If an organisation is to formulate a commercially viable and actionable plan to reduce emissions, they will need to understand their decarbonisation options and the associated economics.

Without this knowledge and understanding, organisations risk pursuing higher cost or higher risk emissions reduction pathways that may put the organisation at a competitive disadvantage.

Competitive dynamics of decarbonisation

Once organisations understand their decarbonisation options, they need to consider the dynamics facing their peer competitors. Competitors may have lower input costs, such as electricity or gas prices, have access to low carbon inputs, have more carbon-efficient facilities, or even have access to greater government support — all of which could impact their economics and shape their strategic choices.

As an example, in glass manufacturing, incorporation of more recycled content (cullet) into the final product lowers the emissions intensity of the bottle more than reducing the proportion of natural gas used to operate the furnace. Therefore, participants who can access recycled content more economically can reduce their carbon footprint more than, say, those who seek only to substitute lower carbon energy inputs. Similarly, offshore competitors with access to cheap electricity and gas could potentially deliver lower-cost products to Australia, displacing locally manufactured products — particularly if they do not face carbon costs like the Safeguard Mechanism, and in the absence of carbon border adjustment regulations.

Different emissions reduction policies and carbon pricing across countries present a particular challenge for both businesses and governments. Businesses facing domestic carbon costs that do not apply to imports are disadvantaged, which can ultimately result in imported products displacing domestic production and may even result in an increase in global emissions (‘carbon leakage’).

A Carbon Border Adjustment Mechanism (CBAM) is an emerging solution to apply equivalent carbon pricing to domestic and imported products. The European Union’s CBAM is scheduled to take effect in 2026 for aluminium, cement, iron and steel, electricity, hydrogen, and fertiliser commodities and products, and CBAMs are under investigation and in development around the world, including in Australia. Given the many complex policy design choices that must be made to implement a CBAM — some of which are not neutral in application across market participants — CBAMs should not be viewed as a panacea, particularly as a CBAM does not address other competitiveness challenges for domestic manufacturers that are related to carbon policy but not directly reflecting carbon pricing (for example, ability to secure cost-competitive natural gas).

The implication of a careful competitive carbon analysis is often that competitors have different emission reduction economics-based variances in options, inputs or policy environment. Understanding the relative advantages that you and your competitors face can give you and your organisations greater confidence around the pathways those competitors are likely to take, and therefore help shape your own choices to successfully compete in a carbon-constrained future.

Achieving a balance: passing on decarbonisation costs

Organisations then need to consider to what extent their decarbonisation costs can be passed through to customers.

The customer willingness to pay will be one factor. Some customer segments may be willing to pay premiums for environmentally friendly products (‘green premiums’), while others less so. For example, recent work we have undertaken in various markets has shown that stated willingness to pay for lower carbon products is greater in premium products where the decarbonisation costs represent a relatively immaterial increase on the overall product cost. Segments where end consumers are younger and more affluent also tend to experience this. Luxury motor vehicles are an example of this dynamic, where the costs of low-emission inputs are small relative to the final price of the vehicle, and environmental responsibility is an important part of the value proposition to customers.

However, green premiums remain elusive in practice and stated intentions do not necessarily flow through to purchasing behaviour.

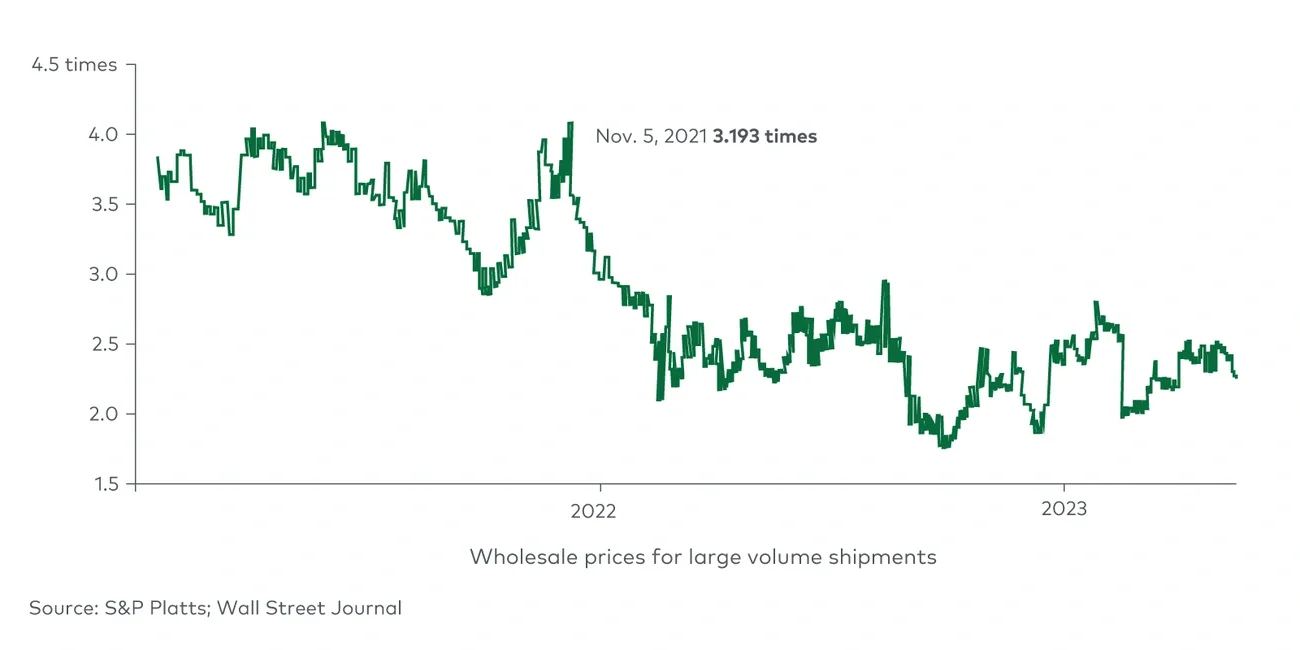

One example of this is sustainable aviation fuels. While there has been an observable premium of 2-4x for sustainable aviation fuel (SAF) over conventional jet fuel (driven by substantially higher production costs), adoption remains low in the competitive aviation industry. Part of the challenge for SAF adoption is the increased cost of SAF, where many airlines offer carbon offsets at low cost that represent a ‘good enough’ solution for some customers.2 The implication of this is that organisations need to understand nuances at the segment level (e.g. including potential early adopters) when considering whether and how to pass on decarbonisation costs.