Realizing the potential in these emerging indications will require the following:

- Deliver transformative efficacy

Build unequivocal evidence of a step-change in efficacy across endpoints routinely accepted as establishing durable benefit in as wide a patient population as possible. - Clearly define epidemiology

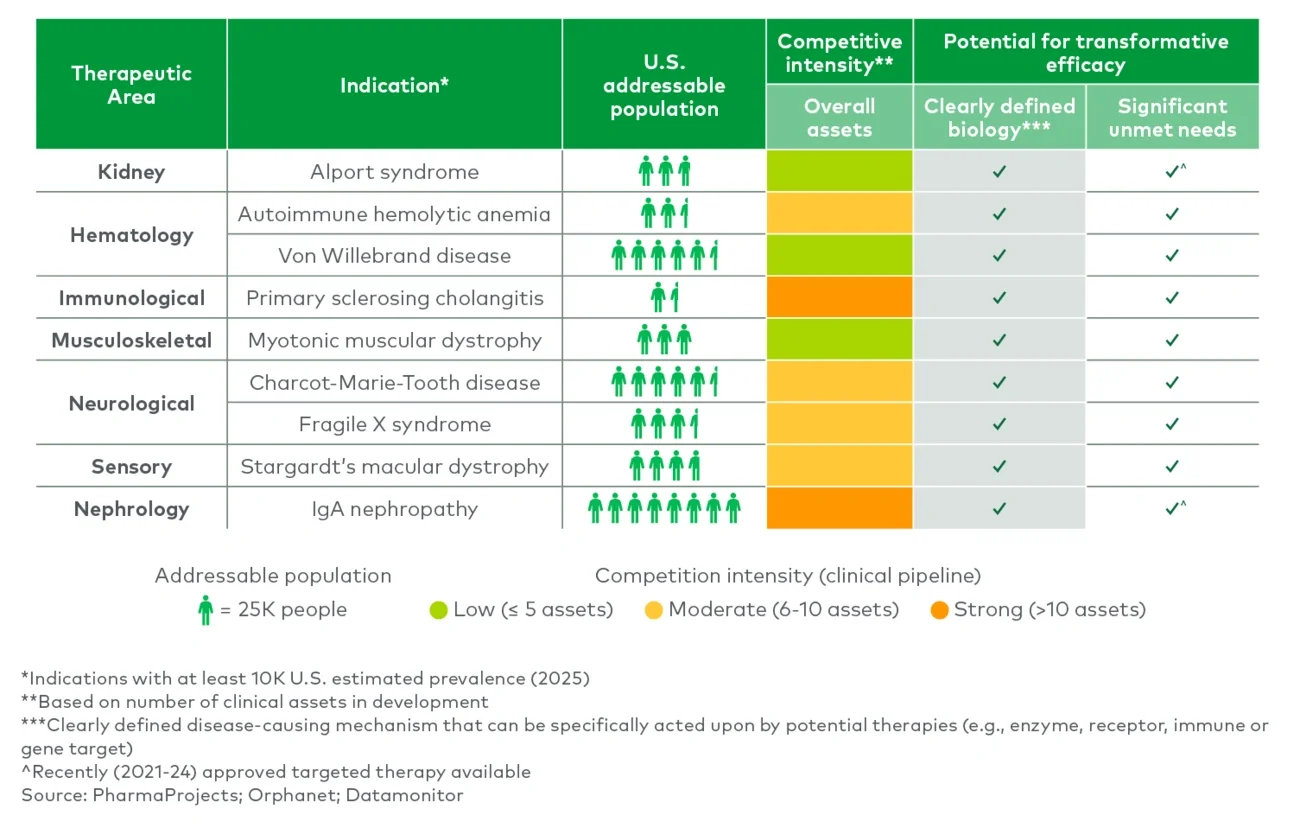

Reliable prevalence data is critical and companies that invest early in clarifying disease epidemiology create the foundation for both payer negotiations and patient advocacy engagement. - Systematically find patients

Successful companies are deploying multi-pronged approaches to resolve diagnostics bottlenecks, including genetic testing, AI-driven EMR mining and specialist education to uncover untreated and undertreated populations. - Articulate residual unmet need

Even in conditions with existing therapies, residual gaps (durability, administration burden, partial efficacy) must be clearly documented (e.g., patient-reported outcomes are particularly powerful in demonstrating quality-of-life improvements). - Build a robust HEOR evidence base

As orphan drugs expand toward meaningful patient populations, payers are likely to demand evidence of reduced or eliminated downstream costs, exacerbating the need to quantify avoided hospitalizations, productivity loss and long-term complications. - Engage stakeholders early

Proactive dialogue with regulators, payers and advocacy groups, including co-developing trial endpoints with regulators and collaborating on diagnostic infrastructure, can potentially accelerate adoption and support favorable coverage.

Together, these imperatives can define a repeatable model to successfully capture the opportunity in orphan drugs.

Overall outlook

The orphan drug segment is likely to remain one of the most attractive growth areas in pharma. Potential for structural advantages, resilient demand and emerging indications point toward further expansion. While policy scrutiny is likely to continue, orphan assets remain comparatively advantaged and continue to attract both investor and strategic interest.

For pharma leaders, the opportunity lies not only in scientific innovation but also in systematic market development, from patient-finding to downstream value demonstration. Companies that integrate these elements are likely to be best positioned to capture the next wave of growth in orphan drugs.

For more information, please contact us.

References

2024 FDA New Drug Therapy Approvals Annual Report

https://www.fda.gov/media/184967/download

FDA Orphan Drug Act

https://www.fda.gov/industry/medical-products-rare-diseases-and-conditions/designating-orphan-product-drugs-and-biological-products

EMA Market exclusivity orphan medicines

https://www.ema.europa.eu/en/human-regulatory-overview/post-authorisation/orphan-designation-post-authorisation/market-exclusivity-orphan-medicines

Medicare Drug Price Negotiation Program guidance

https://www.cms.gov/files/document/revised-medicare-drug-price-negotiation-program-guidance-june-2023.pdf

MIT Project ALPHA

https://projectalpha.mit.edu/pos/

Wong et al., JAMA Network Open (2023)

https://jamanetwork.com/journals/jamanetworkopen/fullarticle/2808944

Booth, Bruce. “Twenty Years in Early-Stage Biotech VC, Part 1.” LifeSciVC, 10 Oct. 2025

https://lifescivc.com/2025/10/twenty-years-in-early-stage-biotech-vc-part-1/

JAMA orphan drug vs non-orphan drug revenues (asset level)

https://jamanetwork.com/journals/jama/fullarticle/2804613%20

IQVA white paper (source for lack of generic competition and SOC claims)

https://www.iqvia.com/-/media/iqvia/pdfs/library/white-papers/from-orphan-to-opportunity-mastering-rare-disease-launch-excellence.pdf