The macroeconomic environment has been challenging recently for much of the construction sector. However, plumbing services provide some potential resilience. While consolidation in the sector is increasing, it remains highly fragmented and offers attractive acquisition opportunities. Companies that pursue platform expansion will be at a significant advantage due to market dynamics that favor scaled players.

Solid market fundamentals

A combination of market attributes — including steady growth, recession resiliency and expected increase in demand — make plumbing services a sector with potential.

Stable base and recession resistant

Plumbing services benefit from a large underlying pool of demand. It is primarily driven by the size of the installed base of homes, which grows in tandem with the overall population. While the population growth rate in the United States fell during COVID-19, it is currently recovering, albeit more slowly than in prior years, due in part to lower immigration. Meanwhile, the number of households has shown steady and consistent growth as households continue to form, particularly among millennials. Similarly, the U.S. housing stock is expected to grow at a steady rate through 2026. Together, these trends indicate a large and relatively stable pool of demand for plumbing services in the near future.

A handful of factors help insulate plumbing services against economic downturns such as the one we are currently experiencing. First, plumbing skews more toward repair and remodel (R&R) services and is viewed as nondiscretionary, making it less volatile than other product categories. Plumbing services are also considered noncyclical compared with other types of building and construction spend. Although bathroom and kitchen remodels (front-of-wall plumbing) are a bit more cyclical than other plumbing services given that these projects can be delayed, they benefit disproportionately during economic rebounds. Furthermore, homeowners are often more willing to spend on premium products (e.g., faucets and HVAC) that they use more frequently.

Service diversity

Plumbing services are highly diverse, and unlike services for which there may be a rule of thumb for a standardized service, plumbing services are hard to define and price discretely, especially for break-fix services. Prices can also vary dramatically depending on the scale and complexity of the job, time of day (e.g., daytime versus after hours), day of the week (e.g., weekday versus weekends), and size of the provider. Nevertheless, the need for plumbing services tends to occur frequently. The need for services can also be unexpected, and timeliness is often critical. Indeed, between 70% and 80% of plumbing services are viewed as urgent, which reduces a customer’s willingness to price shop.

Aging housing stock

Housing stock in the United States is getting older, with median age increasing from 38 years in 2015 to 42 years in 2021. As a result, more plumbing problems are likely to arise. Homes that are over 30 years old may have aging fixtures or problems due to poor original installation. They may also have lead, galvanized steel or polybutylene pipes, all of which can cause problems with drinking water and are more likely to require replacement. Other issues include bellied lines — as the soil that homes are built on settles over time, the underlying pipes may slope or bend.

Recurring services

Most homeowners don’t have regular maintenance plans for plumbing in the same way they might for HVAC systems, but service companies that provide both HVAC and plumbing services have found that the loyalty and repeat business of their HVAC customers can be cross-sold to their plumbing customers. There may also be an opportunity to expand service plans to plumbing where there is a recurring need. For example, a typical water heater should be serviced about every five years, and drains should be cleaned around every four years. This is a clear revenue expansion opportunity, especially for integrated players that can offer plans in which they visit the home (e.g., every six to 12 months) and provide preventive services.

Some larger players are already offering these types of plans to customers. For instance, Mr. Rooter Plumbing has maintenance and 24/7 emergency services. Its maintenance plans and Advantage Plan include preferred pricing, priority scheduling and other benefits. F.H. Furr has a Preferred Partner Plan that provides preventive maintenance, priority service, discounts of 15%, special coupons and campaigns, and free HVAC, electrical and plumbing home inspections.

Maintenance plans are a clear win for providers. Not only do they ensure recurring revenue and the opportunity to identify additional service needs, but they also increase customer stickiness. Research shows that around 40% of homeowners call a previous plumbing provider for their next service need, and maintenance plans can support and extend this loyalty.

Consolidation versus fragmentation

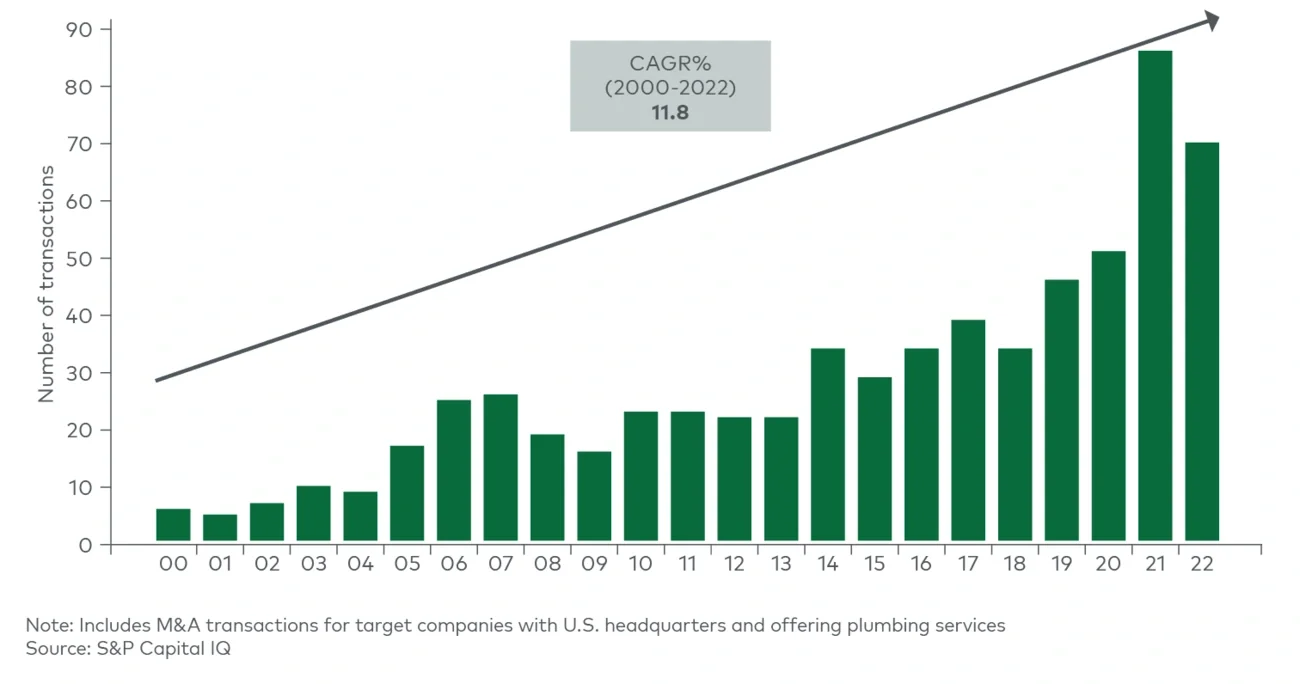

The plumbing services market is highly fragmented, with many small providers and practitioners. That said, the pace of consolidation in the plumbing services market is increasing. Indeed, M&A activity has increased on average by nearly 12% a year since 2000, with a noticeable jump in activity over the past two years (see Figure 1).