Ensuring global energy security

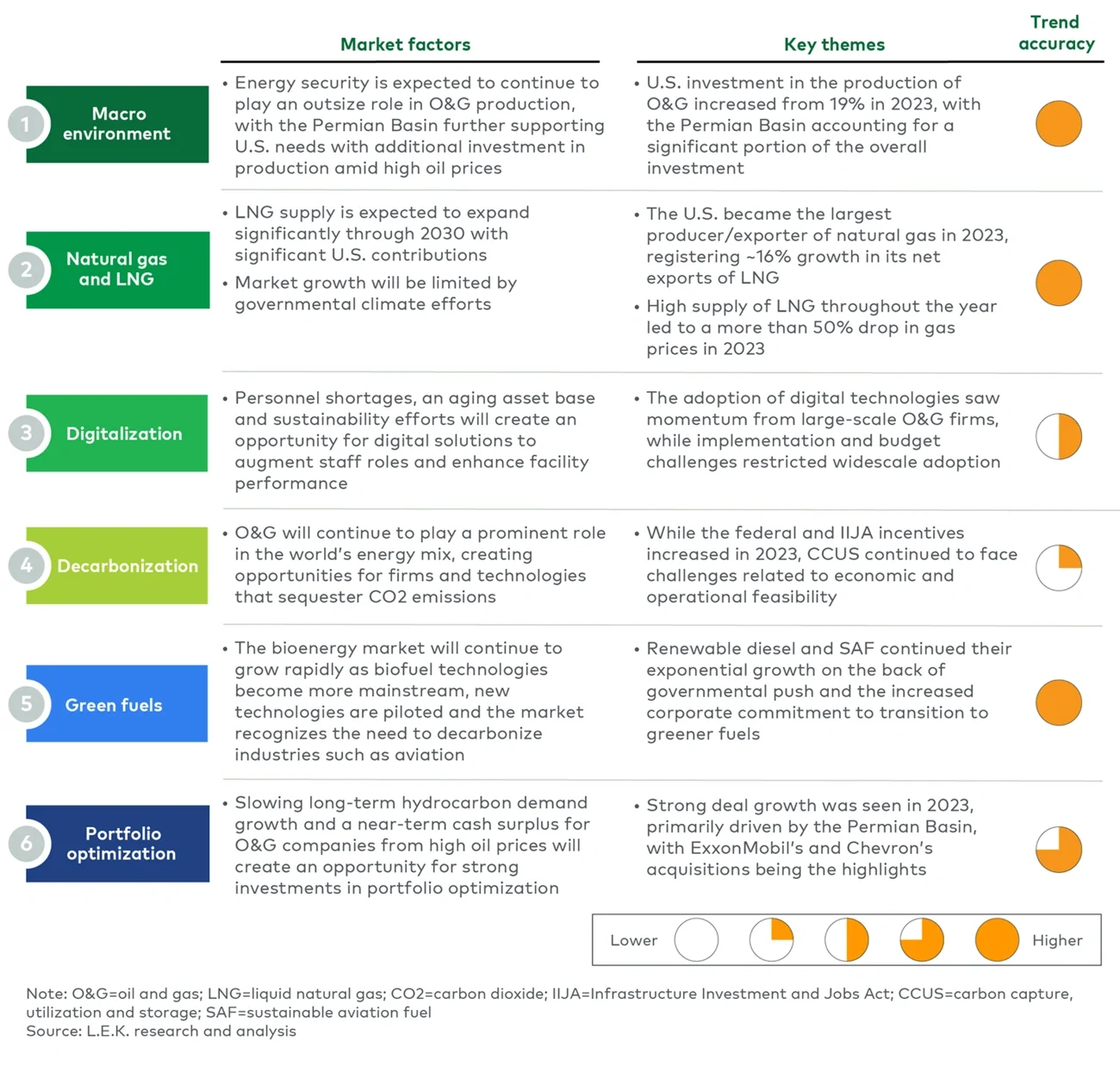

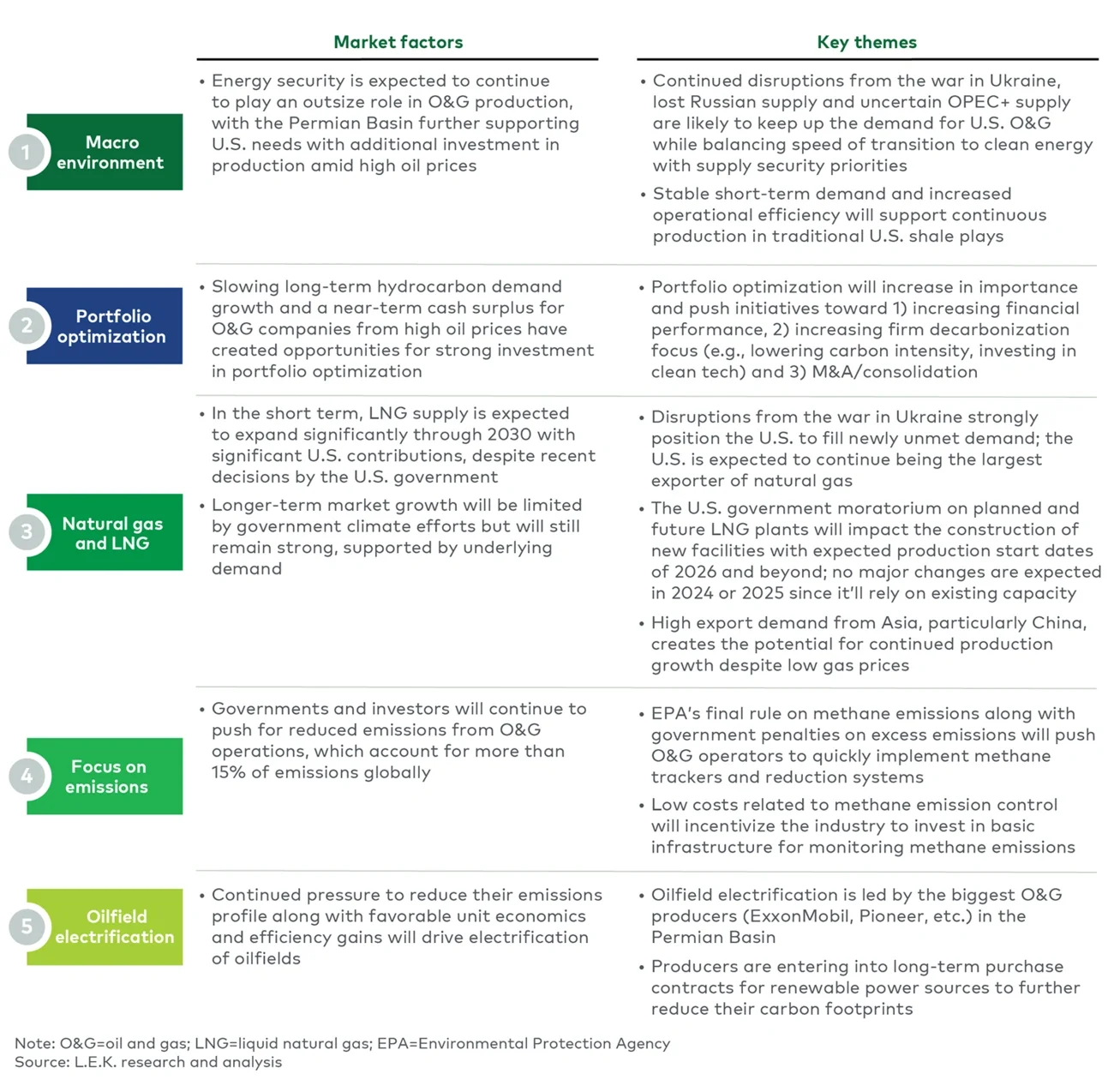

With continued disruptions and realignments expected on the geopolitical front worldwide, energy security will play an outsize role in the oil and gas industry this year, much as it did in 2023. Factors with the largest impact include the lost Russian supply due to the war with Ukraine and the potential OPEC+ supply response (most likely to sustain curtailments through the end of the year).

Boasting a significant capacity buildup through upstream capital spending in the past few years, the U.S. and the rest of North America are poised to continue to meet the increased demand. In the Permian Basin especially, additional investment in production amid high oil prices is expected to take advantage of untapped oil reserves, driving an estimated 25% growth in production through 2028 (from 8.5 million in 2023 to an estimated 10.5 million in 2028). We can expect to see continuous production in traditional U.S. shale plays through 2024 thanks to stable short-term demand and increased operational efficiency.

The industry should also see a heightened focus on balancing the speed of transition to clean energy with supply security priorities as quickly approaching 2025 and 2030 decarbonization targets drive investment. As observed in our recent 2023 Energy Study, the oil and gas industry will continue to increase its emphasis on decarbonization initiatives that best fit each individual reality while keeping focused on improving overall portfolio performance.

Meanwhile, investments in the energy transition will stay a priority but be highly scrutinized.

Optimizing portfolios with a cash surplus

A key factor to watch in 2024 is portfolio optimization — companies will continue to evolve and consolidate, bringing an active year for M&A as the industry continues to seek larger economies of scale, higher financial performance and a lower overall carbon footprint associated with operations. An opportunity for strong investment has been created for legacy oil and gas companies by slowing long-term hydrocarbon demand growth, while a near-term cash surplus from high oil prices opens doors for oil and gas companies of all sizes.

The market has already seen a handful of notable M&A moves this year, such as Chevron acquiring Hess for $53 billion to gain access to Hess’ position in high-quality assets such as the deepwater Stabroek oilfield in Guyana and U.S. shale operations in the Bakken, ExxonMobil doubling its Permian Basin footprint through the $64.5 billion acquisition of Pioneer Natural Resources, and Talos Energy boosting its deepwater asset portfolio in the Gulf of Mexico by purchasing QuarterNorth Energy for $1.29 billion.

Additional moves prove an increased interest in clean technology investment, including Shell plc investing in a green hydrogen plant in the Netherlands, Occidental Petroleum’s carbon capture facility that is set to open in 2024 and ExxonMobil’s move to invest approximately $15 billion per annum through 2027 in renewable energy initiatives to diversify its energy mix.

US domination of natural gas and liquefied natural gas

This year, global investment in new liquefied natural gas (LNG) infrastructure is expected to reach $42 billion annually, with global LNG supply continuing to grow toward a predicted peak of 705 million tons per year in 2034. An uptick in demand from Asia, particularly China, could incentivize more LNG production in the U.S. and abroad — the U.S. is forecast to remain the largest exporter of LNG to Europe and Asia, continuing to replace lost Russian supply. From 2018 to 2021, about 30% of U.S. LNG exports went to Europe; however, in the past two years this has grown to over 60%, an increase that’s expected to continue.

Notable market activity so far this year includes a joint $10 billion venture between QatarEnergy and ExxonMobil expected to start production in Texas, a $13.2 billion development sanctioned for Venture Global’s LNG export plant in Louisiana and a 20-year deal signed by German utility EnBW and Venture Global.

While the U.S. leads in approved LNG projects globally with about 32% of the total, this momentum faces headwinds from a Jan. 26 announcement that the Biden administration will pause pending and future permits to export LNG to non-Free Trade Agreement countries until the Department of Energy finishes a new review of climate impacts. It is estimated that this review may take up to one year, which means we will see a minor impact on the short-term outlook — as supply capacity is already in place — and a larger effect on post-2026 supplies, given construction times. The industry may see this pause reconsidered in 2024 or 2025, given the expectations of international allies in Europe and Asia that the U.S. will replace Russia as a leader in the global LNG market.

Bigger focus on emissions

This year is expected to see a marked change in the way operators think about and address emissions as increased pressure from governments and regulatory agencies drives investments aimed at reducing them.

A May 2023 report from the International Energy Agency (IEA) predicted that emissions intensity of oil and gas activities will fall by 50% by the end of 2030. In the U.S., the Environmental Protection Agency’s (EPA) Dec. 2, 2023 final rule aimed at sharply reducing methane emissions from oil and gas operations will promote the use of cutting-edge methane detection and reduction technologies.

Associated financial penalties from EPA’s ruling that increase year by year, from $900/ton in 2024 to $1,200/ton in 2025 to $1,500/ton thereafter, can be expected to provide the industry with the incentive to meet these new mandates. An indicator of interest in this direction is the number of early-stage venture capital firms that have attracted funding to develop new techniques for sensing methane and for products designed to use methane to supply on-site energy.

Fortunately for the companies facing increased governmental pressure, mitigating methane emissions is among the lowest-cost options of any technology that can bring about a step change in global greenhouse gas emissions; almost all available abatement measures cost less than $20/ton of carbon dioxide equivalent, and most would cost considerably less.

Permian Basin power: Electrifying oilfields

Pressure to reduce emissions, along with favorable unit economics and efficiency gains, will lead to more electrification of oilfield equipment in 2024. A slowly expanding electric grid offers electric options to more wells, such as replacing gas-powered compressors with electric ones that are powered by renewable sources, helping companies meet the new EPA standards.

We have already seen producers entering into long-term purchase contracts for renewable power sources to further reduce their carbon footprints. Leading in electrification are the biggest oil and gas producers, like Oxy, Pioneer and ExxonMobil, in the Permian Basin.

Oxy plans to meet almost 30% of its new Permian Basin compression needs in 2024 with electric compressors, an increase from about 7% in 2023. Pioneer is actively partnering with a local utility provider in the Permian Basin to develop a long-term renewable power delivery strategy for electrification of drilling, completions and field compression, and it has also partnered with NextEra Energy Resources on a 51-turbine wind farm project. ExxonMobil has established plans to achieve net-zero greenhouse gas emissions in the Permian Basin by 2030, powering its operated assets with low-carbon sources like wind, solar and hydrogen.

Don’t overlook these additional factors

- Focus on operations: Companies are looking to leverage new tech and upskill their workforces to do more with less in a highly uncertain economic environment.

- Technology adoption: Artificial intelligence and data analytics tools can increase efficiency and optimize production through predictive maintenance; higher investments in digital twins and cybersecurity are expected.

- Decarbonization: New technology related to methane leak detection and flaring reduction could see more investments this year, while carbon capture, utilization and storage may face headwinds after the IEA shared doubts that large-scale carbon capture can significantly help achieve net-zero goals.

- Renewable fuels: The International Air Transport Association estimates that sustainable aviation fuel production in 2024 will triple to 1.875 billion liters, accounting for 0.53% of aviation’s fuel need and 6% of renewable fuel capacity.

Generally, the oil and gas industry is looking at the continuation of long-term trends in 2024, rather than an influx of new factors, to drive investment. However, innovation, global supply and regulatory requirements can be relied on for a consistently evolving environment that will affect strategic plans across the market.

For more information, please contact industrials@lekinsights.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC