address supply/demand gaps by allowing owners to release energy generated at low prices into the grid at peak demand. This flexibility could allow storage owners to command premium prices for their power and dampen the volatility in Texas’ energy market. As a result, storage is developing rapidly in Texas, growing from 104MW in 2019 to 568MW in 2021.3 Investment in this space allows investors to capture a significant part of the solution to supply/demand gaps in an increasingly renewable-focused market.

Support transmission capacity

As the network diversifies with new solar installations, transmission capacity will need to keep pace. Transmission investment allows renewables investors to avoid front-end production risks. Furthermore, both wind and solar buildout in Texas are expected to stimulate material need for new infrastructure to support remote locations. Sempra and Berkshire Hathaway’s battle to purchase Oncor (a Texas transmission and distribution utility) highlighted the power of this idea. Oncor eventually sold to Sempra for some $9 billion. Investing in transmission could allow investors to benefit from stable utility-style returns, with significant upside, as transmission buildout is required to support remote renewable sites.

Drive the supporting data, automation and equipment

Investors can find and capture value beyond these three themes by looking deeper into the supply and service chain. An ecosystem of equipment and service providers exists around renewables and transmission infrastructure, supported by data and analytics to optimize operations. For example, numerous software providers (e.g., Uptake, OSIsoft) and original equipment manufacturers (e.g., GE, Vestas, Siemens) are currently competing to develop optimization programming for wind assets. Investors should seek out the players within this ecosystem that can integrate equipment and data to drive operational performance on assets and maximize value.

Conclusions

Smart investing in Texas energy requires investors to understand and address ERCOT dynamics. The growth of renewables in the Texas energy mix is likely to present opportunities and challenges, creating disruption in the commercial landscape. Institutions and investors in Texas that can resolve peak usage and transmission problems stand to capture a significant share of value. By contrast, poorly planned investments in capacity could perpetuate a cycle of declining average prices and low returns. Investing in grid diversity, flexibility and management provides an opportunity to capture value in a more dynamic energy setting.

These lessons from Texas can be applied globally. International energy systems are facing unique challenges, with rapid changes in their generation mixes. Not only are social, political and environmental pressures driving interest in renewables, but economics will likely support rapid shifts away from less-competitive fossil fuel assets. Investors need to think critically to navigate this transition. The focus on renewables could create an overheated market in some sectors, where investments could easily underperform. Furthermore, unstrategic investing could create grid instability, price volatility and resource inadequacy. At a macro level, the rapid changes in economics, politics and society create considerable uncertainty. And black swan events, such as the rapid slowdown in unconventional drilling driven by supply-side price wars and COVID-19’s impact on demand, could lead to short- or long-term shifts in transition pathways, as the relative costs of energy fluctuate rapidly.

As a result, smart investing in context will require careful considerations of local conditions, future pathways and developing needs. Investors need to ask the right strategic questions and pressure-test their answers under a range of considered energy transition pathways, not just end states. By identifying how energy dynamics are likely to develop and where pinch points might occur, investors can invest ahead of the curve to meet these challenges and unlock significant value in the process.

Endnotes:

1ERCOT — Generation data (2010-17) files

2ERCOT — Generation data (2019) pack

3ERCOT — Capacity data

06202023140648